Survey on the Access to Finance of Enterprises in the euro area - Second quarter of 2024

1 Overview of the results

This report presents the main results of the 31st round of the Survey on the Access to Finance of Enterprises (SAFE) in the euro area, which was conducted between 28 May and 20 June 2024. In this survey round, firms were asked about economic and financing developments over the three-month period between April and June 2024.[1] The sample comprised 5,940 enterprises in the euro area, of which 5,431 (91%) had fewer than 250 employees. This is the new additional round in the quarterly version of the survey, with a reduced sample and a focus on bank-based finance and trade credit in the part of the questionnaire on firm financing.[2]

Overall, in this survey round, euro area enterprises signalled more positive developments as regards the supply of bank loans, reflected in a small increase in bank loan availability, fewer obstacles to obtaining loans as well as an improvement in banks’ willingness to lend. At the same time, firms’ need for bank loans has stabilised, albeit it has not yet increased, in part due to high internal funds. Moreover, the share of firms applying for bank loans has also stabilised at a low level.

With regard to their economic situation, firms indicated that the forces compressing profitability have moderated relative to past survey rounds. Enterprises reported a further pick-up in investment over the past three months and are expecting a similar increase over the next three months.

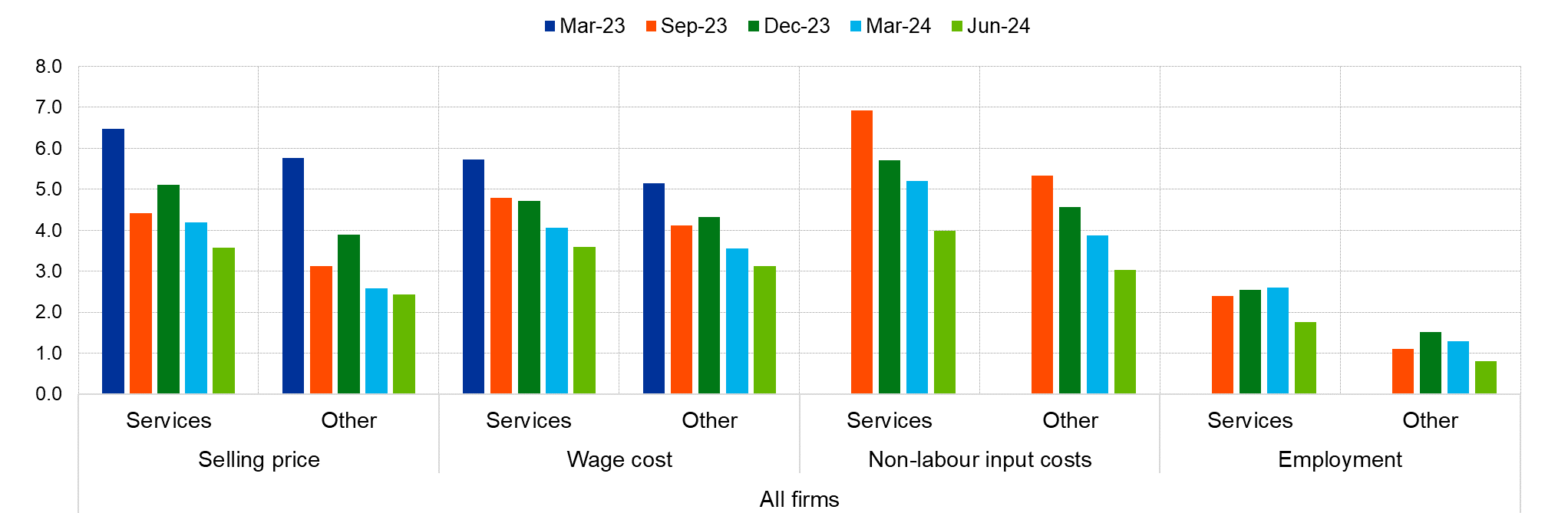

Firms in the services sector expect a larger increase in selling prices, wage costs, non-labour input costs and employment over the next 12 months compared with other sectors. At the one-year horizon, median inflation expectations are similar across the services sector and industry, whereas their dispersion is higher for the services sector.

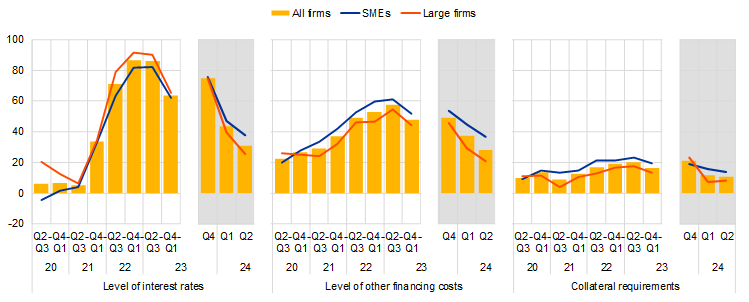

Fewer firms reported a tightening of financing conditions over the second quarter of 2024 in net terms compared with the previous survey round (Chart 1 in Section 2). The net percentage[3] of firms reporting an increase in interest rates on bank loans in the second quarter of 2024 was 31% (following 43% in the first quarter of 2024). At the same time, a net 28% of firms (down from 37%) reported an increase in other costs of financing and 11% (down from 12%) stricter collateral requirements.

Firms reported a slight reduction in the need for bank loans and a small improvement in the availability of bank loans, resulting in a small decrease in their bank financing gap (Table 1, columns 9-10 at the end of this section and Chart 2 in Section 2). In the second quarter of 2024 a net 1% of companies reported lower needs for bank loans (stable from the previous survey round). At the same time, the net percentage of firms reporting an improvement in the availability of bank loans was 2% (in contrast with the previous quarter when a net 3% of firms reported a deterioration). As a result, the change in the financing gap for bank loans – the difference between the change in needs and the change in availability – was negative for a net 1% of firms, down from the net 2% of firms for which it was positive in the first quarter of 2024. Looking ahead, firms have become more optimistic about the availability of bank loans over the next three months.

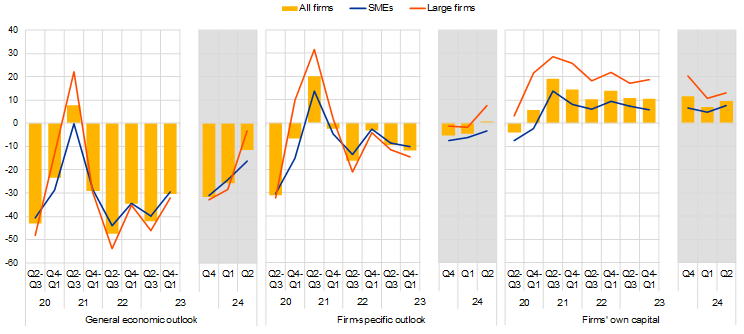

Firms perceived the general economic outlook to be the main factor hampering the availability of external financing, albeit to a much lesser extent than in the previous survey round (Chart 5 in Section 2). In the second quarter of 2024 a net 12% of firms, down from 26% in the previous quarter, reported that a deterioration in the general economic outlook had reduced the availability of external financing. On average, firms did not indicate any change in the impact their firm-specific outlook had on the availability of external financing, in contrast with the net 5% that indicated a deterioration in the first quarter of 2024.

More firms reported an increase in the willingness of banks to lend (Chart 6 in Section 2). On balance, 9% of firms reported an improvement in banks’ willingness to lend, up from 4% in the previous survey round, with both SMEs and large firms signalling a more benign risk assessment of their condition.

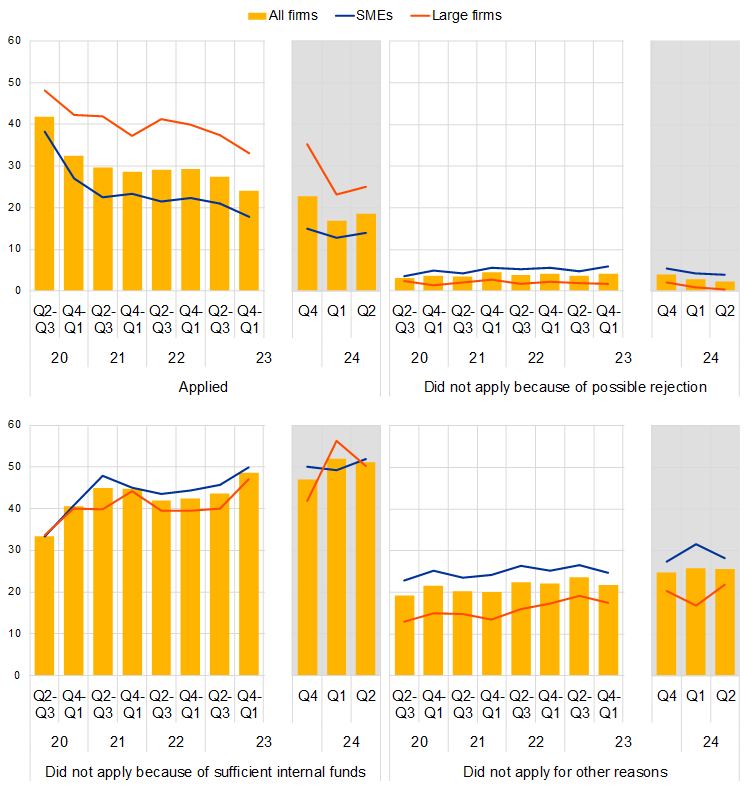

The share of firms applying for bank loans remained relatively low, mainly due to high internal funds (Chart 7 in Section 2). In the second quarter of 2024 the share of firms applying for bank loans was 19%, slightly higher than in the first quarter of 2024 (17%), and this was similar across size classes. The most common reason reported by firms for not applying for a bank loan is the amount of internal funds at their disposal, which firms consider sufficient to finance their business plans.

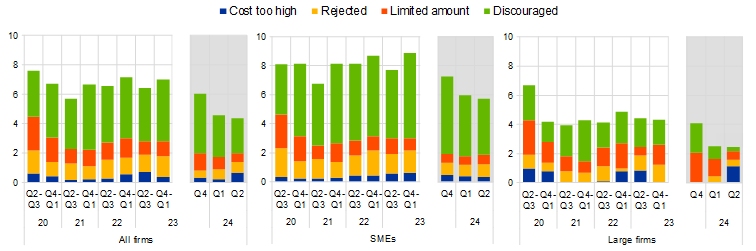

Very few firms reported obstacles to obtaining a bank loan. Among enterprises that judged bank loans to be relevant, 4% reported obstacles when seeking to obtain a loan (down from 5% in the previous round), 6% for SMEs and 2% for large firms (Table 1, columns 11 and 12 in this section, and Chart 8 in Section 2).

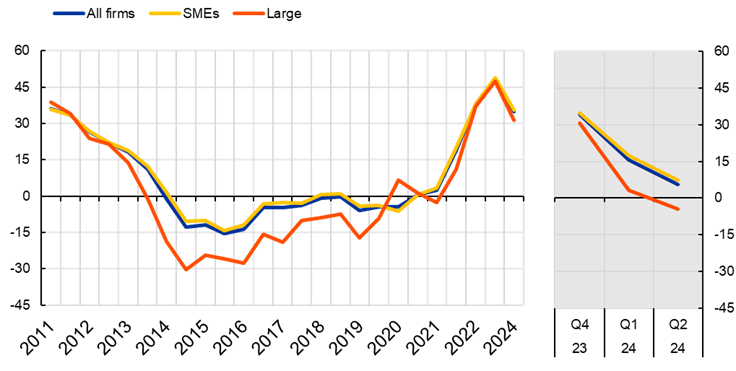

An indicator reflecting firms’ price terms and conditions of financing suggests a moderate tightening of perceived financing conditions in the second quarter of 2024 (Chart A in this section), significantly less than in the first quarter. This indicator covers changes in firms’ bank interest rates and other costs related to bank financing (charges, fees and commissions) and is one of three “principal components” reflecting how euro area firms perceive overall financing conditions.[4] In this survey round, fewer firms reported a deterioration in price terms and conditions in the second quarter of 2024, significantly down from what they signalled in the first quarter of 2024 and the last quarter of 2023 (Chart A, right-hand panel). The continuing decline reflects the ongoing moderation in the cost of borrowing. Across size classes, large firms signalled better overall financing conditions than SMEs.

Chart A

Change in price terms and conditions as perceived by euro area firms

(weighted average scores in percentages)

Base: Enterprises who applied for a bank loan.

Notes: Indicator derived from factor analysis. For details of the analysis see footnote 4. The indicator in the left-hand panel is based on firm-level survey replies from 2010 to the end of 2023, using the replies on changes in the previous six months. The indicator in the right-hand panel is calculated from the fourth quarter 2023 to the second quarter of 2024 using the replies on changes in the previous three months. The aggregate indicators are the average of firm-level scores, weighted by size, economic activity and country. Positive values indicate a deterioration in firms’ financing conditions. The individual scores are standardised, meaning that they have a range of between -1 and 1 and are multiplied by 100.

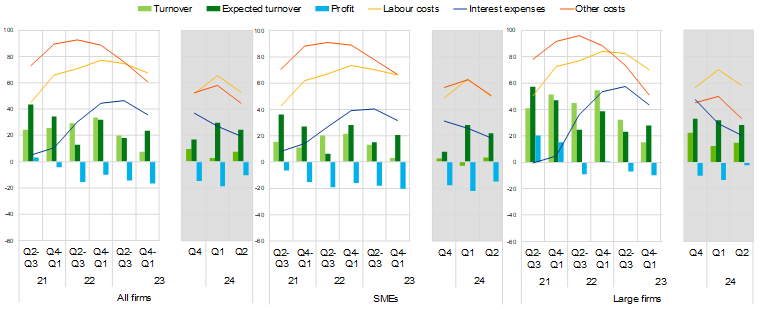

More enterprises reported an increase in turnover over the past three months. A net 8% reported increased turnover (Chart 9 in Section 3), compared with 3% the previous quarter. The increased turnover was mainly recorded by larger firms. Looking forward, firms are optimistic about future turnover, with 24% of them expecting net future increases.

Fewer firms saw a deterioration in profits, while increases in labour and other costs were indicated less often than in the previous quarter. A net 10% of euro area enterprises signalled a decline in their profits (after -19%). While cost pressures remain widespread, in net terms a smaller percentage of firms indicated an increase in labour, other costs and interest expenses than in the previous quarter.

The financial vulnerability of euro area enterprises declined further (Chart 10 in Section 3). According to this indicator, 5% of euro area enterprises encountered major difficulties in running their business and servicing their debts over the past three months (down by 2 percentage points from the previous round).

Enterprises reported a further pick-up in investment over the last three months (Chart 11 in Section 3). Firms across size classes are expecting a similar increase over the next three months.

A small share of firms in net terms indicated an increase in average hours worked over the second quarter of 2024, with firms indicating an increase in services and a decrease in industry. The overall increase was mostly associated with an increase in demand, but there were difficulties in hiring labour too (Box 1 in Section 3). To better understand labour market developments, a new set of ad hoc questions has been introduced in this survey wave. Firms were asked about the change in average hours worked over the second quarter of 2024 and the factors contributing to this. A 2% of firms indicated an increase in average hours worked in the second quarter of 2024, with a net 10% of firms indicating a decrease in industry and a net 7% of firms indicating an increase in services.

Firms expect the increase in their selling prices and wages to moderate over the next 12 months (Chart 12 in Section 3.3). Selling prices are expected to increase by 3%, on average (down from 3.3% in the previous survey round) and wages by 3.3% (down from 3.8% in the previous survey round). On average, firms in services expect their selling prices and wages to increase more strongly than firms in other sectors (3.6% in the services sector compared with 2.4% in the other sectors for selling prices, and 3.6% compared with 3.1% respectively for wage increases). In addition, firms expect their non-labour input costs to increase by 4% in the services sector and 3% in other sectors, whereas for employment, the expected increase is 1.8% in services and 0.8% in other sectors over the next 12 months.

Inflation expectations continued to decline, and the dispersion also moderated at the one-year horizon (Chart 15 in Section 3.4). Median inflation expectations stood at 3% for annual inflation in one, three and five years. Compared with March 2024, median inflation expectations fell by 0.4 percentage points for the one-year horizon and remained at 3% for longer horizons. The dispersion of inflation expectations, as measured by the interquartile range of inflation expectations, also declined for the one-year horizon. With regard to inflation in five years, more firms (50%) continued to perceive that the risks to the outlook are tilted to the upside, compared with the shares of firms seeing balanced (37%) or downside risks (10%).

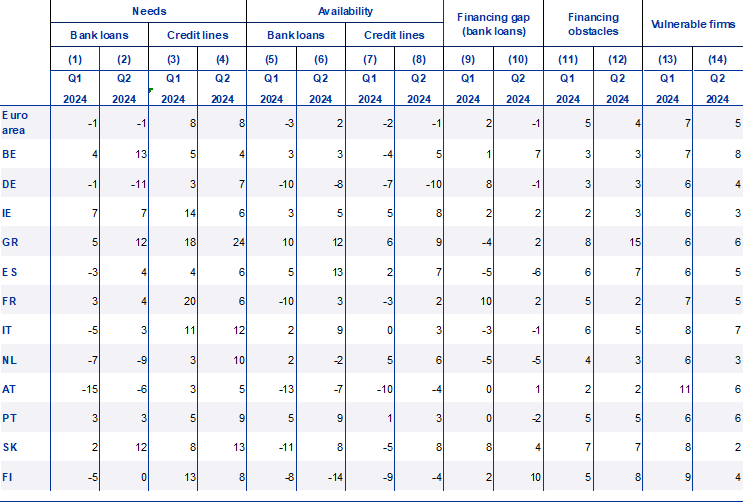

Table 1

Latest developments in SAFE country results for euro area firms

(net percentages and percentages of respondents)

Notes: For the “financing gap”, see the notes to Chart 2; for “financing obstacles”, see the notes to Chart 8; for “vulnerable firms”, see the notes to Chart 10. “Q1 2024” refers to round 30 (January-March 2024) and “Q2 2024” refers to round 31 (April-June 2024). Financing obstacles and vulnerable firms refer to the percentages of respondents, while the other indicators in the table are expressed in net percentages.

2 Firms’ financing conditions

2.1 Firms’ costs of bank loans continued to rise, but less than in the previous quarter

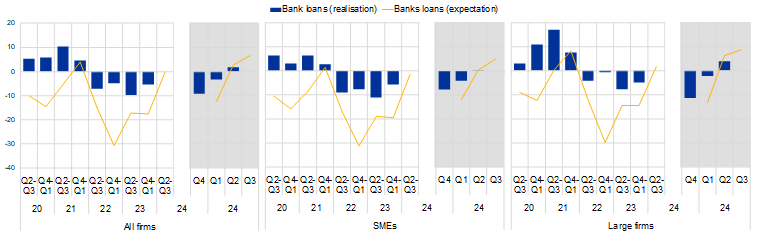

Fewer firms reported rising bank interest rates and other costs of bank financing in net terms than in the previous quarter (Chart 1). In the second quarter of 2024 the share of firms reporting an increase in bank interest rates continued to decline, to 31%, compared with 43% in the first quarter of 2024 and 75% in the last quarter of 2023. The lower percentage is consistent with the moderate tightening of credit standards reported by the euro area bank lending survey in the same period. At the same time, a net 28% of firms (down from 37% in the first quarter of 2024) reported an increase in other costs of financing (i.e. charges, fees and commissions) and 11% (12% in the first quarter of 2024) stricter collateral requirements. Across size classes, firms signalled similar developments in bank interest rates; the rise in other costs of bank loans was more widespread among SMEs than large firms.

Chart 1

Changes in the terms and conditions of bank financing for euro area enterprises

(net percentages of respondents)

Base: Enterprises that had applied for bank loans (including subsidised bank loans), credit lines, or bank or credit card overdrafts. The figures refer to rounds 23 to 31 of the survey (April-September 2020 to April-June 2024).

Notes: Net percentages are the difference between the percentage of enterprises reporting an increase for a given factor and the percentage reporting a decrease. The data included in the chart refer to Question 10 of the survey. The grey areas represent responses to the same question within a reference period of three months, whereas the main charts cover a reference period of six months.

2.2 A small increase in availability and a slight decline in needs contributed to a small decrease in the financing gap for bank loans

Firms reported a slight reduction in the need for bank loans (Chart 2). In the second quarter of 2024 a net 1% of companies reported lower needs for bank loans (stable from the previous quarter). While a net 1% of large firms indicated a decline in their need for bank loans (down from 2%), SMEs on average signalled no change (from a net 1% signalling a decrease the previous quarter).

Few firms reported an improvement in the availability of bank loans (Chart 3). The net percentage of firms reporting an improvement in the availability of bank loans was 2%, in contrast with the previous quarter where a net 3% of firms reported a deterioration. This change is due to large firms; a net 4% of these reported an improvement in the availability of bank loans (from -2% in the first quarter of 2024), while SMEs on average reported no change (0%, from -4% in the first quarter of 2024). Consequently, the change in the financing gap for bank loans – the estimated difference between the change in needs and the change in availability – was negative for a net 1% of firms, down from 2% of firms for which it was positive the previous quarter.

Chart 2

Changes in euro area enterprises’ financing needs and the availability of bank loans

(net percentages of respondents)

Base: Enterprises for which the instrument in question is relevant (i.e. they have used it or considered using it). Respondents replying “not applicable” or “don’t know” are excluded. The figures refer to rounds 23 to 31 of the survey (April-September 2020 to April-June 2024).

Notes: The financing gap indicator combines both financing needs and the availability of bank loans at firm level. The indicator of the perceived change in the financing gap takes a value of 1 (-1) if the need increases (decreases) and availability decreases (increases). If enterprises perceive only a one-sided increase (decrease) in the financing gap, the variable is assigned a value of 0.5 (-0.5). A positive value for the indicator points to a widening of the financing gap. Values are multiplied by 100 to obtain weighted net balances in percentages. The data included in the chart refer to Questions 5 and 9 of the survey. The grey areas represent responses to the same question within a reference period of three months, whereas the main charts cover a reference period of six months.

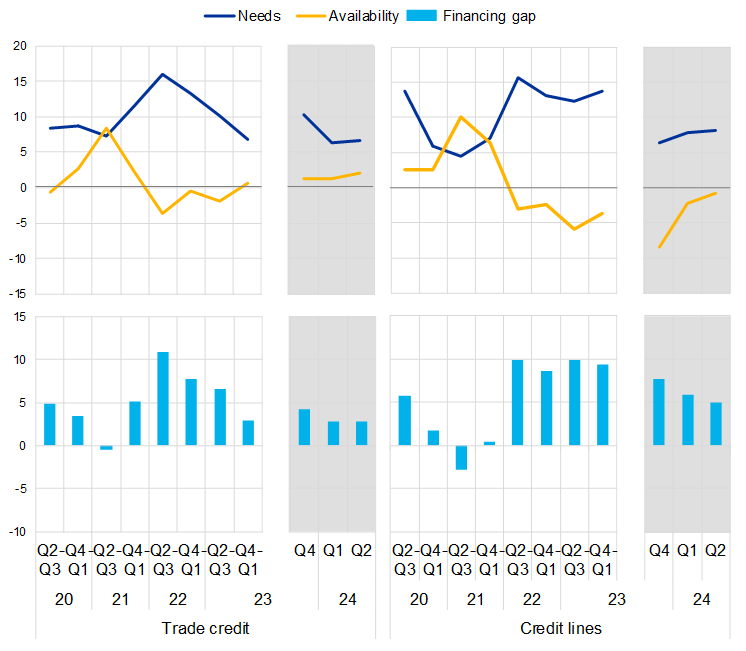

Firms continued to report an increase in their financing needs for trade credit, with a modest improvement in availability (Chart 3). A net 7% of companies reported higher needs for trade credit (similar to the previous quarter), possibly reflecting their willingness to reduce any fluctuations in their finances in times of uncertainty. At the same time, 2% of firms (up from 1% the previous quarter) signalled increased availability. Hence the change in the financing gap for trade credit remained positive and stable compared with the previous quarter (at 3%).

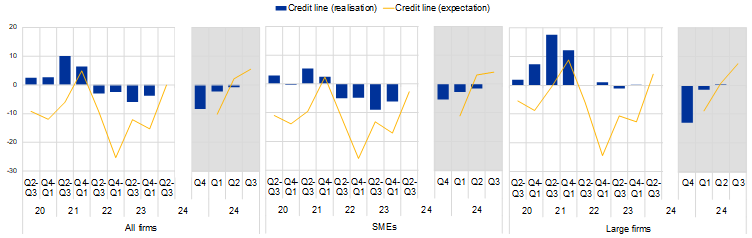

Firms’ needs for credit lines remained stable, while availability continued to decline, but less so than in the first quarter of 2024 (Chart 3). In this survey round a net 8% of firms reported increased needs for credit lines (as in the first quarter of 2024), while continuing to signal a decline in availability (-1%, up from -2%). As a result, the financing gap for credit lines (5%) remained positive and higher than for bank loans and trade credit.

Chart 3

Changes in euro area enterprises’ financing needs and the availability of trade credit and credit lines

(net percentages of respondents)

Base: Enterprises for which the instrument in question is relevant (i.e. they have used it or considered using it). Respondents replying “not applicable” or “don’t know” are excluded. The figures refer to rounds 23 to 31 of the survey (April-September 2020 to April-June 2024).

Notes: For a description of the indicator, see the notes to Chart 2. The data included in the chart refer to Questions 5 and 9 of the survey. The grey areas represent responses to the same question within a reference period of three months, whereas the main charts cover a reference period of six months.

2.3 Firms expect the availability of external financing to improve further

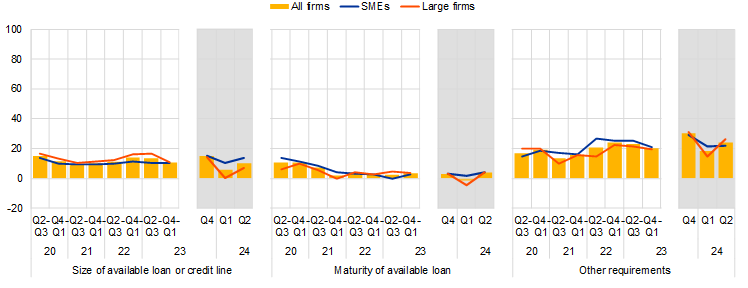

Looking ahead, firms are more optimistic about the availability of external financing over the next three months (Chart 4). A net 7% of firms expect access to bank loans to improve over the next three months, while 6% expect an improvement in credit lines and 4% in trade credit. Compared with large firms, fewer SMEs expect to see an improvement in bank loans and credit lines. By contrast, SMEs are slightly more optimistic on the future availability of trade credit. Likewise, firms also expect the availability of internal funds to increase.

Chart 4

Changes in euro area enterprises’ expectations regarding the availability of financing

(net percentages of respondents)

Base: Enterprises for which the instrument in question is relevant (i.e. they have used it or considered using it). The figures refer to rounds 23 to 31 of the survey (April-September 2020 to April-June2024).

Notes: See the notes to Chart 1. The data included in the chart refer to Question 9 and 23 of the survey. The expectation line has been shifted forward by one period to allow for a direct comparison with realisations. The grey areas represent responses to the same question within a reference period of three months, whereas the main charts cover a reference period of six months.

2.4 Fewer enterprises perceived the general economic outlook as negatively affecting the availability of external finance

Firms perceived the general economic outlook as the main factor hampering the availability of external financing, albeit to a much lesser extent than in the previous survey round (Chart 5). In the second quarter of 2024 a net 12% of firms reported that a deterioration in the general economic outlook had reduced the availability of external financing, down from a net 26% in the first quarter of 2024. In this survey round large firms were less pessimistic than SMEs (-3%, down from - 28% in the previous quarter) in reporting a deterioration in the availability of external financing due to the general economic outlook (compared with -16% of SMEs, down from -24%). On average, firms did not indicate any change in the impact of their firm-specific outlook on the availability of external financing, in contrast with a net 5% indicating a deterioration in the first quarter of 2024. While a net 3% of SMEs continued to signal a deterioration in their firm-specific outlook, down from 6% in the first quarter of 2024, a net 7% of large firms reported an improvement (up from -2%). Firms continued to signal an improvement in their own capital position (net 10%) and creditworthiness (net 14%)

Chart 5

Changes in factors that have an impact on the availability of external financing to euro area enterprises

(net percentages of respondents)

Base: All enterprises. The figures refer to rounds 23 to 31 of the survey (April-September 2020 to April-June 2024).

Notes: See the notes Chart 1. The data included in the chart refer to Question 11 of the survey. The grey areas represent responses to the same question within a reference period of three months, whereas the main charts cover a reference period of six months.

Firms reported an increase in the willingness of banks to lend (Chart 6). On balance, 9% firms reported an improvement in banks’ willingness to lend, up from 4% in the previous survey round, with both SMEs and large firms signalling a better attitude of banks towards them. At the same time, firms reported that business partners were slightly more willing to provide trade credit (a net total of 6%, up from 5% the previous round), with similar percentages across size classes.

Chart 6

Changes in factors that have an impact on the availability of external financing to euro area enterprises

(net percentages of respondents)

Base: All enterprises; for the category “willingness of banks to lend”, enterprises for which at least one bank financing instrument (credit line, bank overdraft, credit card overdraft, bank loan or subsidised bank loan) is relevant. The figures refer to rounds 23 to 31 of the survey (April-September 2020 to April-June 2024).

Notes: See the notes to Chart 1. The data included in the chart refer to Question 11 of the survey. The grey areas represent responses to the same question within a reference period of three months, whereas the main charts cover a reference period of six months.

2.5 Few firms applied for bank loans, while overall financing obstacles are slightly on the decline

Firms continued to report low applications for bank loans (Chart 7). In the second quarter of 2024 the share of applications for bank loans stood at 19% (up from 17%) for all firms, 14% for SMEs and 25% for large firms, while fewer firms felt discouraged from applying for bank loans (2%, compared with 3% the previous quarter). The most common reason stated by firms for not applying is the amount of internal funds at their disposal, which firms consider sufficient to finance their business plans. In this survey round, 51% of firms were signalling this reason (52% the previous quarter), with no differences across size classes.

Chart 7

Applications for bank loans by euro area enterprises

(percentages of respondents)

Base: Enterprises for which bank loans (including subsided bank loans) are relevant. The figures refer to rounds 23 to 31 of the survey (April-September 2020 to April-June 2024).

Notes: The data included in the chart refer to Question 7A of the survey. The grey areas represent responses to the same question within a reference period of three months, whereas the main charts cover a reference period of six months.

The percentage of firms reporting obstacles to obtaining a bank loan remained low and stable (Chart 8). Among firms that considered bank loans to be relevant for their enterprise, 4% reported obstacles when seeking to obtain a loan, with 6% for SMEs and 2% for large firms. All percentages were broadly in line with those reported in the first quarter of 2024. In a long-term perspective, financing obstacles perceived by firms seem to have stabilised, with persistently higher obstacles for SMEs than large firms. Discouraged borrowers (firms that do not apply for bank loans even if they need them) represent the largest fraction of firms facing financing obstacles (2% of all firms in the current survey round), mostly among SMEs.

Chart 8

Obstacles to obtaining a bank loan

(percentages of respondents)

Base: Enterprises for which bank loans (including subsidised bank loans) are relevant. The figures refer to rounds 23 to 31 of the survey (April-September 2020 to April-June 2024).

Notes: Financing obstacles are defined here as the total of the percentages of enterprises reporting (i) loan applications that resulted in an offer that was declined by the enterprise because the borrowing costs were too high, (ii) loan applications that were rejected, (iii) a decision not to apply for a loan for fear of rejection (discouraged borrowers), and (iv) loan applications for which only a limited amount was granted. The grey areas represent responses to the same question within a reference period of three months, whereas the main charts cover a reference period of six months.

3 The economic situation of euro area firms

3.1 Turnover increased modestly, with costs still weighing on profitability

More enterprises reported an increase in turnover over the last three months (Chart 9). The net percentage of euro area firms reporting an increase in turnover jumped to 8% (up from 3% in the first quarter of 2024), reflecting the ongoing pick-up in economic activity in the euro area. Across firm sizes, a net 4% of SMEs reported an increase in turnover (up from 3% reporting a decline the previous quarter), while the net percentage of large firms signalling an increase rose further (to 15% from 12%). Looking forward, firms are optimistic about future turnover, with 24% of them expecting net increases over the next three months.

Chart 9

Changes in the economic situation of euro area enterprises

(net percentages of respondents)

Base: All enterprises. The figures refer to rounds 25 to 31 of the survey (April-September 2021 to April-June 2024).

Notes: See the notes to Chart 1. The data included in the chart refer to Question 2 of the survey. The grey areas represent responses to the same question within a reference period of three months, whereas the main charts cover a reference period of six months.

Euro area firms continued to report a deterioration in their profits, but less than the previous quarter. The net percentage of euro area enterprises that signalled a decline in their profits was somewhat below that in the first quarter of 2024 (-10%, compared with -19%). SMEs seem to be facing greater profitability issues. More SMEs continued to report lower profits (-15%, down from -22% the previous quarter) than large firms (-2%, down from -13% the previous quarter).

The lower deterioration in profitability reflects the fact that fewer firms indicated cost pressures in net terms, including on the labour side. A net 53% of firms reported higher labour costs (down from 66% the previous quarter), while the net share of firms indicating rising costs for materials and energy declined to 44% (from 58% the previous quarter).

Increasing interest expenses are still affecting profitability, though their impact is gradually diminishing. The net share of firms reporting increased interest expenses declined to 19% (from 27%), with large firms (21%) being slightly more affected than SMEs (19%). Looking at a longer horizon, the pressure stemming from interest expenses remains high, but the downward path signals that the impact of past monetary policy tightening is gradually fading.

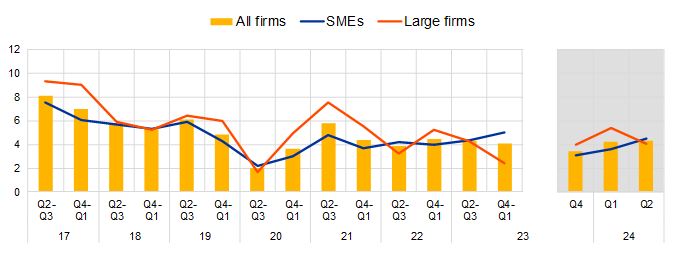

The percentage of financially vulnerable enterprises declined further (Chart 10). The financial vulnerability indicator, which provides a comprehensive picture of firms’ financial situation, suggests that 5% of euro area enterprises encountered major difficulties in running their business and servicing their debts over the past three months (down by 2 percentage points from the previous quarter).[5] At the other end of the spectrum, the share of financially resilient firms (those that are more likely to withstand adverse shocks) remained unchanged at 4%.

Chart 10

Vulnerable and financially resilient firms in the euro area

a) Vulnerable firms

(percentages of respondents)

b) Financially resilient firms

(percentages of respondents)

Base: All enterprises. The figures refer to rounds 17 to 31 of the survey (April-September 2017 to April-June 2024).

Notes: For a definition of “vulnerable firms” and “resilient firms”, see footnote 6 The data included in the chart refer to Question 2 of the survey. The grey areas represent responses to the same question within a reference period of three months, whereas the main charts cover a reference period of six months.

Box 1

Average hours worked and other employment-related outcomes

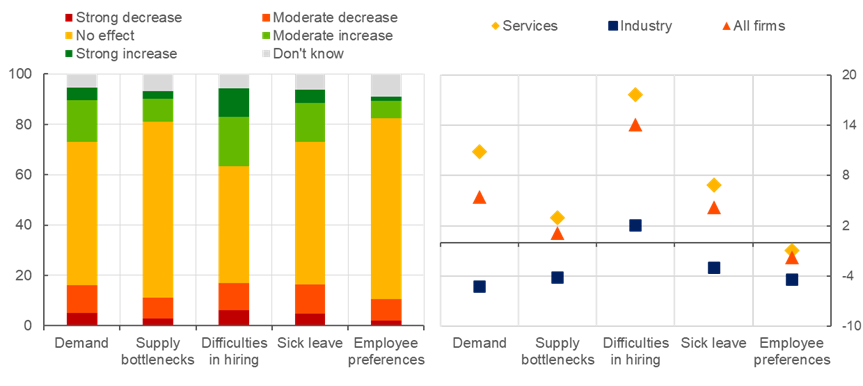

This box examines the changes in average hours worked and firms’ other employment-related outcomes, with a focus on sectoral heterogeneities. To understand labour market developments in the euro area better, a new set of ad hoc questions was introduced in this survey round. While the survey regularly asks about employment and expected wages, in this wave firms were also asked about the developments in average hours worked over the second quarter of 2024. They also indicated the role of various factors contributing to recent developments in average hours: (1) the demand for own products and services, (2) supply chain bottlenecks and energy costs, (3) difficulties in hiring staff, (4) sick leave and other employee health considerations, and (5) employees’ preferences regarding work, not related to health considerations.

A small share of firms in net terms indicated an increase in average hours worked over the second quarter of 2024, albeit with significant heterogeneity across sectors (Chart B). A net 2% of firms indicated an increase in average hours worked in the second quarter of 2024.[6] Across sectors, a net 10% of firms indicated a decrease in average hours worked in industry and a net 7% indicated an increase in services. Across firm sizes, SMEs reported broadly no change in average hours worked, while a small net percentage of large firms signalled an increase (1% for SMEs and 3% for large firms).

Chart B

Change in average hours worked

(net percentages of respondents)

Base: All enterprises.

Notes: Firms were asked to indicate whether average hours increased, remained unchanged or decreased over the second quarter of 2024.

Firms report that recent changes in average hours worked are mainly associated with the demand for their own products and services and difficulties in hiring labour, especially in the services sector (Chart C). A net 5% of firms indicated that demand conditions had had an increasing impact on average hours worked, while 14% indicated that labour shortages, and 4% indicated that sick leave taken by employees had contributed to an increase in average hours worked. Supply bottlenecks had broadly had no impact (1%), whereas employee preferences had a small negative impact on average hours worked (-2%). In services, 11% of firms indicated a positive contribution to average hours worked from demand, whereas firms in industry indicated a decreasing impact in net terms (-5%). Difficulties in hiring workers contributed to an increase in average hours worked for 18% of the service sector firms in net terms, whereas in industry this factor had a positive contribution for only 2% of firms in net terms.

Chart C

Factors contributing to changes in average hours worked

(left: percentages; right: net percentages of respondents)

Base: All enterprises.

Notes: Firms were asked to indicate the extent to which the demand for products or services, supply chain bottlenecks and energy costs, difficulties in hiring staff, sick leave and other employee health considerations, and employees’ preferences regarding work, not related to health considerations had an impact on average hours worked. The panel on the left shows the share of firms indicating a strongly decreasing/moderately decreasing/no effect/moderately increasing/strongly increasing contribution to average hours worked from these factors. The panel on the right shows the contribution from each factor on balance, by pooling strong and moderate decreases (increases) when calculating the net percentage.

Firms indicating an increase in average hours in the second quarter of 2024 are also more positive about past and future developments in employment and expected wages (Chart D). A net 43% of firms with increasing average hours also increased their employment over the past quarter, whereas a net 29% of firms with decreasing average hours decreased their employment. These developments are similar across services and industry. Moreover, firms with an increase in average hours in the second quarter of 2024 expect an increase in employment one year ahead too (a 3% increase on average), whereas firms with a decrease in average hours expect a small decrease in expected employment (-0.6% on average). Services firms with increasing average hours expect an even stronger increase in employment over the next 12 months (3.9%), whereas firms with decreasing hours in services expect unchanged employment. The differences between the groups of firms with increasing and decreasing average hours are also apparent in terms of expected wages, mostly due to developments in the services sector. While a small share of firms indicated net increases in average hours overall, the survey-based findings confirm the labour market remains robust, especially in services.

Chart D

Average hours worked, employment and wages

(left: net percentages of respondents; middle and right: percentage change over the next 12 months)

Base: All enterprises.

Notes: The chart focuses on firms which indicated an increase in average hours worked and those which indicated a decrease over the second quarter of 202. For these firms the chart shows the net percentage for changes in employment and the expected percentage change in employment and wages over the next 12 months, including a sectoral breakdown.

3.2 Investment activity recovered; with a similar increase expected in the third quarter

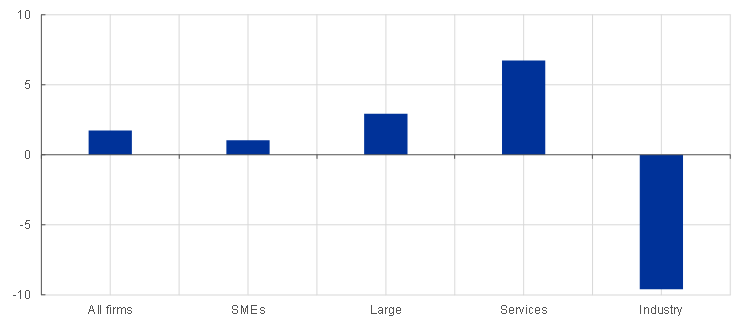

Enterprises reported a further pick-up in investment over the last three months (Chart 11). The net share of firms reporting a rise in investment went up to 9% in the second quarter of 2024, from 5% the previous quarter, with large firms reporting the biggest increase. When asked about investment in the coming quarter, firms across size classes signalled a similar increase over the next three months.

Chart 11

Changes in realised and expected fixed investments of euro area enterprises

(net percentages of respondents)

Base: All enterprises. The figures refer to rounds 23 to 31 of the survey (April-September 2020 to April-June 2024).

Notes: See the notes to Chart 1. Bars refer to developments over the preceding six months and lines to expectations over the next six months. The data included in the chart refer to Questions 2 and 26 of the survey. The expected investment line is shifted by one period to compare with realisations. The question on expected investments was first included in the questionnaire covering the second and third quarters of 2023.The grey areas represent responses to the same question within a reference period of three months, whereas the main charts cover a reference period of six months.

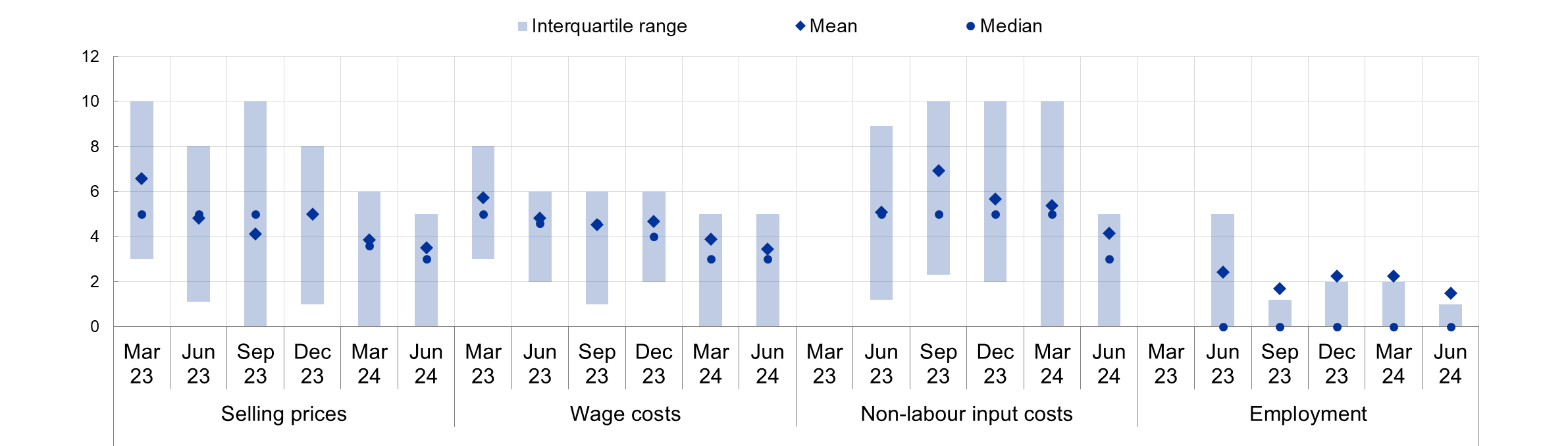

3.3 Firms expect the growth of their selling prices and wages to moderate further over the next year

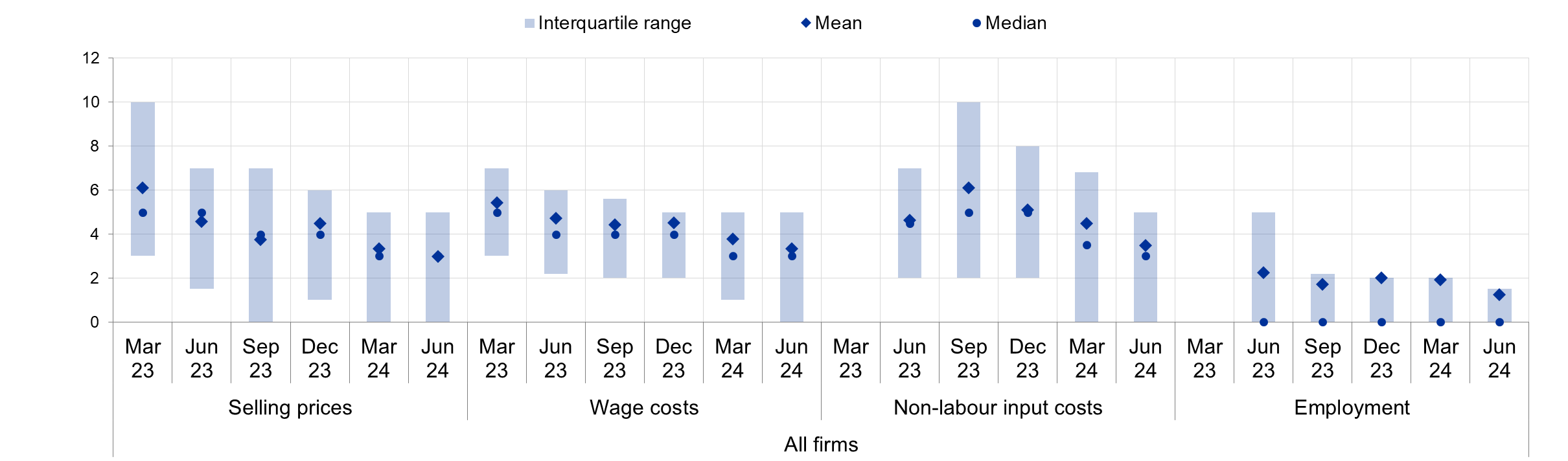

Firms expect their selling prices to increase by 3% on average over the next 12 months (down from 3.3% in the previous survey round), while the corresponding number for wages is 3.3% (down from 3.8%; Chart 12). Average selling price and wage expectations both remained unchanged at 3%. The dispersion of selling price expectations remained stable, with at least one-quarter of firms in the survey continuing to expect prices not to increase over the next year.[7]

Both SMEs’ and large firms’ expectations about selling price and wage increases over the next year have eased compared with the previous survey round. On average, SMEs expect higher increases than large firms, both in their selling prices (3.5%, compared with 2%) and wage costs (3.5%, compared with 3.2%) over the next year (Chart 13). Across sectors, firms in the services sector expect, on average, both higher selling prices and wage costs than firms in industry over the next 12 months (3.6%, compared with 2.4% for selling prices and 3.6%, compared with 3.1% in wage costs).

Chart 12

Expectations for selling prices, wages, input costs and employees one year ahead

(percentage change over the next 12 months)

Base: All enterprises. The figures refer to: round 28 (October 2022-March 2023), pilot 1 (March-June 2023), round 29 (April-September 2023), pilot 2 (October-December 2023), round 30 (January-March 2024) and round 31 (April-June 2024) of the survey, with firms’ replies collected in the last month of the respective survey waves.

Notes: Mean and median euro area firm expectations of changes in selling prices, wages of current employees, non-labour input costs and number of employees for the next 12 months, along with interquartile ranges, using survey weights. The statistics are computed after trimming the data at the country-specific 1st and 99th percentiles. The data included in the chart refer to Question 34 of the survey. Questions on non-labour input costs and employees were not available in round 28.

Chart 13

Expectations for selling prices, wages, input costs and employees one year ahead, by size class

a) SMEs

(percentage change over the next 12 months)

b) Large firms

(percentage change over the next 12 months)

Base: All enterprises with fewer than 250 employees (panel a) and all enterprises with 250 or more employees (panel b). The figures refer to: round 28 (October 2022-March 2023), pilot 1 (March-June 2023), round 29 (April-September 2023), pilot 2 (October-December 2023), round 30 (January-March 2024) and round 31 (April-June 2024) of the survey, with firms’ replies collected in the last month of the respective survey waves.

Notes: Mean and median euro area firm expectations of changes in selling prices, wages of current employees, non-labour input costs and number of employees for the next 12 months, along with interquartile ranges, using survey weights. The statistics are computed after trimming the data at the country-specific 1st and 99th percentiles. The data included in the chart refer to Question 34 of the survey. Questions on non-labour input costs and employees were not available in round 28.

Comparing developments across sectors (Chart 14), firms in services expect their selling prices and wages to increase more than in other sectors (3.6% in services compared with 2.4% in sectors excluding services for selling prices and 3.6% compared with 3.1%, respectively, for wage increases).

Chart 14

Average expectations for selling prices, wages and input costs one year ahead, by sector

(percentage change over the next 12 months)

Base: All enterprises. The figures refer to: round 28 (October 2022-March 2023), pilot 1 (March-June 2023), round 29 (April-September 2023), pilot 2 (October-December 2023), round 30 (January-March 2024) and round 31 (April-June 2024) of the survey, with firms’ replies collected in the last month of the respective survey waves.

Notes: Mean euro area firm expectations of changes in selling prices, wages of current employees, non-labour input costs and number of employees for the next 12 months, along with interquartile ranges, using survey weights. The statistics are computed after trimming the data at the country-specific 1st and 99th percentiles. The data included in the chart refer to Question 34 of the survey. Questions on non-labour input costs and employees were not available in round 28.

Firms expect their non-labour input costs to increase by 3.5% on average over the next year, with enterprises in the services sector predicting higher increases (Chart 12 and Chart 14). In this survey round the distribution of the expected average increase in non-labour input costs is less dispersed, as firms in the highest part of the distribution reported lower increases in non-labour input cost expectations compared with the previous survey round (5%, down from 6.8%). SMEs expect a higher increase in non-labour input costs than large firms (4.2%, compared with 2.3%). The median firm expects non-labour input costs to rise by 3%, with the median expectation of SMEs standing at 3% and of large firms at 2%.

On average, firms expect their staffing levels to increase by 1.3% over the next year, while the median firm expects zero growth (Chart 12 and Chart 14). This reflects the fact that the distribution of expected changes in staffing levels is skewed to the upside, with some firms expecting larger increases but most expecting modest increases or no change. The average expected workforce growth for SMEs is slightly higher than for large firms (1.5%, compared with 0.8%), while across sectors, the increase in expected employment is larger in the services sector than in other sectors (1.8%, compared with 0.8%).

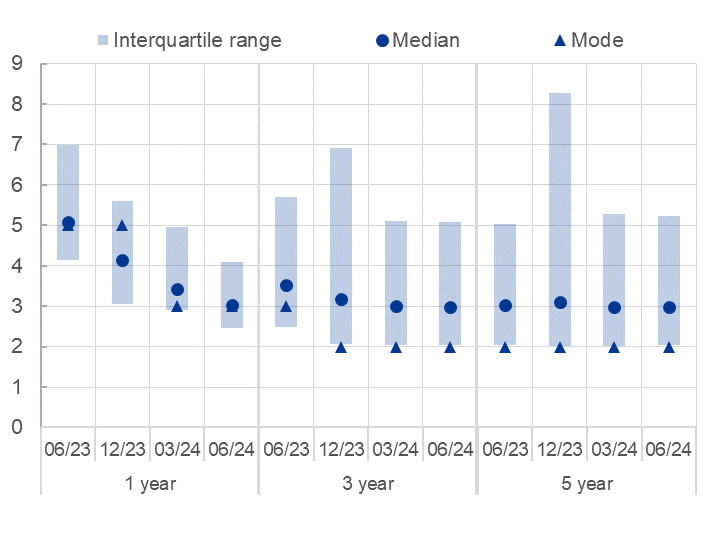

3.4 Firms’ inflation expectations continue to decline

Euro area firms’ median inflation expectations continued to decline to 3% on the one-year horizon (Chart 15). Compared with March 2024, median inflation expectations fell 0.4 percentage points on the one-year horizon and remained at 3% for longer horizons. The continued easing of short-term inflation expectations is consistent with the disinflationary process observed. In the services sector, median inflation expectations were 3.1%, 3% and 3.1% at the one-, three- and five-year horizons, whereas the comparable figures for industry are 3%, 2.5% and 2.5%. The mode of one-year-ahead inflation expectations continued to stand at 3% in June 2024, whereas for longer horizons it remained at 2%.

In addition to lower expectations, the dispersion declined at the one-year horizon. The dispersion in inflation expectations, measured by the interquartile range, decreased from 2 percentage points in March 2024 to 1.6 percentage points in June 2024 for one-year-ahead inflation expectations. At the one-year horizon, median inflation expectations are similar in the services sector as in industry, while dispersion is higher in the services sector. The range of views on longer-term inflation expectations narrowed only slightly.

Chart 15

Firms’ expectations for euro area inflation at different horizons

(annual percentages)

Base: All enterprises.

Notes: Survey-weighted median, mode and interquartile ranges of firms’ expectations for euro area inflation in one year, three years and five years. Quantiles are computed by linear interpolation of the mid-distribution function. The statistics are computed after trimming the data at the country-specific 1st and 99th percentiles.

Firms report that the risks to the five-year-ahead inflation outlook are tilted to the upside, with slightly more SMEs reporting upside risks (Chart 16). 50% of firms find it more likely that five-year-ahead inflation will turn out above rather than below their point prediction. 37% of firms perceive balanced risks and 10% perceive mainly downside risks. While SMEs and large firms perceive the risks to the inflation outlook relatively similarly, slightly more SMEs (52%) report upside risks than large firms (48%). Large firms report more often that the risks to the inflation outlook are balanced. For all firm categories, these shares are similar to the ones observed in March 2024.

Firms with relatively high point predictions for inflation also perceive upside risks more often (Charts 17). Of the firms that expect inflation in five years to turn out above 5% − meaning at levels much higher than currently observed − 61% perceive that the risks to their outlook are tilted to the upside. By contrast, firms that expect inflation to be between 0% and 2% in five years’ time perceive the risks to their inflation outlook to be relatively more balanced: 40% of those firms perceived mainly upside risks and 47% balanced risks in June 2024.

Chart 16

Firms’ perceived risks about euro area inflation five years ahead, by firm size

(weighted percentages)

Base: All enterprises. The figures refer to round 30 (January-March 2024) and round 31 (April-June 2024) of the survey.

Notes: Survey-weighted percentages of firms’ subjective inflation outlook over the next five years. Firms that answered “don't know” in Question 31 are not considered. The data included in the chart refer to Question 33 of the survey.

Chart 17

Firms’ perceived risks about euro area inflation five years ahead, by inflation point forecast

(weighted percentages)

Base: All enterprises. The figures refer to round 30 (January-March 2024) and round 31 (April-June 2024) of the survey.

Notes: Survey-weighted percentages of firms’ subjective inflation outlook over the next five years. Firms that answered “don't know” in Question 31 are not considered. The data included in the chart refer to Questions 31 and 33 of the survey.

Annexes

Annex 1

Descriptive statistics for the sample of enterprises

Chart 18

Breakdown of enterprises by economic activity

(unweighted percentages)

Base: The figures refer to round 31 of the survey (April-June 2024).

Chart 19

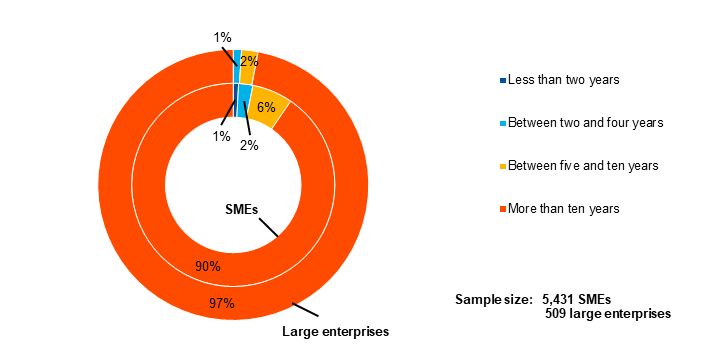

Breakdown of enterprises by age

(unweighted percentages)

Base: The figures refer to round 31 of the survey (April-June 2024).

Chart 20

Breakdown of enterprises by ownership

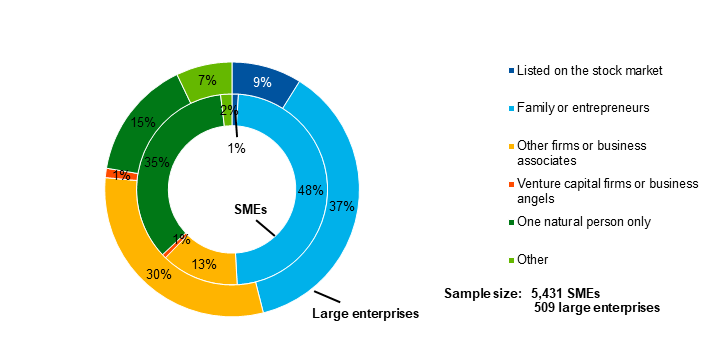

(unweighted percentages)

Base: The figures refer to round 31 of the survey (April-June 2024).

Chart 21

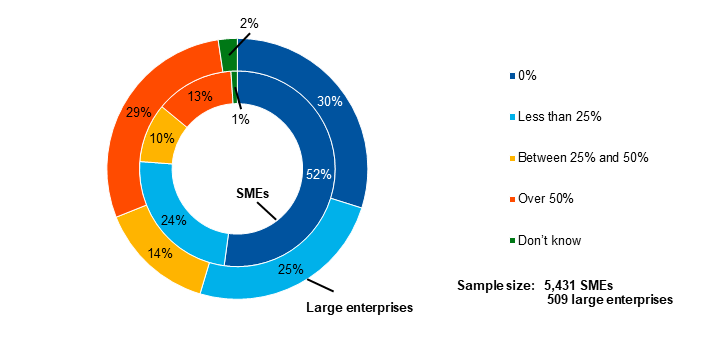

Breakdown of enterprises by exports

(unweighted percentages)

Base: The figures refer to round 31 of the survey (April-June 2024).

Annex 2

Methodological information on the survey

For an overview of how the survey was set up, the general characteristics of the euro area enterprises that participate in the survey and the changes introduced to the methodology and the questionnaire over time, see the “Methodological information on the survey and user guide for the anonymised micro dataset”, which is available on the ECB’s website.[8]

Starting from this round, a shorter questionnaire will be used for the waves in Q2 and Q4. Questions Q0b, Q32 and Q6A were removed. In addition, items f, h, j, m, r and p were removed from question Q4; items c, d, g and h were removed from question Q5; item c was removed from questions Q7A and Q7B; item h was removed from question Q11; items c, d, g and h were removed from question Q9; and item j was removed from question Q23.[9]

In this round, the three-month reference period was asked of the entire sample.

Two ad hoc questions were added in the second quarter of 2024 on hours worked: i) Have the average hours actually worked by employees in your enterprise increased, remained unchanged or decreased during the current quarter? ii) To what extent have the following factors affected the average hours worked during the current quarter? (strong decrease, moderate decrease, no effect, moderate increase and strong increase) 1. Demand for your products or services, 2. Supply chain bottlenecks and energy costs, 3. Difficulty to hire staff, 4. Sick leave and other employee health considerations, 5. Employees’ preferences regarding work, not related to health considerations.

© European Central Bank, 2024

Postal address 60640 Frankfurt am Main, Germany

Telephone +49 69 1344 0

Website www.ecb.europa.eu

All rights reserved. Reproduction for educational and non-commercial purposes is permitted provided that the source is acknowledged.

For specific terminology please refer to the ECB glossary (available in English only).

PDF ISSN 1831-9998, QB-AP-24-002-EN-N

HTML ISSN 1831-9998, QB-AP-24-002-EN-Q

This structure will be repeated in the fourth quarter of 2024, while in the third quarter of 2024 and the first quarter of 2025, the sample of firms will be complete again (covering around 17,000 European firms in the third quarter and around 12,000 euro area firms in the first quarter of 2025). In these two survey rounds, one-half of the firms will be surveyed about developments over the previous six months, the other half over the previous three months; the questionnaire will be the usual extended one. These different structures should help to maintain the internal consistency and the time series of the SAFE at semi-annual frequency.

See Annex 3 for details of methodological issues relating to the survey.

The net percentages indicated in this report are defined as the difference between the percentage of enterprises reporting that an indicator has increased and the percentage reporting that it has declined. Companies are not asked in any of the questions to provide answers adjusted for inflation (but are instead asked to provide answers in volume rather than value terms).

The indicator is derived from a factor analysis covering changes in (i) price terms and conditions of bank loans (changes in interest rates and other costs of bank loans); (ii) non-price terms and conditions (changes in collateral requirements); (iii) the financial position of firms (in terms of changes in profits, credit history and own capital); and (iv) firms’ perceptions of changes in the willingness of banks to provide credit. The reported indicator is one of three main principal components and mainly relates to price terms and conditions. The analysis detects two other principal components, namely (i) the financial position of firms, and (ii) non-price terms and conditions. For a detailed description of the indicator, see the box entitled “Financing conditions through the lens of euro area companies”, Economic Bulletin, Issue 8, ECB, 2021.

Vulnerable firms are defined as firms that simultaneously report lower turnover, decreasing profits, higher interest expenses and a higher or unchanged debt-to-assets ratio or a subset of those conditions and reply to the rest with “do not know”. Financially resilient firms are those that simultaneously report higher turnover and profits, lower or no interest expenses and a lower or no debt-to-assets ratio or a subset of those conditions and reply to the rest with “do not know”. See the box entitled “Distressed and profitable firms: two new indicators on the financial position of enterprises”, Survey on the Access to Finance of Enterprises in the euro area, October 2017 to March 2018, ECB, June 2018.

Around 70% of firms indicated no change in average hours worked in the second quarter of 2024.

The share of firms expecting non-positive price changes was 34% in this round, 33% in March 2024, 24% in December 2023, 30% in September 2023, 22% in June 2023 and 17% in March 2023.

The questionnaire is available on the ECB’s website. It has been translated into various languages for the purposes of the survey.

-

15 July 2024