Published as part of the ECB Economic Bulletin, Issue 7/2022.

This box provides an analysis of recent developments in trade and financial linkages between the euro area and Russia as recorded in the euro area balance of payments. Euro area trade and financial linkages with Russia are in the spotlight due to Russia’s invasion of Ukraine and the sanctions that have subsequently been imposed on Russia by the European Union (EU) as well as the United States and other countries. This box documents how the record deficit in the trade balance between the euro area and Russia – due to steep price increases for imported energy and lower exports amid EU sanctions – contributed to a sizeable shift in the euro area’s overall current account balance. Moreover, it documents how bilateral financial linkages, which were already limited prior to the invasion, were affected by the impact of sanctions and volatility in financial markets.

Current account

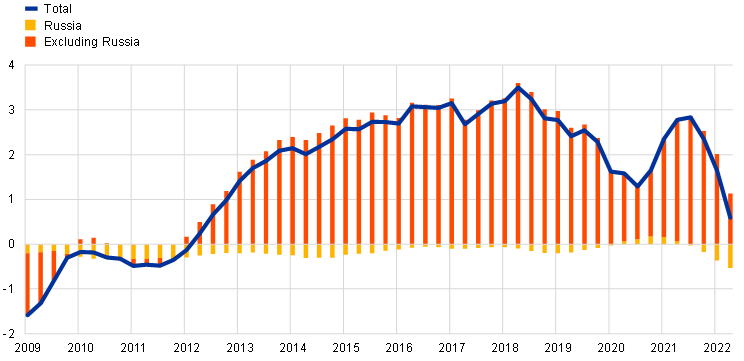

The euro area current account balance vis-à-vis Russia turned from a small surplus into a deficit of 0.5% of euro area GDP between the second quarter of 2021 and the second quarter of 2022, thus contributing significantly to the sharp reduction in the euro area’s current account surplus over the same period (Chart A). Due to Russia’s role as a major exporter of energy products and other commodities, the euro area has typically recorded a current account deficit vis-à-vis Russia. The bilateral deficit was largest over the period 2010-14 when it averaged 0.3% of euro area GDP, as energy prices were at elevated levels. The deficit started to trend downwards thereafter, averaging 0.1% of GDP over the period 2015-19, before turning into a small surplus in 2020 in line with reduced energy imports during the coronavirus (COVID-19) pandemic. However, in the first quarter of 2022 the bilateral current account balance recorded – in annual terms – a deficit in excess of 0.3% of euro area GDP for the first time since 2014. The deficit increased further to 0.5% of GDP in the second quarter of 2022, constituting the historically largest euro area deficit vis-à-vis Russia and the euro area’s second largest bilateral deficit in that quarter, exceeded only by the deficit vis-à-vis China (which reached 1% of euro area GDP).[1] Overall, the worsening of the euro area’s bilateral current account balance with Russia between the second quarter of 2021 and the second quarter of 2022, amounting to 0.6 percentage points of GDP, accounted for about a quarter of the narrowing of the euro area current account surplus from 2.8% to 0.6% of GDP over that period.

Chart A

(four-quarter cumulated flows, percentage of GDP)

Sources: ECB and Eurostat.

The bilateral current account deficit vis-à-vis Russia increased on account of the rising value of nominal imports, largely in the form of energy products, and the fall in exports driven by the EU sanctions (see Chart B).[2] Energy imports from Russia were the primary contributor to the worsening of the bilateral current account balance, as the value of energy imports reached 1% of euro area GDP in the first half of 2022 – almost doubling year on year. This was driven by the surge in energy prices leading to rising nominal imports, despite the fact that lower quantities were imported from Russia: at the end of Q2 2022, values for energy imports were 60% above 2021 average levels, while volumes were 16% below them.[3] In addition, the value of non-energy goods and services imports from Russia also rose in the first half of 2022 amid increasing prices. At the same time, euro area goods and services exports to Russia decreased sharply in the first half of 2022 as the EU implemented sanction packages against Russia following its invasion of Ukraine, with exports of goods subject to sanctions driving this decline (e.g. electrical machinery and vehicles and transport equipment).[4] In particular, exports of goods to Russia almost halved in value from a multi-year peak of around €21 billion in the last quarter of 2021 to a historical low of around €11 billion in the second quarter of 2022[5], underpinned by a steep decline in the quantities of goods exported. A similar picture emerges for euro area exports of services to Russia, as transport and other business-related services recorded considerable declines in the first half of 2022, while exports of travel services to Russian tourists dropped in the second quarter of 2022, to a low previously only seen in 2020 when movement across borders was severely limited due to the pandemic.

Chart B

Euro area current account vis-à-vis Russia

(quarterly flows, percentage of GDP)

Sources: ECB and Eurostat.

Notes: Euro area imports are shown with a minus sign. Total goods trade is included as published in the ECB’s balance of payments statistics, while energy goods trade is based on Eurostat trade statistics. Income balance includes the balances on primary income (e.g. compensation of employees, dividends and interest) and on secondary income (such as international cooperation and workers’ remittances).

Financial linkages

Euro area financial exposures to Russia before Russia’s invasion of Ukraine were relatively limited, with foreign direct investment (FDI) being the most important component. At the end of 2021 total assets and total liabilities vis-à-vis Russia amounted to less than 4% of euro area GDP, compared to total foreign assets and liabilities of the euro area of close to 250% of GDP (Chart C). FDI accounted for the largest share of bilateral investment[6] (63% and 42% of total assets and liabilities respectively), followed by other investment (19% and 33% of total assets and liabilities respectively) and portfolio investment (16% and 24% of total assets and liabilities respectively).

Chart C

Euro area international investment position vis-à-vis Russia

(end-of-period values, percentage of GDP)

Sources: ECB and Eurostat.

Notes: Euro area liabilities are shown with a minus sign. Bilateral positions in financial derivatives are not shown separately, as data are available only from the end of 2013 and account for a small proportion of bilateral assets and liabilities (less than 0.1% of GDP).

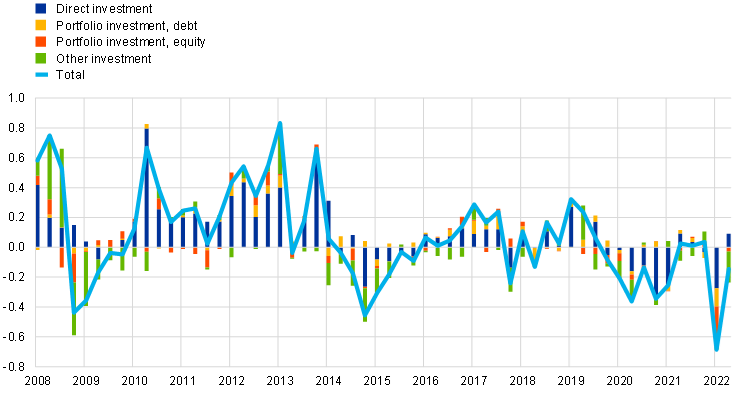

Euro area holdings of Russian assets have declined since the start of the war, while liabilities vis-à-vis Russia have increased due to the impact of EU sanctions. Euro area holdings of Russian assets declined by 10% between the end of the fourth quarter of 2021 and the end of the second quarter of 2022. This drop was mainly due to a reduction in the value of euro area holdings of Russian portfolio investment securities, which decreased by 55% over this period, while other investment assets decreased by 12%. FDI positions remained broadly unchanged as a result of the euro exchange rate changes vis-à-vis the rouble that offset euro area companies’ disinvestment. Over the same period, euro area liabilities vis-à-vis Russia increased by 11%. This was mainly driven by a 28% increase in liabilities in other investment, resulting from the EU sanctions. In particular, the restrictions on payments to Russian residents and asset freezes led to increased deposits in euro area banks vis-à-vis Russian residents as funds owned by Russian residents (e.g. generated by blocked coupon payments and redemptions of securities held in custody in the euro area) were prohibited from being transferred to Russia.[7]

Following Russia’s invasion of Ukraine euro area residents broadly divested from Russian assets (see Chart D). While euro area investors had already started to retrench from Russian assets after the outbreak of the coronavirus (COVID-19) pandemic in 2020 – mainly affecting FDI – the divestment in the first half of 2022 also involved portfolio and other investment. Amid the turbulences in Russian financial markets following Russia’s invasion of Ukraine, euro area residents divested more than €10 billion from Russian portfolio investment equity and debt instruments. Several euro area companies also started to close down and sell their Russian subsidiaries, resulting in net divestments in FDI. Taking a longer term perspective, euro area investors’ activities in Russian assets had already been rather subdued over the past decade, in particular as euro area investors divested from Russian assets in the aftermath of the Russian annexation of Crimea in 2014, which led to several EU sanctions packages.

Chart D

Euro area net purchases of Russian financial assets

(quarterly flows, percentage of GDP)

Source: ECB.

Note: A positive (negative) number indicates net purchases (sales) of Russian instruments by euro area investor.

The bilateral euro area current account series are available since 2008.

See Council of the EU: EU sanctions against Russia explained.

The latest monthly trade in goods data show that volumes of euro area energy imports from Russia continue to decrease sharply, with the volume of energy imports in August 2022 being more than 30% lower than the 2021 average levels.

For details on the effect of sanctions on global trade flows to Russia, see the box entitled “Trade flows with Russia since the start of its invasion of Ukraine”, Economic Bulletin, Issue 5, ECB, 2022.

Comparable drops in the value of euro area goods exports to Russia were also seen in the aftermath of the 2008 financial crisis and the 2014 Crimea invasion, when bilateral euro area exports almost halved compared with previous periods. The decline in exports in the first half of 2022 is however steeper than in these two earlier episodes as the value of euro area exports to Russia halved – reaching a historical low – in just two quarters.

Bilateral euro area FDI figures are strongly affected by the structure of multinational corporations, which often set up holding companies in euro area financial centres, implying a distorted view of the size, geography and economic sectors involved in FDI linkages. Around two-thirds of the bilateral FDI linkages between Russia and the euro area involve Cyprus and the Netherlands, with large bilateral positions both in assets and liabilities, suggesting that entities resident in these two euro area countries are acting as intermediaries within complex FDI arrangements.

For instance, the sanctions affected the balance sheet of financial market infrastructure services provider Euroclear.