- 15 JUNE 2022 · RESEARCH BULLETIN NO. 96

Europe’s growing league of small corporate bond issuers: new players, different game dynamics

While historically only very large firms issued in the European corporate bond market, recent years have seen the entry of many new players: small, private, and unrated issuers. Firm-level data show these new players face different game dynamics. They are disconnected from aggregate market movements and still depend heavily on banks. A better understanding of the differences between new and more established corporate bond issuers could help us identify policy implications for financial stability, capital markets development, and growth.

Introduction

The global rise of bond financing is of particular interest in Europe, as its financial sector has always been heavily bank-based relative to the United States. In the eurozone since 2008, aggregate market financing has been growing significantly faster than bank lending. Policymakers have supported the increase in bond financing as it can help insulate firms from shocks to the banking sector by diversifying sources of funds.

Historically, the European bond market included only the very largest firms. But entry by smaller issuers is increasing. These new players are considered key to achieving a transition from a largely bank-based system towards more capital market funding. To fully understand these changes to the state of play in the bond market, we need to go beyond the aggregate data and dig into the characteristics of these new arrivals. We need to understand how they compare to historical issuers, we need a clear view of who buys their bonds, and we need to know how they can be affected by market disruptions.

To this end, in Darmouni and Papoutsi (2022), we have built a large panel dataset, using two decades of micro-data. We have used this to study the European corporate bond market’s new players: smaller, private, and unrated issuers that have entered the market in recent years.

Focusing on small and first-time bond issuers

Using micro-data enables us to look beyond aggregate growth and unveil firm-level patterns. This is important because, while these new issuers embody the shift towards increased capital market funding, they might be "invisible" in aggregate bond market volume or spreads. Such market indicators tend to be driven by large, public, and rated issuers. Our dataset looks at the detail of debt structure and balance sheets over the past 20 years.

While bank loans still account for the largest share of corporate debt, euro area firms have increasingly resorted to bond financing, especially following the global financial crisis of 2008-09. The outstanding volume of corporate bonds relative to bank borrowing by euro area firms has risen to around 30%, up from roughly 15% in mid-2008 (Cappiello et al., 2021).

We focus on new issuers. This is justified by the number of firms entering the bond market. Every year approximately 10% of issuers were new entrants into the market and entry has accelerated in recent years.

Figure 1

Number of firms entering the euro area corporate bond market per year

Source: Darmouni and Papoutsi (2022)

Notes: This figure presents the total number of new public and private issuers from 2010 to 2021 by year of entry. The sample includes all firms with a non-zero bond outstanding between the period 2018 to 2021. In each year, new issuers are defined as firms that issue bonds for the first time ever in that year. The first year of issuance was obtained by combining data from Capital IQ and the Centralised Securities Database (CSDB): it corresponds to the earliest issue year identifiable for any subsidiary or branch within the group structure of firms in the sample. I.e. for any group, we keep the date of issuance – either identified directly using the variable date of issuance from CSDB or the first year with a non-zero bond volume outstanding in Capital IQ – which corresponds to the earliest issuance date across all entities within the group. Bonds in Capital IQ correspond to the sum of all senior bonds, subordinated bonds and commercial paper. Bonds in the CSDB correspond to debt securities.

These new issuers differ from the historical European bond issuers. They are significantly smaller and mostly tend to be private firms. Most are unrated: they lack a credit rating from one of the three largest rating agencies. This contrasts with the United States, where rating coverage is much wider.

Who buys bonds from small and first time issuers?

It is important to know who is buying which bonds in Europe, as it can shed light on potential fragility of credit supply. While traditional “buy-and-hold” bond investors such as pension funds and insurance companies have a long-term horizon (Becker and Benmelech, 2021), other bond investors such as investment funds can be responsible for fire sales and price dislocation in bad times (Goldstein et al., 2017, Falato et al., 2020).

Figure 2

Investor composition of euro area non-financial corporate bonds

Source: Darmouni and Papoutsi (2022).

Notes: This figure presents the investor composition of the debt securities issued by firms in our sample at the end of 2019. The rest of the world is estimated as the residual amounts held by selected investors in the euro area. Owing to space limitations, in the legend "insurance and pension funds" is shorthand for "insurance corporations and pension funds”. The sources of this data are the ECB Securities Holdings Statistics by Sector and the ECB Securities Holdings Statistics of the Eurosystem.

Figure 2 shows that traditional “buy-and-hold” investors held a large share of the aggregate in 2019. Insurance companies and pension funds held approximately a quarter of the total, and the European Central Bank (ECB) another 10%. Investment funds held 25% and financial institutions and households less than 15%, while the rest of the world covered the final 26%.

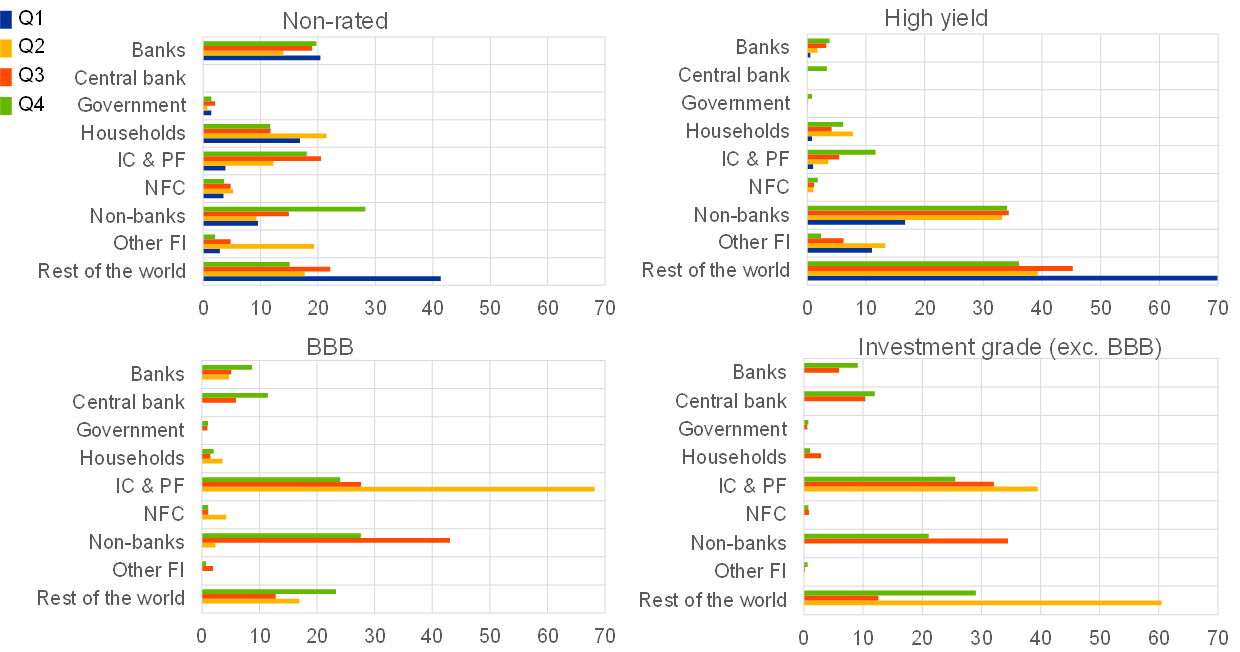

Looking beyond the aggregate data, Figure 3 considers issuers with different ratings and sizes and plots investor composition at the end of 2019. What initially stands out is that, for the largest and investment-grade rated issuers, investor composition is remarkably similar to the aggregate. For instance, insurance companies and pension funds hold about a quarter and the ECB 10%. This is unsurprising, as the largest firms are so much larger that they fully drive the aggregate patterns.

But who holds bonds issued by the European bond market’s new players? Based on Figure 3, investor composition for smaller and unrated issuers is strikingly different. For instance, the share of “buy-and-hold” investors (ECB, insurance companies, pension funds) is only 5% for the smallest issuers, or about 30 percentage points lower than in the aggregate.

We find that banks buy a disproportionate share of the bonds issued by small firms. Traditional banks hold 20% of the smallest and unrated issuers’ bonds in our sample. This is remarkable, as access to the bond market is often considered to be a way to help firms reduce their dependence on banks. The relatively higher share of holdings of corporate bonds by banks suggests that the bank-dependence of this segment of issuers is likely understated. This fact also raises potential concerns about the stability of credit supply to these firms: banks are often thought to be exposed to balance sheet effects in downturns (Becker and Benmelech, 2021). To understand that better, we next turn to studying the effects of the period of turmoil in the credit markets in spring 2020.

Figure 3

Investor composition by rating and size of the firm

Source: Darmouni and Papoutsi (2022).

Notes: This figure presents the investor composition of the debt securities issued by firms in our sample at the end of 2019, broken down by size and rating categories. The sample is divided using firm assets as an approximation for firm size. The firms’ assets grow with each quartile (i.e. the first quartile includes firms with the lowest level of total assets in the sample, while the fourth-quartile firms have the highest level of total assets). The rating categories correspond to “investment grade” (IG) if the rating of the firm is above BBB+, to BBB if the rating is between BBB- and BBB+, “high yield” (HY) if the rating is below BBB-, and “unrated” (NR) if the firm is not rated. The rest of the world is estimated as the residual amounts held by selected investors in the euro area. ECB Securities Holdings Statistics by Sector and the ECB Securities Holdings Statistics of the Eurosystem. The breakdown of ratings of issuers is obtained after collecting data on the ratings of the firms and bonds issued by each firm, from either Standard & Poor’s, Moody’s or Fitch, from the CSDB rating database. Ratings are dynamic over time, i.e. they are computed in each month. The breakdown of the size of issuers is obtained after collecting data on the asset size of all firms in the sample, from Orbis, Capital IQ and RIAD. Quartiles are fixed, i.e. they are computed for asset values in the year 2019. Investors’ shares are expressed in percentages.

The credit market turmoil of spring 2020

In March 2020, at the onset of the coronavirus (COVID-19) pandemic, European corporate bond markets were thrown into turmoil. An investor sell-off led to large spikes in borrowing costs for firms and new issuance drying up. The ECB had to intervene to restore market functioning and allow firms to borrow in the bond market again.

There is a concern that smaller firms with a smaller share of “buy-and-hold” investors might have been disproportionately affected by the investor sell-off. However, our study paints a different picture: it seems that the pullback of bond investors was primarily aimed at the largest, rated issuers. Insurers, pension funds, mutual funds and banks all reduced their holdings of bonds issued by the largest firms. Interestingly, this is consistent with a "reverse flight to quality", where bonds from the largest firms tend to be sold first, because they are more liquid, safer and/or have a lower yield (Falato et al., 2020, Ma et al., 2020, Haddad et al., 2020).

Our findings indicate that only the largest firms tapped the bond market in the subsequent issuance wave from March to December 2020. Smaller and unrated issuers in fact borrowed less through bonds than they had before 2020. If they were able to raise funding at all, it came from the loan market.

Policy implications

Overall, our paper suggests that the new players in the growing “minor league” of the European bond market are largely disconnected from the more established, “top-division” players and still heavily bank-dependent. This evidence has three key policy implications. First, if we rely entirely on aggregate bond market indicators, we might not pick up on what is happening with smaller issuers. Second, the reduction in small issuers’ bank-dependence might have been overstated. Banks are key investors in the market for smaller issuers’ bonds and so accessing the bond market has not diversified these firms’ sources of funds as much as previously thought. Third, interventions aimed at stimulating the bond market might have limited impact on smaller issuers relative to larger, investment grade firms. Overall, looking at European corporate bond markets through the lens of firm-level data reveals striking differences between the major and minor leagues. This can help us better understand issues related to financial stability, capital markets development, and growth.

References

Becker, B., and Benmelech, E. (2021), “The resilience of the U.S. corporate bond market during financial crises”, NBER Working Paper, No 28868, May.

Cappiello, L., Holm-Hadulla, F., Maddaloni, A., Mayordomo, S., Unger, R. et al. (2021), “Non-bank financial intermediation in the euro area: implications for monetary policy transmission and key vulnerabilities”, Occasional Paper Series, No 270, ECB, Frankfurt am Main, December.

Darmouni, O., and Papoutsi, M. (2022), “The rise of bond financing in Europe”, Working Paper Series, No 2663, ECB, Frankfurt am Main, May.

Falato, A., Goldstein, I., and Hortaçsu, A. (2021), “Financial Fragility in the COVID-19 Crisis: The Case of Investment Funds in Corporate Bond Markets”, Journal of Monetary Economics, Vol. 123, pp. 35-52.

Goldstein, I., Jiang, H., and Ng, D. T. (2017), “Investor flows and fragility in corporate bond funds”, Journal of Financial Economics, Vol. 126, Issue 3, pp. 592-613.

Haddad, V., Moreira, A., and Muir, T. (2021), “When Selling Becomes Viral: Disruptions in Debt Markets in the COVID-19 Crisis and the Fed’s Response”, The Review of Financial Studies, Vol. 34, Issue 11, pp. 5309–5351.

Ma, Y., Xiao, K., and Zeng, Y. (2022), “Mutual Fund Liquidity Transformation and Reverse Flight to Liquidity”, The Review of Financial Studies.

This article was written by Olivier Darmouni (Associate Professor, Columbia Business School) and Melina Papoutsi (Senior Economist, Directorate General Research, European Central Bank). The authors gratefully acknowledge the comments of Jonathan Drake, Simone Manganelli, Alexander Popov, and Zoë Sprokel. The views expressed here are those of the authors and do not necessarily represent the views of the European Central Bank or the Eurosystem.