Household inequality and financial stability risks: exploring the impact of changes in consumer prices and interest rates

Published as part of the Financial Stability Review, November 2022.

Since the start of 2022, euro area households have seen the largest increase in consumer prices in decades and the first increase in interest rates in over ten years. For some households – especially those with lower incomes – these shocks could lead to financial distress, including debt defaults. Simulations of the impact of rising consumer prices and interest rates on the near-term financial health of households reveal a more pronounced risk of default in lower income quintiles. For most countries, systemic risk arising from loans originated in lower income quintiles, which represent a lower share of total household debt than loans originated in higher income quintiles, is limited, although it is more significant in others. Policy support aimed at dampening the impact of shocks could help to mitigate this risk. Across the euro area, second-round effects stemming from foregone consumption in response to higher financial burdens could weigh on economic performance and further impair banks’ asset quality.

1 Introduction

During 2022, euro area households have seen the largest increase in consumer prices in decades and the first increase in interest rates in over ten years. Despite the scale of the pandemic’s impact on overall GDP, households have generally experienced relatively benign financial conditions in recent years, supported by declining unemployment, stable incomes and low interest rates. On aggregate, debt service-to-income ratios and household non-performing loan (NPL) ratios have steadily declined since 2015 (Chart B.1, panel a). However, the recent combination of higher core inflation, surging energy prices, high economic uncertainty and increasing mortgage rates could test households’ financial capacity (Chart B.1, panel b).

For some households – especially those with lower incomes – this pressure could lead to financial distress, including debt defaults. Households with smaller financial cushions, for which food and energy costs represent a large share of expenditure, have suffered particularly badly from the high increases in both components in 2022 and could quickly become overburdened. If a sufficiently large number of vulnerable households which also hold debt were to suffer defaults on parts – or even all – of their debt, this could ultimately pose a threat to financial stability. Additionally, significant declines in consumption resulting from the financial squeeze could have a negative feedback effect on economic performance. Governments are therefore considering additional responses over and above normal social transfers.

Chart B.1

Recent stability in euro area households’ financial situation could be tested by sharp increases in energy and consumer prices

Sources: Panel a: Bank for International Settlements, Eurostat, ECB and ECB staff calculations. Panel b: ECB.

Notes: Panel a: household NPLs and Gini coefficients are shown as euro area averages, while the debt service-to-income ratio is the equally-weighted average of eight available euro area countries (Belgium, Germany, Spain, France, Italy, Netherlands, Portugal, Finland) and is defined as the ratio of interest payments plus amortisations to gross income. All values are as at year-end.

This special feature explores financial stability risks from a perspective of household inequality. It takes a granular look at households’ consumer price and interest rate sensitivities, exploiting distributional survey data from the ECB’s Household Finance and Consumption Survey (HFCS). The analysis extrapolates survey data from between 2016 and 2018 forward to the first quarter of 2022 and simulates the impact of consumer price rises and interest rate changes until the end of 2022 on the near-term financial health of households across the income distribution and the overall effect on euro area financial stability.

2 Euro area household spending, debt service and saving by income level

The average lower-income household in the euro area spends a large portion of its income on basic goods and housing. The average middle-income household across the euro area spends roughly 34% of its gross income[2] on essentials – food, energy and housing – leaving room for savings or the purchase of consumer durables like cars. By contrast, the average household in the lowest income quintile spends about 70% on basic needs (Chart B.2, panel a).[3] Thus, a stylised 10% increase in the basic cost of living that is not offset by income growth would translate into a reduction in spending power of just over 20% for the lowest-income households versus around 5% for middle-income households. The disproportionate effect on lower-income households could, in turn, considerably limit their ability to withstand shocks and build up financial safety cushions.

Chart B.2

Lower-income households have little financial room to cushion higher food and energy prices, especially in countries where high debt service levels meet low savings

Sources: HFCS and ECB staff calculations.

Notes: Panel a: expenditure is calculated in relation to gross income, data are extrapolated forward to the first quarter of 2022 and winsorised. Averages are equally weighted across euro area countries. Basic consumption is defined as the amount spent on food at home and utilities (e.g. electricity, gas, water, internet, TV and telephone). Non-basic consumption is defined as all expenditure on consumer goods and services excluding basic consumption. Money spent on consumer durables (e.g. cars or household appliances), the cost of insurance policies and renovation expenses is not included in non-basic consumption. Child and health care expenses are included in non-basic consumption. Not all households rent housing or have debt, meaning that the expenditure shares displayed above are averages across all households within the respective income quintiles. Reported income shares are in line with the ECB’s Consumer Expectations Survey and Eurostat’s European Union Statistics on Income and Living Conditions, while slight discrepancies may occur due to differences in samples, weighting techniques, tax deductions and the treatment of outliers. Panel b: data are extrapolated forward to the first quarter of 2022. Lithuania and Malta are excluded from the first quintile due to data limitations.

Indebted lower-income households, which may now face an increase in debt servicing costs, have only limited savings that could help offset the increase. While a high share of fixed-rate mortgages shields households in many countries from the immediate impact of higher mortgage rates,[4] some countries still have predominately variable-rate mortgages, making households more vulnerable to recent changes in mortgage rates.[5] While indebted lower-income households, which make up around 20% of all lower-income households in the euro area, tend to have high debt service-to-income ratios, in some countries these are offset by savings which could be used in the event of cashflow shortfalls. However, indebted lower-income households tend to spend a high share of their income on servicing debt while holding low volumes of liquid assets (Chart B.2, panel b).[6] The lower the income, the higher the probability of any illiquidity stemming from changes in prices and interest rates translating into debt default.

3 Near-term impact of inflation and rising interest rates

A first step towards assessing the impact more fully is to estimate the current distribution of income and the current composition of spending. Granular analysis of euro area households at different income levels is generally hampered by long lags in data collection.[7] To overcome this, this special feature presents a “forward extrapolation”, assuming a stable overall level of inequality consistent with the euro area income Gini coefficient (Chart B.1, panel a). Each variable of interest (such as income, liquid assets and expenditure) is then adjusted for each individual household by a factor equal to the growth of the country-level macroeconomic aggregates of the respective variables of interest between the reference period of the HFCS and the first quarter of 2022.[8] Separate calculations are used to account for the change to the income distribution induced by the general improvement in employment in recent years, which is not captured by the latest HFCS vintage, and the structural shift towards fixed-rate mortgages in many countries.[9]

These data are used to estimate household-level disposable income, which is gross income after taxes,[10] debt service, basic consumption and rent. Households with disposable income either spend it on non-basic consumption or save it. If disposable income falls below zero, however, households resort to using savings (i.e. liquid assets) to service their debt and maintain basic consumption.[11] If liquid assets cover less than twelve months of debt and basic consumption expenditure, a household has negative disposable income and is considered to be in distress; if liquid assets cover less than one month of debt and basic consumption expenditure, such a household is considered to be illiquid.[12]

Chart B.3

Lower-income households could be disproportionately squeezed by inflation and to a lesser extent by higher interest rates from the end of 2022 onwards

Sources: HFCS and ECB staff calculations.

Notes: Data are extrapolated forward to the first quarter of 2022. Lithuania and Finland are excluded because of insufficient data coverage. “Shock” refers to the impact of changes in consumer prices and interest rates on household finances between the first quarter of 2022 and the end of 2022.

All other things being equal, high inflation could considerably increase the share of distressed households in the lowest income quintile. Country-level and expenditure component-specific inflation rates, together with realised variable-loan mortgage rates up to the third quarter of 2022, are applied as a shock to euro area household data, which are then forecast up to the fourth quarter using the ECB’s September 2022 macroeconomic projections. By the end of 2022, the interest rate and inflation shocks materialise mainly in the lowest income quintile, where the share of illiquid and distressed households rises significantly (Chart B.3, panel a) when disposable incomes are recomputed.

At the same time, the higher income quintiles, which hold most household debt, would see little increase in estimated distress. The remaining disposable income of higher-income households provides sufficient room to absorb higher debt servicing costs and consumption expenditure, likely resulting in slightly lower saving rates or a reduction in non-basic consumption. Generally, higher consumer prices have a stronger impact on household budgets than the interest rate shock, due to the high share of fixed-rate mortgages in many countries which remain unaffected in the near term (Chart B.3, panel b). The share of illiquid households after the shock increases more in countries with a higher initial share of illiquid households and lower savings for lower-income households.

4 Impact on bank asset quality

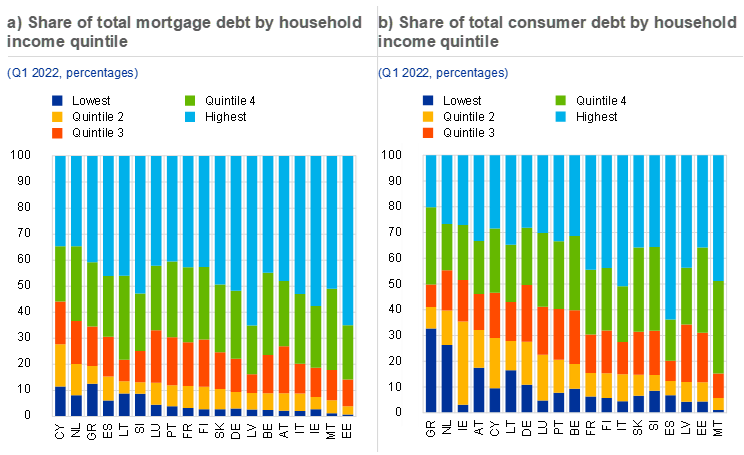

Households are the largest recipient of lending from the euro area’s banking system.[13] As of the second quarter of 2022, collateralised mortgages account for over 75% of household debt on banks’ balance sheets, while mainly uncollateralised consumer loans represent a further 10% or so.[14] In recent years there has been a gradual increase in aggregate nominal household indebtedness, largely driven by very low interest rates and robust housing demand but also supported by income growth and low unemployment. A strong deterioration of households’ financial positions could translate into loan defaults, which would weigh on banks’ asset quality. Thus, a more detailed look at the decomposition of household debt and banks’ exposure across the income distribution is warranted.

More than 70% of euro area households’ bank debt is attributable to higher-income households, compared with around 13% to lower income quintiles. For consumer debt alone, however, which has historically faced substantially higher default rates than mortgages, the share held by the lower income quintiles can be much higher, depending on the country concerned (Chart B.4).[15] Risks would most likely arise in those countries where lower-income households with high debt servicing costs but limited savings – making them particularly vulnerable to the simulated disposable income squeeze and hence most likely to default – hold a relatively large share of the banking system’s debt.

Chart B.4

Household debt is mostly attributable to higher-income households, with some degree of heterogeneity across countries and loan types

Sources: HFCS and ECB staff calculations.

Note: Data extrapolated forward to the first quarter of 2022.

The simulated impact on banks’ asset quality from the end of 2022 is material, albeit from historically low NPL levels, with a downside estimate of the NPL ratio increasing by 80 basis points. Using the estimations described in the section above, both the group of illiquid households and the group of distressed households (Chart B.3) holding debt are assumed to default on their entire loan portfolio, thus increasing banks’ NPL ratios.[16] These two groups each represent a scenario. The default of illiquid indebted households is a baseline scenario for the impact of higher prices and interest rates in 2022, with no real income growth or government assistance to alleviate their situation. Distressed indebted households, on the other hand, have negative cash flows but up to one year of savings to cover their shortfall. Their default represents a downside scenario that can be interpreted as what would happen if there were no offsetting real income growth in 2022 and 2023 and no government assistance.[17] Both scenarios would start to materialise from the end of 2022. To calculate the expected change in NPL ratios, the estimated within-country shares of indebted illiquid and distressed households, as well as the debt dispersion per income quintile and country, are used to calibrate banks’ NPL ratios across countries and to map bank exposures from supervisory data into income quintiles.[18] The resulting country-specific bank NPL ratios are assumed to change in line with the share of illiquid or distressed loans within each income quintile after the shock. The majority of NPLs stem from mortgage loans, reflecting the fact that mortgages are by far the most common type of household loan on banks’ balance sheets. In some countries, however, non-performing consumer loans play a disproportionately large role.[19] In the downside scenario, in which all distressed households default on all their loans, the average NPL ratio could increase by 80 basis points as of year-end 2022 (Chart B.5, panel a).

Lower-income households are the main source of defaults, and increases in NPL ratios may vary across countries. At the same time, more affluent households, which account for the bulk of loans to households, provide only a small portion of new NPLs (Chart B.5, panel b). The significant cross-country heterogeneity in the contribution of different income quintiles to the increases in NPL ratios can be attributed to the different debt shares and savings levels of lower-income households. In the baseline scenario, where all illiquid households default, only few countries would be negatively affected, while in the downside scenario, where all distressed households default, a wider range of countries would see their NPL ratios increase. It should be noted that shocked NPL ratios do not account for structural changes in the distribution of household indebtedness that have occurred between the time of the last HFCS vintage and the first quarter of 2022. Preliminary data indicate that this is particularly relevant for countries which have taken significant action to reduce past and future stocks of NPLs.[20]

Chart B.5

Immediate impact on banks’ NPL ratios is contained but downside risks exist in the form of distressed households

Sources: HFCS, ECB supervisory data and ECB staff calculations.

Notes: Excludes Lithuania, Slovakia and Finland due to insufficient data coverage. NPL ratios after the shock are calculated assuming that all newly illiquid/distressed households default after the shock. “Shock” refers to the impact of changes in consumer prices and interest rates on household finances between the first quarter of 2022 and the end of 2022. Panel b: for each country, the left bar represents illiquid households and the right bar distressed households.

Second-round effects from a consumption-induced economic slowdown in response to surging living costs may pose a challenge going forward. In 2021 household consumption contributed roughly half of the euro area’s total GDP. A recent ECB study exploring the channels of energy price increases and consumption across income distributions estimates that lower-income households reduce their spending on essentials by about 20 basis points for each percentage point increase in energy prices.[21] Additionally, lower-income households are likely to cushion the impact by foregoing new savings and resorting to any existing stock of savings they may have. Should consumption fall more sharply, the resulting lower aggregate private consumption could weigh on GDP. As a result, an economic downturn could become more severe, with potential further second-round effects on banks’ asset quality.

Higher-income households could, however, be subject to risks in the medium to long term, depending on labour market and interest rate developments. In conjunction with rising house prices, the very low interest rates of recent years have allowed many more affluent households to fully exploit their borrowing capacities in many countries. Their debt service capability may come under pressure in the future if (a) the fixation periods of mortgages originated in recent years expire and interest payments are recalculated at potentially much higher interest rates, and (b) unemployment rises or incomes weaken across the income distribution.[22] In several countries, a significant share of higher-income households are low on savings but at maximum debt servicing capacity.

5 Conclusion

Lower-income households have been disproportionately affected by rising consumer prices and interest rates in 2022. Lower-income households spend a much larger share of their income on basic needs, especially energy and food. Since both components have been hit particularly hard by inflation in 2022, lower-income households find themselves in a more vulnerable position. The effect of rising interest rates is, however, less critical in the near term, as a large share of existing loans are at fixed rates. That said, they will have a much greater impact in the medium to long run in the form of higher mortgage rates. The result could be a pronounced increase in the debt service costs for households which have locked in low interest rates in recent years once the fixation periods of their loans expire.

While outright defaults are likely to increase only slightly, the downside risks to banks’ asset quality are increasing, especially in vulnerable countries. Although the fact that most debt is granted to households in the upper income quintiles mitigates systemic risk for banks, significant differences exist across countries. Vulnerability to asset quality deterioration could be a particular issue for banks in countries with a higher share of bank loans to households in the lowerincome quintiles, which are suffering a significant impact from rising inflation and higher interest rates and have lower amounts of liquid assets available.

Second-round effects from a consumption-induced economic slowdown are likely to impose an additional burden on banks’ asset quality. Depending on the outlook for income growth and government assistance, aggregate private consumption may decline in response to higher living costs, thus weighing on GDP, increasing the likelihood of a recession and potentially resulting in higher risks to banks’ asset quality through corporate defaults. Going forward, a prolonged period of high inflation would represent a risk to euro area financial stability as it could exacerbate the income squeeze on households, potentially threatening households with medium and higher incomes as well. Bringing inflation back to its medium-term goal therefore remains of paramount importance.

This special feature has greatly benefited from data transformation support from Pablo Serrano Ascandoni.

As of 2015, and according to OECD data, the median effective tax rate for households in the third gross income quintile was 26.7%. For the lowest quintile, the median rate was 22.0%.

The lowest-income households are defined as the 20% of households with the lowest gross income within each country – the first income quintile. Median-income households are, in turn, defined as those in the third, middle, quintile. Lower-income households are defined as those in the first and second quintiles, while higher-income households are defined as those in the fourth and fifth quintiles.

See the box entitled “Financial stability implications of higher than expected inflation”, Financial Stability Review, ECB, May 2022.

The countries with predominately variable-rate mortgage origination are Estonia, Cyprus, Latvia, Lithuania, Portugal and Finland. For countries like Ireland, Spain, Luxembourg and Slovenia, where mortgage lending has recently become predominately fixed rate, only their older mortgage stock would see short-term rate effects.

Liquid assets are defined as the stock of sight and savings deposits, bonds, equities and mutual funds.

Depending on the country, the survey data in the most recent HFCS vintage are from any time between 2016 and 2018.

The approach is similar to, but expands on, that of Ampudia, M., van Vlokhoven, H. and Żochowski, D., “Financial fragility of euro area households”, Journal of Financial Stability, Vol. 27, 2016, pp. 250-262.

To capture structural changes in the employment situation, a logistic regression model is used to predict household members’ likelihood of switching into employment and using the unemployment benefits they previously received as a guideline for their new income. To account for the structural increase in the share of newly originated fixed-rate mortgages in many countries, a correction factor is applied to households’ monthly interest payment burden. This is computed from the change in the share of variable-rate mortgages between the vintage date and the end of the first quarter of 2022 and the share of mortgages originated in the years between the vintage date and the end of the first quarter of 2022 in comparison with total household mortgages.

Income after taxes is computed using data from the OECD on average household tax rates per country-specific income quintile. For the sake of simplicity, it is assumed that non-household main residence mortgage interest payments are tax-deductible in all euro area countries.

When households become illiquid, there is no distinction between mortgage debt and consumer debt. It is reasonable to assume that households would prefer to default on consumer debt before jeopardising their mortgage if they hold both types of debt.

Since the analysis is focused on the short term, it does not consider non-liquid assets which illiquid or distressed households could liquidate to cover negative cash flows. Countries in which lower-income households have relatively high holdings of non-liquid assets, such as real estate, may ultimately face lower risks of loan defaults.

As of the second quarter of 2022, loans to households make up roughly 52% of total domestic bank lending in the euro area, followed by loans to non-financial corporations with a share of around 39%.

Data from the ECB. The remaining debt are loans for purposes other than housing or purchasing consumer goods.

While the country breakdown of mortgage debt shares is more informative with regard to the impact on systemic financial stability because of the overall size of mortgages on bank balance sheets, the consumer debt breakdown is useful for assessing the potential impact on individual institutions with a focus on consumer lending as households in distress may choose to default on such loans first.

In reality, it is by no means certain that all distressed or illiquid households will default on their entire debt. Factors such as impending employment changes, family wealth or prioritising debt service over other payments are not considered, which is why the bank impact estimates in this section should be seen as conservative upper bounds and represent a downside scenario. In addition, country-specific insolvency and government guarantee schemes for consumer and mortgage debt, which could have a mitigating impact on households in default or distress, have not been taken into account.

The assumption that households would default on their entire debt is highly conservative and represents a downside estimate in its own right. Also, in reality not all defaults would occur at once. The estimates in this analysis speak more to the magnitude of the defaults than to the timing of their occurrence.

Survey and household data are matched under the assumption that the distribution of households within and across income quintiles is the same for all exposures of a given bank, the counterparty being in the same country. Therefore, bank loans to households in a given country are split into income quintiles according to the share of total household loans located in that quintile, as specified by survey data. A similar approach is used to calculate the NPL ratios per quintile, where the share of defaulted or distressed loans to households within a quintile, as taken from survey data, is used to divide banks’ household NPLs in a given country into five income quintiles. The resulting quintile values for household loans and household NPLs are used to calculate quintile NPL ratios. It is assumed that the distribution of total household debt as shown in the HFCS is identical to household debt held by euro area banks, notwithstanding the fact that some households might be indebted to alternative lenders, not banks.

In Greece notably, consumer debt accounted for a third of household NPLs in the first quarter of 2022, although Greek banks hold almost four times more mortgage debt than consumer debt. This particularly high share of household NPLs is explained by the very high share – over 40% – of consumer debt owed by lower-income households without sufficient savings (Chart B.4, panel b). On the other hand, despite having an equally high share of consumer debt attributable to lower-income households, Dutch banks have virtually no NPLs on their books as, on average, lower-income households in the Netherlands have relatively higher disposable incomes and some liquid assets that they can use to cushion income shortfalls.

In Cyprus, notably, the preliminary data indicate a deleveraging of households and a shift in the debt distribution towards higher income quantiles in recent years. This structural change in the debt distribution, which will likely contain the estimated increase in NPL ratios, is not reflected in the current analysis results but is expected to be reflected in future vintages of HFCS data.

See the article entitled “Energy prices and private consumption: what are the channels?”, Economic Bulletin, Issue 3, ECB, 2022.

See the article entitled “Gauging the sensitivity of loan-service-to-income (LSTI) ratios to increases in interest rates”, Macroprudential Bulletin, Issue 19, ECB, 2022.