The impact of higher energy prices on services and goods consumption in the euro area

Published as part of the ECB Economic Bulletin, Issue 8/2022.

The recent increase in real consumer spending in the euro area masks heterogeneous developments in individual consumption components. Total private consumption in the euro area increased significantly in the second and third quarters of 2022, mainly supported by consumption of services, which rose sharply after subdued growth at the beginning of the year (Chart A).[1] By contrast, consumption of non-durable goods fell for the third quarter in a row. Moreover, consumption of durable goods continued its downward trend (which began in the last quarter of 2021) up until the second quarter of 2022, after which it began to improve in the third quarter. While the recovery in total private consumption reflected several factors, including the widespread loosening of pandemic-related restrictions and the gradual easing of supply bottlenecks, the strong rise in energy prices created significant headwinds to consumption growth through its effect on households’ purchasing power.[2] This box aims to quantify the impact of the recent increase in energy prices on real consumer spending in the euro area. It focuses on energy supply shocks that have become increasingly significant since mid-2021, particularly with the Russian invasion of Ukraine in early 2022.[3]

Chart A

Developments in real private consumption in the euro area

(Q4 2019 = 100)

Sources: Eurostat and ECB calculations.

Note: Non-durable goods include semi-durable goods.

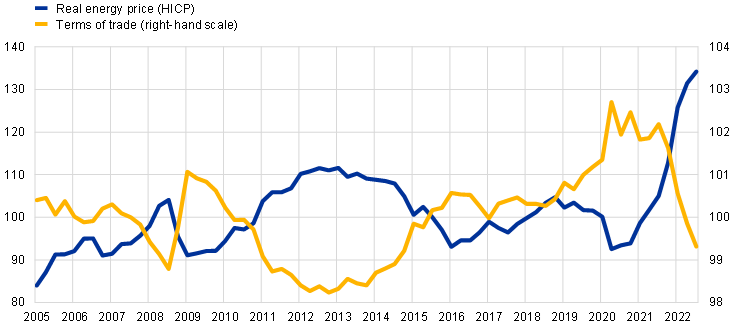

The recent sharp increase in energy prices has had a significant impact on households’ real disposable income. When assessing the impact of energy price changes on real private consumption, the ratio between the GDP deflator and the private consumption deflator (or between the income and the expenditure deflator) is a useful indicator. This measure of the terms of trade is well founded from a theoretical perspective and captures both direct channels (e.g. consumer prices) and indirect channels (e.g. wages) through which energy prices affect households’ purchasing power.[4] In the euro area, this indicator is negatively correlated with real energy prices and has been declining sharply since the end of 2021, weighing significantly on households’ real disposable income and affecting private consumption (Chart B).[5]

Chart B

Real energy prices and the terms of trade

(2015 = 100)

Sources: Eurostat, ECB and ECB calculations.

Notes: The “real energy price” indicates the ratio between the energy component of the HICP and the overall HICP index. The terms of trade are proxied by the ratio between the GDP deflator and the private consumption deflator.

A structural vector autoregression (SVAR) model can be used to derive the impact of energy supply shocks on consumer spending. The SVAR model includes the ratio between the GDP deflator and the private consumption deflator as an indicator of the terms of trade, the HICP, real GDP, the three-month EURIBOR and either total private consumption or consumption of durable goods, non-durable goods, or services. Sign restrictions on the impact responses of the model variables are used to identify structural economic drivers. In determining the energy supply shock, an unexpected deterioration in the supply of energy is modelled by assuming that an unexpected deterioration in the terms of trade (i.e. an increase in real energy prices) leads to an immediate positive impact on inflation and an immediate negative effect on real economic activity and consumer spending.[6]

Energy supply shocks have weighed considerably on real consumer spending in recent quarters, particularly on durable goods. Total private consumption was significantly affected by energy supply shocks in recent quarters (Chart C). However, the individual consumption components were affected to varying degrees. Energy supply shocks only had a negligible negative impact on services consumption, meaning that this component increased substantially following the reopening of the economy in spring 2022. However, these shocks had a clear, larger negative effect on the consumption of non-durable goods, and in particular durable goods, reflecting weaknesses observed in recent quarters. The relatively strong reaction of durable goods consumption in response to the increase in energy prices is likely due to the fact that households are able to use their existing stock of durable goods without an immediate impact on their welfare.[7] Moreover, given the heightened uncertainty due to the energy price fluctuations, households may have decided to postpone irreversible purchases of durable goods.[8]

Chart C

Impact of energy supply shocks on real consumer spending in the euro area

(percentage changes and percentage point contributions)

Sources: Eurostat and ECB calculations.

Notes: The results are based on four individual structural vector autoregression (SVAR) models identified with sign restrictions. Each model includes the ratio between the GDP deflator and the private consumption deflator as an indicator of the terms of trade, the HICP, real GDP, the three-month EURIBOR and either total private consumption or consumption of durable goods, non-durable goods, or services. The models are estimated using quarterly data (expressed as percentage changes against the previous quarter, except for the three-month EURIBOR). The sample covers the first quarter of 1999 to the fourth quarter of 2019 to prevent the extraordinary economic fluctuations during the COVID-19 pandemic from affecting the estimated model coefficients. Non-durable goods include semi-durable goods.

Increased energy prices will continue to weigh on real consumer spending over the next quarters. As energy prices and uncertainty have remained high, households’ real disposable income is likely to wane further at the turn of the year, with negative effects on consumer spending, and particularly on durable goods, notwithstanding the likely positive impact of a further easing of supply bottlenecks. Despite its relative resilience to energy price increases, services consumption is also likely to weaken as reopening effects gradually fade. Overall, this points to significantly weaker consumption dynamics in the near term, in line with the December 2022 Eurosystem staff macroeconomic projections for the euro area.

Real consumer spending and its components for the euro area are based on the aggregation of available data at the country level.

See, for example, the article entitled “Energy prices and private consumption: what are the channels?”, Economic Bulletin, Issue 3, ECB, 2022.

See the article entitled “Energy price developments in and out of the COVID-19 pandemic – from commodity prices to consumer prices”, Economic Bulletin, Issue 4, ECB, 2022.

For a detailed discussion, see the box entitled “Oil prices, the terms of trade and private consumption”, Economic Bulletin, Issue 6, ECB, 2018.

The terms of trade can also be affected by other factors (e.g. the nominal exchange rate, the prices of goods and services other than energy). Empirically, however, most of the variation in the euro area terms of trade is explained by energy prices. For a breakdown of the dynamics of household real disposable income into different sources of income and the terms of trade in periods when energy prices fluctuate sharply, see the article entitled “Energy prices and private consumption: what are the channels?”, Economic Bulletin, Issue 3, ECB, 2022.

The model also identifies an aggregate demand shock, an aggregate supply shock, a monetary policy shock and a residual shock to ensure that all other shocks in the model do not act like the energy price shock. The restrictions imposed are in line with the literature on identifying energy price shocks versus other structural shocks, see, for instance, Conti, A.M., Neri, S. and Nobili, A., “Low inflation and monetary policy in the euro area”, Working Paper Series, No 2005, ECB, 2017.

See Browning, M. and Crossley, T.F., “Shocks, stocks, and socks: smoothing consumption over a temporary income loss”, Journal of the European Economic Association, Vol. 7, No 6, 2009.

See Edelstein, P. and Kilian, L., “How sensitive are consumer expenditures to retail energy prices?”, Journal of Monetary Economics, Vol. 56, No 6, 2009, pp. 766-779. For an overview of the role played by durable goods as a cyclical driver of euro area consumption, see the article entitled “Consumption of durable goods in the euro area”, Economic Bulletin, Issue 5, ECB, 2020.