Assessing wage dynamics during the COVID-19 pandemic: can data on negotiated wages help?

Published as part of the ECB Economic Bulletin, Issue 8/2020.

The confluence of the economic consequences of and policy responses to the coronavirus (COVID-19) pandemic poses challenges for interpreting labour market developments – including wage developments. For instance, the substantial changes observed in recent quarters in hours worked per person employed, together with the widespread application of short-time work schemes and issues related to their statistical recording, complicate the interpretation of wage indicators such as “compensation per hour” or “compensation per employee”.[1] The ECB indicator of negotiated wage rates captures the outcome of collective bargaining processes and is not directly affected by these special factors.[2] It also tends to be published around one month earlier than wage indicators based on quarterly national accounts. It should be noted, however, that the pandemic may also have had an impact on the indicator properties of negotiated wages, as it has led to fewer wage agreements being concluded than under normal circumstances. This box considers what role the indicator of negotiated wage rates can play in assessing and forecasting wage developments at the current juncture.

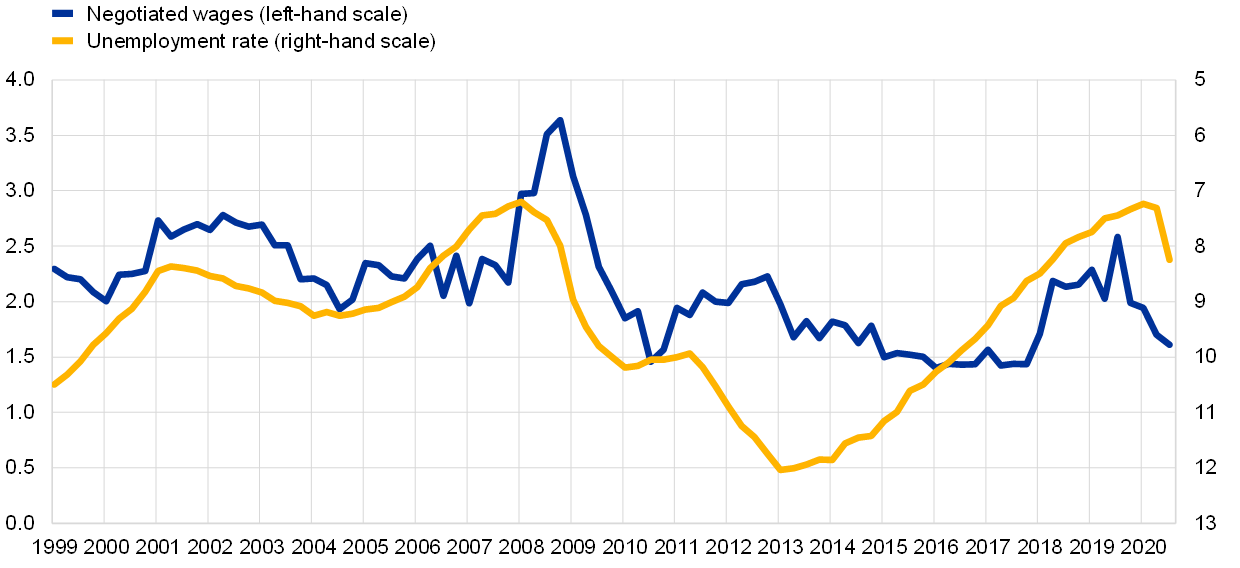

While the data on negotiated wages are available on a more timely basis, negotiated wage growth tends to only react with some lag to changes in labour market conditions. It usually takes time for changes in unemployment reflecting tightness in the labour market to be reflected in wage negotiations. The indicator of negotiated wage rates therefore tends to respond to cyclical labour market developments with a time lag of several quarters (see Chart A). This is a result of bargaining processes in large euro area countries (which mostly take place at the sectoral level), with a variety of start dates and durations, that often set wages for periods longer than one year. In line with this institutional feature, recent developments in negotiated wage growth do not point to the pandemic-related labour market upheavals having had a major impact as yet. While year-on-year growth decreased to 1.9%, 1.7% and 1.6% in the first, second and third quarters of 2020 respectively, this in part reflects base effects – meaning that, for example, the low reading in the third quarter of 2020 is in part related to the upward impact in the third quarter of 2019 associated with special payments in Germany at that time.[3]

Chart A

Developments in negotiated wage growth and the unemployment rate

(left-hand scale: annual percentage changes; right-hand scale: percentages)

Sources: Eurostat and ECB calculations.

Notes: The latest observation is for the third quarter of 2020. The right-hand scale is inverted.

Wage agreements concluded before the outbreak of the pandemic still play a dominant role in the latest developments in the indicator of negotiated wage rates. Quarter-on-quarter changes in the indicator show that negotiated wage dynamics in 2020 have so far been very much in line with the profile observed on average since 1999 (see Chart B). Changes to negotiated wages tend to occur mainly in the first quarter of each year. This holds true both for average changes in the indicator of negotiated wage rates and for average absolute changes. The fact that average absolute changes in the indicator of negotiated wages, which reflect the average absolute amount of increases as well as decreases, are also concentrated in the first quarter shows that changes to negotiated wages do indeed occur mainly at the beginning of each year. More granular information suggests that nearly all of the increase in negotiated wages in the first quarter of 2020 was attributable to wage increases in January, i.e. before the pandemic hit. The dominant role of wage agreements at the start of each year implies that the main effects of the pandemic on negotiated wages might only start to become visible in early 2021, when a large share of wage contracts is due for renegotiation in several euro area countries.

Chart B

Seasonal pattern of changes in negotiated wages

(quarter-on-quarter percentage changes; period analysed: 1999-2020 unless otherwise indicated)

Sources: ECB internal estimates and ECB calculations.

Notes: The latest observation is for the third quarter 2020. Absolute changes are derived by adding up the absolute amounts of increases and decreases.

At this juncture, some forward-looking information may be embedded in the wage drift. The wage drift can be derived as the difference between growth rates of actual pay, as measured by gross wages and salaries per employee, and growth rates of negotiated wages.[4] Based on this approach, the negative wage drift in the first three quarters of 2020 (see Chart C) captures the fact that firms’ actual wage bill was generally lower owing to the government support measures and also fewer bonuses and promotions, among other factors. However, this calculation of the wage drift is inevitably affected by shifts in the composition of employment and in the average hours worked per person employed – and these shifts are very substantial at the current juncture. The composition of employment is likely to have changed, as the pandemic has caused job losses in the service sector in particular, which has relatively more lower-paying jobs, thereby mechanically increasing the average pay and partly offsetting the otherwise negative impacts on the aggregate wage drift.[5] The wage drift signals the downward pressure that may emerge for negotiated wages should the situation in the labour market deteriorate, with workers who are currently on reduced hours instead becoming unemployed.

Chart C

Wage drift and the contribution of hours worked to growth in compensation per employee

(percentage point contributions)

Sources: Eurostat, ECB and ECB calculations.

Notes: The latest observation is for the third quarter of 2020. “Others” refers to all other sectors. The columns represent the contributions of services, manufacturing and other sectors to the overall contribution of hours worked to growth in compensation per employee.

Current growth in negotiated wages continues to be driven by pre-pandemic wage agreements, limiting its informational value for predicting future actual wage growth. The main effects of the pandemic on negotiated wage growth are likely to become visible only from 2021, when a substantial share of wage contracts in euro area countries is due to be renegotiated. Wage drift developments, in conjunction with information on hours worked and unemployment, can provide some indications regarding the environment in which these negotiations take place. The availability of more granular data, for example on negotiated wage growth in different sectors, would be very helpful in analysing euro area wage developments in more detail.

- These issues have been discussed in past issues of the ECB’s Economic Bulletin. See the box entitled “Short-time work schemes and their effects on wages and disposable income”, Economic Bulletin, Issue 4, ECB, 2020 and the box entitled “Developments in compensation per hour and per employee since the start of the COVID-19 pandemic” in the article entitled “The impact of the COVID-19 pandemic on the euro area labour market” in this issue of the Economic Bulletin.

- The indicator of negotiated wage rates has been compiled by the ECB since 2001 based on non-harmonised country data as an indicator of possible wage pressures. For details, see the box entitled “Monitoring wage developments: an indicator of negotiated wages”, Monthly Bulletin, ECB, September 2002.

- For more details, see Monthly Report, Vol. 71, No 11, Deutsche Bundesbank, November 2019, p. 8.

- This implies that headline wage growth as measured by compensation per employee can be broken down into negotiated wage growth, the wage drift and the impact of changes in social security contributions, where the latter is defined as the difference between the annual rate of growth in compensation per employee and the annual rate of growth in gross wages and salaries per employee.

- For details of such compositional effects, see, for example, Crust, E.E., Daly, M.C. and Hobjin, B., The Illusion of Wage Growth, FRBSF Economic Letter, Federal Reserve Bank of San Francisco, August 2020, and the article entitled “The effects of changes in the composition of employment on euro area wage growth”, Economic Bulletin, Issue 8, ECB, 2019.