- PRESS RELEASE

Euro money market statistics: Sixth maintenance period 2022

22 November 2022

This will be the last press release for euro money market statistics. The underlying Money Market Statistical Reporting (MMSR) dataset will continue to be updated in accordance with the ECB statistical calendar and is available in the ECB’s Statistical Data Warehouse (SDW) as before.

- 113 new data series covering the spot and forward OIS markets available as of today in the Statistical Data Warehouse (SDW)

- Daily average borrowing turnover in the unsecured segment increased from €131 billion in the fifth maintenance period of 2022 to €177 billion in the sixth maintenance period of 2022

- Weighted average overnight rate on borrowing transactions in the unsecured segment increased from -0.06% to 0.65% for the wholesale sector and increased from -0.03% to 0.68% for the interbank sector

- Daily average borrowing turnover in the secured segment decreased from €421 billion to €410 billion, with a weighted average overnight rate of 0.23%

New data on the OIS market

The European Central Bank (ECB) has today published, for the first time, statistics on the overnight index swap (OIS) segment of the euro money market. The new statistics complement data on the unsecured and secured money market segments, which have been published regularly since November 2017 and January 2019 respectively. By publishing these figures, the ECB aims to further enhance market transparency and therefore improve money market functioning. The data series include information on the OIS spot and forward markets about the total and daily average nominal amount and the weighted average rate. For spot transactions, the series are broken down by maturity bucket (i.e. by groups of transactions with the same or a very similar maturity) and aggregated by maintenance period. For forward-traded transactions, four different quarterly series are published: (1) transactions related to the ECB maintenance period calendar aggregated by future maintenance period, (2) transactions associated with two subsequent International Monetary Market dates aggregated in terms of quarters for transactions with a three-month maturity, (3) transactions classified in the 12-month to 24-month maturity bucket (also known as 1-year-1-year forwards), and (4) the total notional amount of all forward-dated OIS transactions. These data are collected from 47 Euro Area banks under the Money Market Statistical Reporting Regulation. Please see below for a detailed overview on the new series.

Main developments

Chart 1

Daily average nominal borrowing and lending turnover in the secured and unsecured wholesale markets by maintenance period (MP)

(EUR billions)

Unsecured market

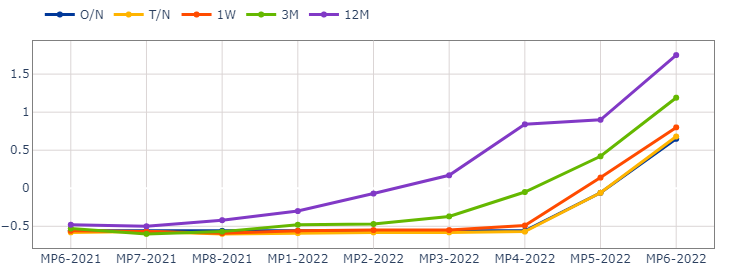

Chart 2

Weighted average rate for wholesale sector borrowing in the unsecured segment by tenor and maintenance period

(percentages)

In the sixth maintenance period of 2022, which started on 14 September 2022 and ended on 1 November 2022, the borrowing turnover in the unsecured segment averaged €177 billion per day. The total borrowing turnover for the period as a whole was €6,179 billion. Borrowing from credit institutions, i.e. on the interbank market, represented a turnover of €842 billion, i.e. 14% of the total borrowing turnover. Lending to credit institutions amounted to €193 billion. Overnight borrowing transactions represented 74% of the total borrowing nominal amount. The weighted average overnight rate for borrowing transactions over the last maintenance period was 0.68% for the interbank sector and 0.65% for the wholesale sector, compared with -0.03% and -0.06% respectively in the previous maintenance period.

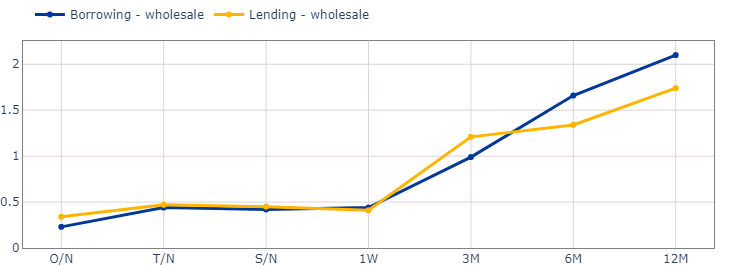

Secured market

Chart 3

Weighted average rate for wholesale sector borrowing and lending in the secured segment by tenor

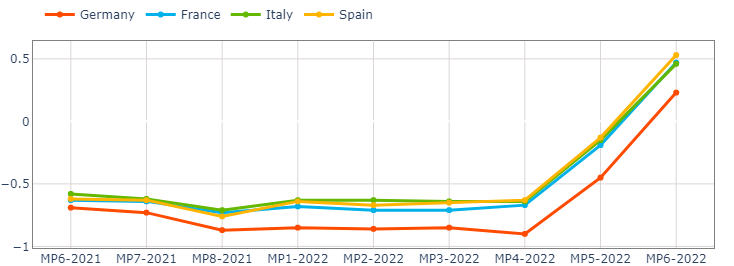

In the sixth maintenance period of 2022, the borrowing turnover in the secured segment averaged €410 billion per day, while the total borrowing turnover for the period as a whole was €14,362 billion. Cash lending represented a turnover of €11,825 billion and the daily average amounted to €338 billion. Most of the turnover was concentrated in tenors ranging from overnight to up to one week, with overnight transactions representing around 26% and 22% of the total nominal amount on borrowing and lending side respectively. The weighted average overnight rate for borrowing and lending transactions was, respectively, 0.23% and 0.34% for the wholesale sector, compared with -0.44% and -0.46% in the previous maintenance period. In the sixth maintenance period of 2022, the weighted average rate for spot/next borrowing transactions ranged from 0.53% for operations based on collateral issued in Spain to 0.23% for operations based on collateral issued in Germany.

Chart 4

Weighted average rate for spot/next borrowing in the secured segment for collateral issued by maintenance period (MP)

(percentages)

OIS market

Two large groups of transactions can be distinguished in the OIS market: spot transactions and forward transactions. In the sixth maintenance period of 2022, the total turnover in the OIS segment including novations was €4,288 billion, of which 48% corresponded to the spot market and 42% to the forward market. The remaining activity (10%) corresponded to novations, which usually occur when a transaction is cleared with a central counterparty between the two original transactors.

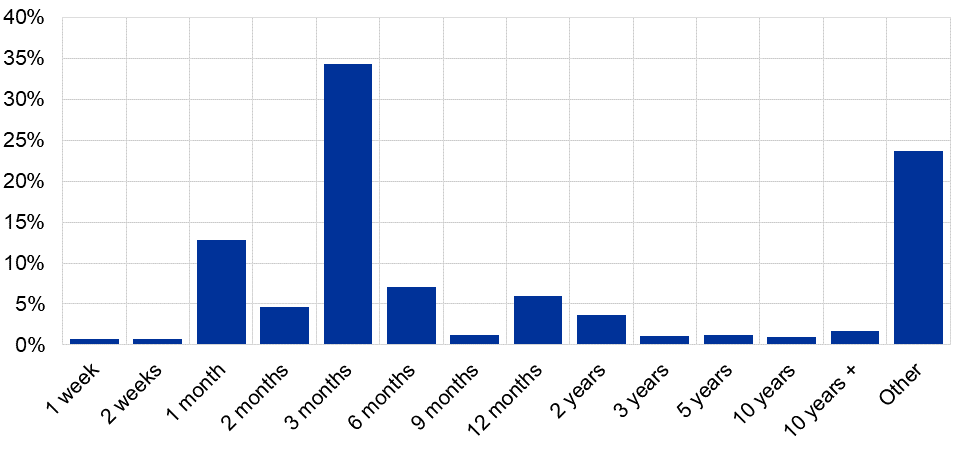

Most of the total turnover of €2,039 billion in spot trading (66%) was concentrated in the intermediate maturities (i.e. ranging from the one-month bucket up to and including the 12-month bucket); 9% of the turnover was spread over longer maturities (i.e. two years and above). Maturities of under one month were traded much less (close to 1%). The remaining 24% of activity corresponded to transactions with tailored maturities that cannot be classified in any standard maturity bucket and are therefore labelled “Other”.

Most of the total turnover of €1,818 billion in forward transactions (58%) was concentrated in transactions that have both their start and end dates tied to the Eurosystem’s reserve maintenance periods (MP-dated trades), while forward transactions that have start and end dates matching International Monetary Market futures dates (IMM-dated trades) made up 17% of the market. Around 1% of forward market activity corresponded to transactions that start 12 months after the trade date and mature 12 months thereafter (FD 12M24M, or 1y-1y) and the remaining 25% corresponded to swaps that do not fall into any of the aforesaid categories.

Chart 5

Total spot notional amounts broken down by maturity bucket in the sixth maintenance period of 2022

(percentages)

In the sixth maintenance period of 2022, the weighted average rate for spot OIS transactions in the three-month maturity bucket was 1.33% for the wholesale sector, compared with 0.46% in the previous maintenance period. The weighted average rate for spot transactions ranged from 0.98% for the one-month maturity bucket to 2.63% for the five-year maturity bucket.

Chart 6

Weighted average rate for wholesale sector spot transactions in the OIS segment by maturity bucket and maintenance period

(percentages)

Table 1

Euro money market statistics

|

| Turnover (EUR billions) | Average rate O/N (percentages) | |||||

|

| Daily average | Total |

|

| |||

|

| MP 5 2022 | MP 6 2022 | MP 5 2022 | MP 6 2022 | MP 5 2022 | MP 6 2022 | |

Unsecured | Borrowing, wholesale | 131 | 177 | 4,600 | 6,179 | -0.06 | 0.65 | |

Of which, interbank | 18 | 24 | 642 | 842 | -0.03 | 0.68 | ||

Lending, interbank | 4 | 6 | 141 | 193 | -0.02 | 0.59 | ||

Secured | Borrowing, wholesale | 421 | 410 | 14,732 | 14,362 | -0.44 | 0.23 | |

Lending, wholesale | 348 | 338 | 12,194 | 11,825 | -0.46 | 0.34 | ||

OIS spot market | Paid and received | 48 | 58 | 1,676 | 2,039 | - | - | |

For media queries, please contact Philippe Rispal, tel.: +49 69 1344 5482.

Notes

- The money market statistics are available in the ECB’s Statistical Data Warehouse.

- The Eurosystem collects transaction-by-transaction information from the 47 largest euro area banks in terms of banks’ total main balance sheet assets, broken down by their borrowing from and lending to other counterparties. Unsecured transactions include all trades concluded via deposits, call accounts or short-term securities with financial corporations (except central banks where the transaction is not for investment purposes), and -general government, as well as with non-financial corporations classified as “wholesale” under the Basel III liquidity coverage ratio framework. Secured transactions cover all fixed-term and open-basis repurchase agreements and transactions entered into under those agreements, including tri-party repo transactions, denominated in euro with a maturity of up to one year, between the reporting agent and financial corporations (except central banks where the transaction is not for investment purposes), and general government as well as non-financial corporations classified as wholesale under the Basel III liquidity coverage ratio framework. OIS transactions include all interest rate swaps denominated in euro where a fixed rate is exchanged for the euro short-term rate (€STR) conducted with financial corporations (except central banks where the transaction is not for investment purposes), general government, or non-financial corporations classified as wholesale under the Basel III liquidity coverage ratio framework. As of the first maintenance period of 2019, the wholesale sector covers all counterparties in the sectors listed above. More information on the methodology applied, including the list of reporting agents, is available in the statistics section of the ECB’s website.

- The weighted average rate is calculated as the arithmetic mean of the rates weighted by the respective nominal amount over the maintenance period on all days on which TARGET2, the Trans-European Automated Real-time Gross settlement Express Transfer system, is open.

- Borrowing refers to transactions in which the reporting bank receives euro-denominated funds, irrespective of whether the transaction was initiated by the reporting bank or its counterpart.

- Lending refers to transactions in which the reporting bank provides euro-denominated funds, irrespective of whether the transaction was initiated by the reporting bank or its counterpart.

- The tenors O/N, T/N, S/N, 1W, 3M, 6M and 12M refer to, respectively, overnight, tomorrow/next, spot/next, one week, three months, six months and twelve months.

- The maturity buckets 1M, 3M, 6M, 12M, 2Y and 5Y refer to, respectively, one month, three months, six months, twelve months, two years and five years.

- Trades with a start date within three business days of the trade date are classified as spot transactions, and those with a later start date are classified as forward transactions.

- The collateral issuer country refers to the jurisdiction that issues the collateral used for transactions secured by single collateral identified by an International Securities Identification Number.

- The missing values for tenors in some of the reserve maintenance periods may be due to confidentiality requirements.

- In addition to the developments in the latest maintenance period, this press release incorporates minor revisions to the data for previous periods.

- Data are published 15 working days after the end of each maintenance period. The release calendar and the indicative calendars for the Eurosystem’s reserve maintenance periods are available on the ECB’s website.

European Central Bank

Directorate General Communications

- Sonnemannstrasse 20

- 60314 Frankfurt am Main, Germany

- +49 69 1344 7455

- media@ecb.europa.eu

Reproduction is permitted provided that the source is acknowledged.

Media contacts