Published as part of the ECB Economic Bulletin, Issue 7/2024.

This box summarises the findings of recent contacts between ECB staff and representatives of 95 leading non-financial companies operating in the euro area. The exchanges took place between 16 and 26 September 2024.[1]

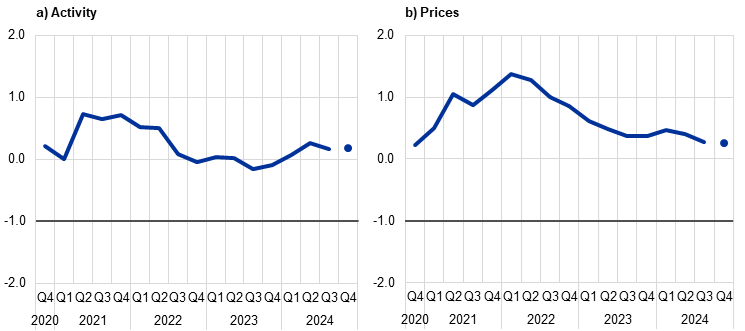

Contacts pointed to a slowdown in business momentum over the summer months, largely observed in the industrial sector (Chart A and Chart B, panel a). This reflected, in particular, growing concerns about competitiveness and mounting uncertainty surrounding the green transition as well as both European and global political developments. This was causing businesses to scale back investment and focus on cost cutting, which also weighed on consumer confidence. The overall picture was nonetheless still consistent with modest growth in overall activity, as continued growth in services offset contracting manufacturing output. Overall activity tended to be below prior expectations, mainly in Germany and France, but was generally more resilient elsewhere.

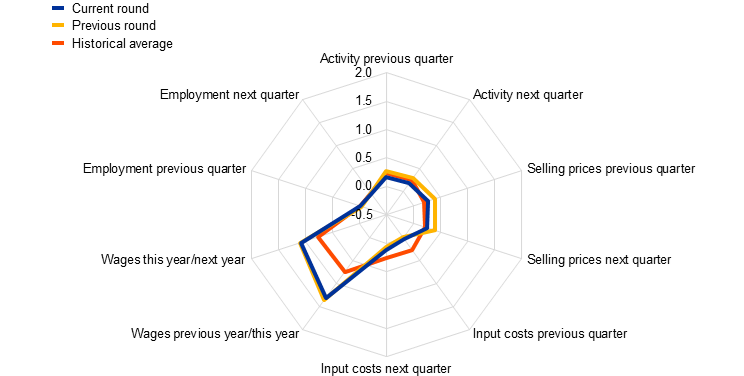

Chart A

Summary of views on activity, employment, prices and costs

(averages of ECB staff scores)

Source: ECB.

Notes: The scores reflect the average of scores given by ECB staff in their assessment of what contacts said about quarter-on-quarter developments in activity (sales, production and orders), input costs (material, energy, transport, etc.) and selling prices, and about year-on-year wage developments. Scores range from -2 (significant decrease) to +2 (significant increase). A score of 0 would mean no change. For the current round, previous quarter and next quarter refer to the third and fourth quarters of 2024 respectively, while for the previous round these refer to the second and third quarters of 2024. Discussions with contacts in January and in March/April regarding wage developments normally focus on the outlook for the current year compared with the previous year, while discussions in June/July and September/October focus on the outlook for the next year compared with the current year. The historical average is an average of scores compiled using summaries of past contacts extending back to 2008.

Chart B

Evolution of views on developments in and the outlook for activity and prices

(averages of ECB staff scores)

Source: ECB.

Notes: The scores reflect the average of scores given by ECB staff in their assessment of what contacts said about quarter-on-quarter developments in activity (sales, production and orders) and selling prices. Scores range from -2 (significant decrease) to +2 (significant increase). A score of 0 would mean no change. The dot refers to expectations for the next quarter.

Contacts gave somewhat mixed views of developments in consumer spending, suggesting a still rather muted recovery thus far. Most contacts in the consumer goods and retail sectors continued to describe a somewhat polarised market in which demand from wealthy customers for the most expensive products continued to grow healthily, while other consumers were still “trading down” and seeking to save money. In the food retail sector, this continued to benefit discounters over regular stores and own brands over traditional labels. Younger consumers’ appetite for online deals was increasingly being met by non-EU online retail platforms offering products at rock-bottom prices. Other signs of consumers still adjusting their budgets included lower volume purchases and the strength of sales in the “circular economy”. This type of reusage not only extended the lifetime of products and reduced waste but was also more affordable. Several contacts did, by contrast, point to a pick-up in consumer goods spending, which they attributed to moderating inflation and recovering real incomes. While this pick-up mostly related to purchases of non-durable consumer goods, there were also reports of retail spending on large kitchen appliances starting to recover from its post-pandemic low, even if overall demand for such appliances remained feeble due to the continued weakness in residential construction. Growth in consumer spending on services continued to outpace that of spending on goods. This was reflected by strong tourism-related activity over the summer months and even healthier trends in hotel bookings thus far for the autumn and winter seasons. That said, there were also increasing signs of consumer demand for tourism services becoming more sensitive to high prices, as reflected, for example, in the sturdier growth in demand for low season hotel bookings as compared with those for the high season.

Demand in the automotive sector had weakened in recent months, with knock-on effects elsewhere in the manufacturing industry. This reflected both a general lack of consumer and corporate demand as well as still fragile or waning demand for battery electric vehicles (BEVs). The renewed weakness in the automotive sector was the most widely cited cause of reportedly declining activity across many parts of the capital and intermediate goods sectors. Moreover, faltering BEV demand was seen as raising questions about the transition of this important sector in the wider context of meeting climate targets, contributing to – and symptomatic of – such broader uncertainty in the manufacturing industry.

There was increasing apprehension across the industrial sector, as it struggled with high costs and political uncertainty, causing firms to scale back investment and focus on cost cutting. Contacts cited high and volatile energy prices, rising regulatory costs and strong wage growth, which were eroding many European firms’ competitiveness in global markets. Many raised growing concerns about an approach to reducing carbon emissions based on complex regulations and reporting requirements, ultimately pushing up the costs to firms. This was coupled with the uncertainty caused by a lack of stability in political decision-making surrounding the relevant regulations and subsidies. Furthermore, contacts pointed to a deteriorating global economic and political environment, including, most notably, the slowing and increasingly self-sufficient Chinese economy, which was dampening export demand and intensifying import competition. These factors combined were increasingly causing both capacity and climate-related investments to be put on hold. This was reflected in a lower intake of orders across much of the capital goods sector, as well as continued low, if not still declining, demand for intermediate goods, such as steel and chemicals which were also facing overcapacity and continued falling demand from a contracting construction sector. Frozen investment plans and a focus on cost cutting were observed to some extent in a reduced demand for consultancy services, while however boosting the demand for certain intangible assets such as efficiency-enhancing software. Contacts operating in civil engineering or manufacturing equipment for the aerospace and rail industries reported growing levels of production. However, these levels reflected past orders with delivery times spanning several years; and the same contacts also pointed to relatively low levels of new orders, in part due to political paralysis and fiscal policy constraints.

Contacts did not anticipate much change to the overall subdued growth dynamic in the short term. This contrasted somewhat with the mood from previous survey rounds this year which had been one of gradually growing optimism. Many still thought that lower inflation, falling interest rates and rising incomes would eventually provide a greater boost to consumer spending. Contacts tended, however, to push back their expectations for such a recovery into 2025. Many contacts also emphasised significant structural downside risks to the industrial sector in the absence of a more stable and less onerous regulatory environment.

The employment outlook was subdued, reflecting the focus of many firms on raising efficiency and productivity. In some parts of the manufacturing sector (automotive, chemicals, steel), this meant not only taking a cautious approach towards recruitment but also restructuring in response to weak demand and/or rising wage costs. The effect of this on aggregate employment was, however, expected to be muted, as employment was still growing in much of the services sector, and because, even in the manufacturing sector, many firms still faced labour shortages and had positions to fill. The cost-cutting measures being undertaken by some firms therefore provided recruitment opportunities for other firms in labour markets that were still structurally tight.

Contacts reported a further moderation in price growth overall (Chart A and Chart B, panel b). Retailers continued to report a competitive environment in which customers remained price-sensitive and this was reflected in rather stable prices. While contacts in the food retail sector still saw prices rising slightly, on average, in the third and fourth quarters, non-food retailers mostly reported stable or declining prices. Prices in the manufacturing sector were reportedly fairly stable overall. While, on average, prices were said to be increasing in the capital and consumer goods sectors, this was offset by decreasing prices in parts of the intermediate goods sector, mostly notably for steel. The overall stable price environment in the industrial sector was a result of the challenging economic situation, strong competition and largely unchanged prices of energy and raw materials, reflecting overall demand and supply conditions across global markets. Several contacts still alluded to higher shipping costs given the substantial increases in costs seen earlier in the year as a result of the rerouting of cargo ships between Asia and Europe around the southern tip of Africa. However, shipping freight rates were now falling once again as strong growth in shipping capacity currently outpaced demand, which had been somewhat frontloaded this year given the aforementioned Red Sea crisis. Most contacts in the business and consumer services sectors continued to report climbing prices. This reflected the need to pass on rising labour costs and continued growing demand. However, the overall momentum seemed to have eased in recent months. Besides wages, the mostly widely cited driver of cost growth was regulation.

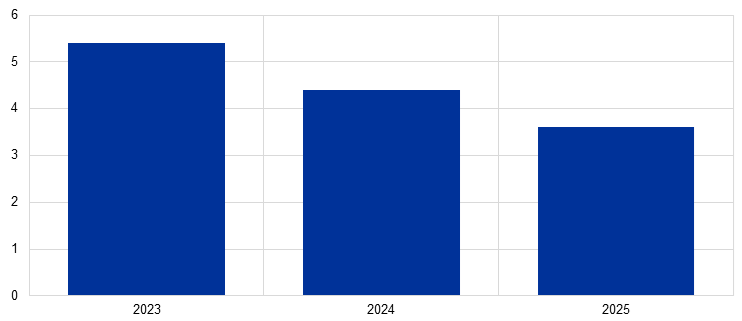

Contacts continued to expect a gradual moderation of wage growth next year (Chart C). On the basis of a simple average of the quantitative indications provided, contacts assessed wage growth as slowing, from 5.4% in 2023 to 4.4% in 2024, expecting a further decline to 3.6% in 2025. Despite the rotating nature of the panel of contacts, these expectations were basically unchanged from the previous survey round. Several contacts nonetheless pointed to very high wage demands made by the unions recently. In their view, these demands did not reflect the currently challenging economic environment and they increased uncertainty regarding both the wage and employment outlook.

Chart C

Quantitative assessment of wage growth

(percentages)

Source: ECB.

Notes: Averages of contacts’ perceptions of wage growth in their sector in 2023 and 2024 and of their expectations for 2025. The averages for 2023, 2024 and 2025 are based on indications provided by 75, 81, and 73 respondents respectively.

For further information on the nature and purpose of these contacts, see the article entitled “The ECB’s dialogue with non-financial companies”, Economic Bulletin, Issue 1, ECB, 2021.