Published as part of the ECB Economic Bulletin, Issue 2/2023.

This box describes liquidity conditions and the ECB’s monetary policy operations during the seventh and eighth reserve maintenance periods of 2022. Together, these two maintenance periods ran from 2 November 2022 to 7 February 2023 (the “review period”).

Policy tightening continued during the review period. The ECB’s Governing Council raised its key policy rates by 75 basis points at the Governing Council meeting at the end of October 2022 and raised them by a further 50 basis points at its mid-December 2022 meeting. These increases took effect in the seventh and eighth maintenance periods respectively.

Average excess liquidity in the euro area banking system declined by €245.8 billion during the review period, but remained very ample at levels above €4 trillion. The decrease was mainly driven by the early repayments in November and December of funds provided under operations 3 to 10 of the third series of targeted longer-term refinancing operations (TLTRO III). However, the decline was partially offset by the reduction in net autonomous factors, which added liquidity to the system. This decline in net autonomous factors continued the trend observed since the end of the negative interest rate environment in July 2022. During the eighth maintenance period a decline in government deposits was the primary driver of the reduction in net autonomous factors.

Hrvatska narodna banka joined the Eurosystem on 1 January 2023 when Croatia adopted the euro. Hrvatska narodna banka has therefore become the 20th Eurosystem member. As of 1 January 2023, the balance sheet figures of Hrvatska narodna banka began to be included in the financial statements of the Eurosystem.

Liquidity needs

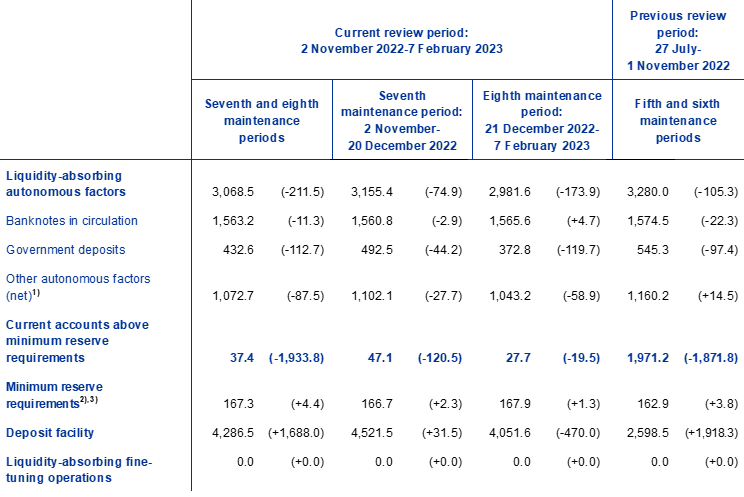

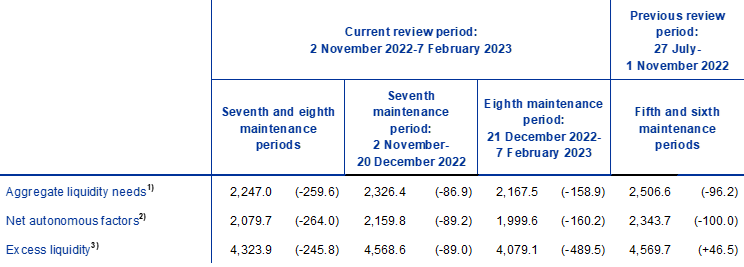

The average daily liquidity needs of the banking system, defined as the sum of net autonomous factors and reserve requirements, decreased by €259.6 billion in the review period, to €2,247 billion. The decrease was almost entirely due to a fall of €264 billion in net autonomous factors, to €2,079.7 billion, which, in turn, was mainly driven by a decline in liquidity-absorbing autonomous factors (see the section of Table A entitled “Other liquidity-based information”). The minimum reserve requirements marginally increased by €4.4 billion to stand at €167.3 billion.

Liquidity-absorbing autonomous factors decreased by €211.5 billion in the review period, to €3,068.5 billion, mainly owing to a declining trend in government deposits and other autonomous factors. Government deposits fell by €112.7 billion on average over the review period, to €432.6 billion, with most of the decline taking place in the eighth maintenance period (see the section of Table A entitled “Liabilities”). With the removal of the 0% interest rate ceiling on government deposits, as decided by the Governing Council in September 2022, the decline not only reflects seasonal effects, whereby lower balances are normally held at the end of the year, but it also reflects a more structural post-pandemic decline in the buffers held by national treasuries and an increase in the investment of such buffers in market instruments. The average value of banknotes in circulation decreased by €11.3 billion over the review period, to €1,563.2 billion. The reduction in banknote holdings and the amount of vault cash observed since the end of the negative policy rate environment continued, but at a slower pace. This trend was partially offset by the usual seasonal increase observed at the end of the year.

Liquidity-providing autonomous factors increased by €52.6 billion to stand at €989.2 billion. While net foreign assets decreased marginally, declining by €2.5 billion, net assets denominated in euro increased by €55.1 billion in the review period.

Table A provides an overview of the autonomous factors[1] discussed above and their changes.

Table A

Eurosystem liquidity conditions

Liabilities

(averages; EUR billions)

Source: ECB.

Notes: All figures in the table are rounded to the nearest €0.1 billion. Figures in brackets denote the change from the previous review or maintenance period.

1) Computed as the sum of the revaluation accounts, other claims and liabilities of euro area residents, capital and reserves.

2) Memo item that does not appear on the Eurosystem balance sheet and should therefore not be included in the calculation of total liabilities.

3) With the suspension of the two-tier system, information on the exemption allowance has been removed from the table.

Assets

(averages; EUR billions)

Source: ECB.

Notes: All figures in the table are rounded to the nearest €0.1 billion. Figures in brackets denote the change from the previous review or maintenance period. “MROs” denotes main refinancing operations, “LTROs” denotes longer-term refinancing operations, and “PELTROs” denotes pandemic emergency longer-term refinancing operations.

1) With the discontinuation of net asset purchases, the individual breakdown of outright portfolios is no longer shown.

Other liquidity-based information

(averages; EUR billions)

Source: ECB.

Notes: All figures in the table are rounded to the nearest €0.1 billion. Figures in brackets denote the change from the previous review or maintenance period.

1) Computed as the sum of net autonomous factors and minimum reserve requirements.

2) Computed as the difference between autonomous liquidity factors on the liabilities side and autonomous liquidity factors on the assets side. For the purposes of this table, items in the course of settlement are also added to net autonomous factors.

3) Computed as the sum of current accounts above minimum reserve requirements and the recourse to the deposit facility minus the recourse to the marginal lending facility.

Interest rate developments

(averages; percentages and percentage points)

Source: ECB.

Notes: Figures in brackets denote the change in percentage points from the previous review or maintenance period. The €STR is the euro short-term rate.

Liquidity provided through monetary policy instruments

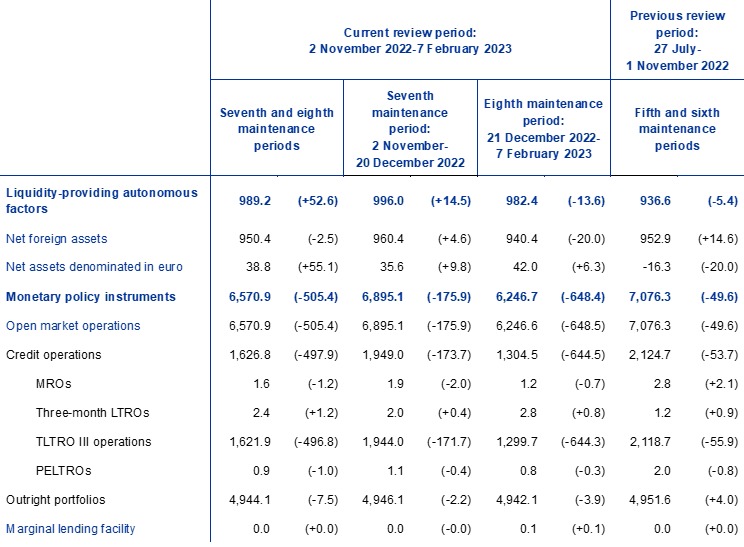

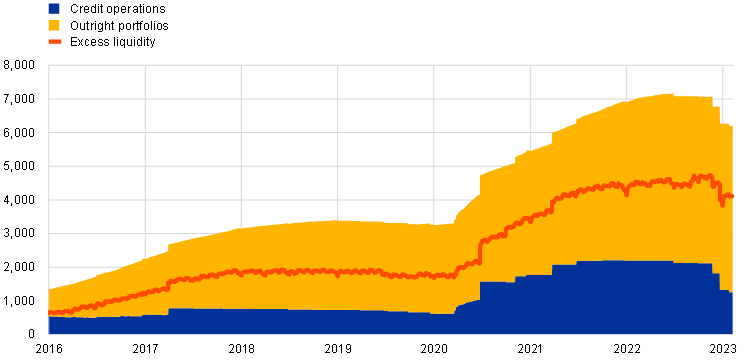

The average amount of liquidity provided through monetary policy instruments decreased by €505.4 billion during the review period, to €6,570.9 billion (Chart A). The reduction in liquidity was primarily driven by the decline in credit operations as a result of voluntary repayments by banks of TLTRO III funds. Net asset purchases under the ECB’s pandemic emergency purchase programme (PEPP) were discontinued at the end of March 2022 and purchases under its asset purchase programme (APP) were discontinued on 1 July 2022, meaning that outright portfolios no longer provide any additional liquidity.[2] As communicated in December, the APP portfolio will decline at a measured and predictable pace from the beginning of March 2023, as the Eurosystem will no longer reinvest all of the principal payments from maturing securities. The decline will amount to €15 billion per month on average until the end of June 2023 and its subsequent pace will be determined over time.

Chart A

Changes in liquidity provided through open market operations and excess liquidity

(EUR billions)

Source: ECB.

Note: The latest observations are for 7 February 2023.

The average amount of liquidity provided through credit operations decreased by €497.9 billion during the review period. This decrease mainly reflects the voluntary TLTRO III repayments, which amounted to €496.8 billion during the review period. The voluntary early repayment operations in November, December and January amounted to €296.3 billion, €447.5 billion and €62.7 billion respectively. These large repayments followed the decision of the ECB’s Governing Council to recalibrate the terms of the operations at the end of October in order to ensure consistency with the broader monetary policy normalisation process. Changes in other credit operations (pandemic emergency longer-term refinancing operations, main refinancing operations and three-month longer-term refinancing operations) were minor, amounting to a net decline in liquidity provided of just €1 billion.

Excess liquidity

Average excess liquidity decreased by €245.8 billion to reach €4,323.9 billion (Chart A). Excess liquidity is the sum of banks’ reserves above the reserve requirements and the recourse to the deposit facility net of the recourse to the marginal lending facility. It reflects the difference between the total liquidity provided to the banking system and banks’ liquidity needs. After peaking at €4,748 billion in November 2022, excess liquidity has progressively decreased following the aforementioned TLTRO III early repayments, net of the effects of autonomous factors.

Interest rate developments

The average euro short-term rate (€STR) increased by 136.6 basis points over the review period, to 1.65% per annum. The pass-through of the ECB policy rate hikes that became applicable in November and December to unsecured money market rates was complete and immediate. On average, the €STR traded at 9.8 and 10 basis points below the deposit facility rate during the seventh and eighth maintenance periods respectively, compared with 8.5 and 9.3 basis points during the fifth and sixth maintenance periods respectively.

The average euro area repo rate, as measured by the RepoFunds Rate Euro Index, increased by almost 133.7 basis points during the review period, to 1.485%. The pass-through to secured money market rates was not as smooth as for the unsecured money market, particularly in the case of the initial policy rate hikes in July and September 2022. However, transmission subsequently improved, with the policy rate hikes in November and December being almost fully passed through. This smoother transmission was likely related to an easing of concerns about collateral scarcity. Collateral availability improved through several channels. At its September meeting, the ECB’s Governing Council decided to change the remuneration of certain non-monetary policy deposits by temporarily removing the 0% interest rate ceiling for the remuneration of government deposits until 30 April 2023, thereby reducing market concerns that a large portion of government deposits held with the Eurosystem would be placed in the repo market. The debt management offices of Germany and Italy announced further measures to facilitate the functioning of the repo market. As of 10 November the Eurosystem increased the securities lending limit against cash to €250 billion (from €150 billion), in order to pre-empt potential concerns around the year-end and support market functioning in general. Furthermore, the TLTRO III early repayment operations have also helped increase the availability of collateral eligible for use in repo operations by releasing some marketable collateral with which TLTRO borrowing had been collateralised.

For further details on autonomous factors, see the article entitled “The liquidity management of the ECB”, Monthly Bulletin, ECB, May 2002.

Securities held in the outright portfolios are carried at amortised cost and revalued at the end of each quarter, which also has an impact on the total averages and the changes in the portfolios.