Wage developments and their determinants since the start of the pandemic

Wage developments and their determinants since the start of the pandemic

Published as part of the ECB Economic Bulletin, Issue 8/2022.

1 Introduction

The coronavirus (COVID-19) pandemic has greatly affected labour markets and wage growth indicators in the euro area. The onset of the pandemic led to the sharpest decline in total hours worked on record. The widespread introduction of job retention schemes to contain the effects of the pandemic helped to keep employment losses moderate – particularly when compared with the decline in GDP – and affected developments in labour compensation. The containment measures and the pandemic-induced shifts in demand and supply for goods and services also led to more diverse employment and wage dynamics across sectors. More recently, wage growth has been driven by the exceptional strength of the economic rebound post-reopening and the Russian invasion of Ukraine, both contributing to an unprecedented surge in consumer price inflation. At the same time consumer confidence in the euro area dropped abruptly following the invasion and uncertainty about the economic outlook rose. The combination of these factors has made assessing underlying wage pressures and the outlook for wage growth extremely challenging. Issues related to the statistical treatment of government support in the context of job retention schemes add to these difficulties.

Wage growth indicators have been extremely volatile since the start of the pandemic, partly owing to the impact of job retention schemes, complicating the assessment of wage developments. Large pandemic-related swings in hours worked and, to a much lesser extent, employment have resulted in more volatile annual growth rates for compensation per employee and compensation per hour, which are typically the main indicators used to assess wage growth in the euro area.[1] Job retention schemes introduced by governments to prevent large-scale job losses have had a differing impact on employment and hours worked, creating a wedge between growth in compensation per employee and growth in compensation per hour. Different statistical treatments of these support measures have also made it difficult to compare wage developments across euro area countries.

In this unusual economic environment, standard empirical models provide only limited help in analysing wage developments in the euro area. Normally, wage developments can be assessed against empirical regularities by observing the Phillips curve, which links wage growth to economic or labour market slack, past and/or expected inflation, and productivity. During the pandemic, however, wage growth indicators as well as indicators of economic activity and labour market slack have followed patterns that deviate strongly from historical regularities, making it harder to interpret results obtained from the usual empirical models.[2] As a result, assessing underlying wage pressures has become a lot more challenging and requires an in-depth analysis of the impact of the pandemic on different indicators of wage growth.

This article discusses wage developments and the main factors that have influenced them since the start of the pandemic. First, it reviews developments in a broad range of wage measures for the euro area since the start of the pandemic and discusses their usefulness as signals of wage pressures. It also proposes approaches to adjust for the impact of job retention schemes on the growth in compensation per employee (CPE growth) and compensation per hour (CPH growth). Second, the article looks at how wage developments have differed across sectors, reflecting the heterogeneous impact of the pandemic shock. Finally, it discusses the impact of inflation on wage growth in the euro area by examining developments in consumer and producer wages for the economy as a whole and in its main sectors.

2 Euro area wage growth since the start of the pandemic – assessing underlying wage pressures

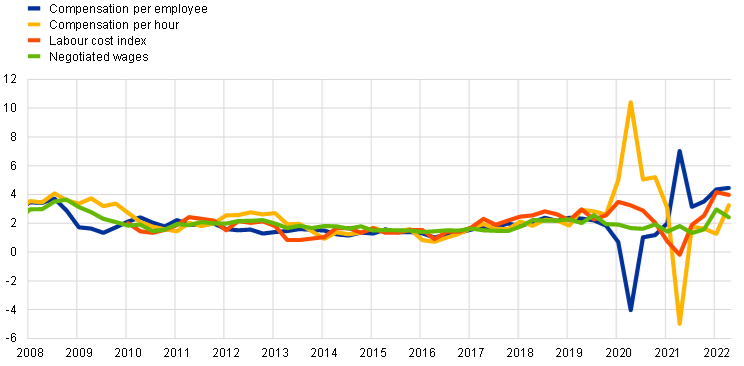

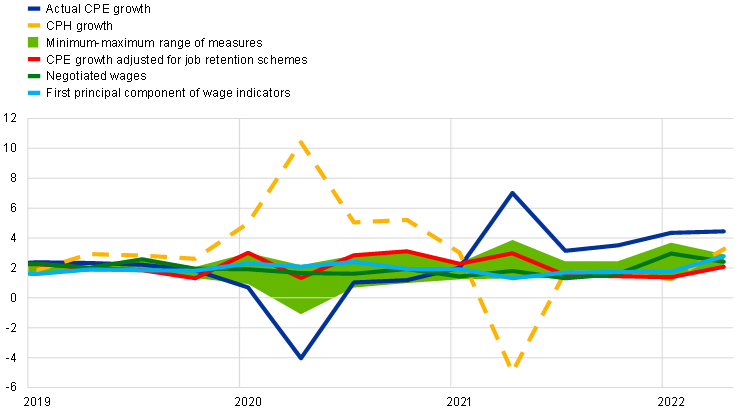

The pandemic has led to an unusual divergence between measures of euro area wage growth (Chart 1). A key indicator in the assessment of wage growth in the euro area is the annual growth rate of compensation per employee. This reflects the labour costs payable by employers – including wages, salaries and employers’ social contributions – expressed as an average per employee. CPE growth declined considerably at the start of the pandemic and during most of 2020, whereas indicators of wage growth per hour worked, such as compensation per hour and Eurostat’s labour cost index, rose.[3] These indicators also remained volatile in 2021 owing to base effects. These developments are heavily influenced by statistical factors linked to the pandemic and the use of job retention schemes, which distorted the information content of CPE and CPH growth during this period. By contrast, the ECB’s indicator of negotiated wages, which captures the outcome of collective bargaining processes, remained relatively stable during 2020-21. The differences in the growth rates of different wage measures have moderated over time but remain substantial. For example, in the second quarter of 2022 indicators of year-on-year wage growth ranged from 2.4% (negotiated wages) to 4.5% (compensation per employee).

Chart 1

Measures of euro area wage growth

(annual percentage growth)

Sources: ECB and Eurostat.

Note: The latest observations are for the second quarter of 2022.

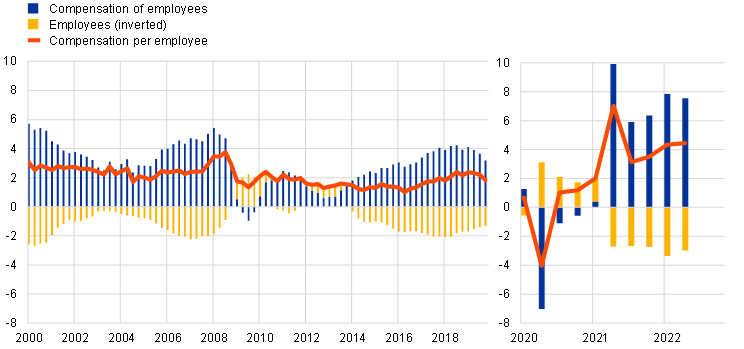

Compensation per employee declined strongly during the pandemic, heavily affected by job retention schemes (Chart 2). Total labour input at the start of the pandemic fell substantially, by around 16%, owing mainly to the drop in hours worked per employee.[4] Measures of compensation per hour increased significantly as a result, given the lower denominator. By contrast, total compensation of employees declined by 7.0% in the second quarter of 2020 on a year-on-year basis as job retention schemes cushioned employment losses and governments compensated part of the decline in wages through transfers. Furthermore, while job retention schemes prevented major job losses, the number of employees still fell, counteracting somewhat the decline in compensation per employee.[5] As a result, compensation per employee fell by 4.0% year on year in the second quarter of 2020, resulting in the lowest annual growth rate in any quarter since 1999. Compensation of employees and the number of employees both recovered in 2021 when the economy reopened, and their contributions to CPE growth changed signs. However, base effects implied a spike in CPE growth and continue to distort it.

Chart 2

Decomposition of compensation per employee growth into compensation of employees and number of employees

(annual percentage growth and percentage point contributions)

Sources: Eurostat and ECB staff calculations.

Note: The latest observations are for the second quarter of 2022.

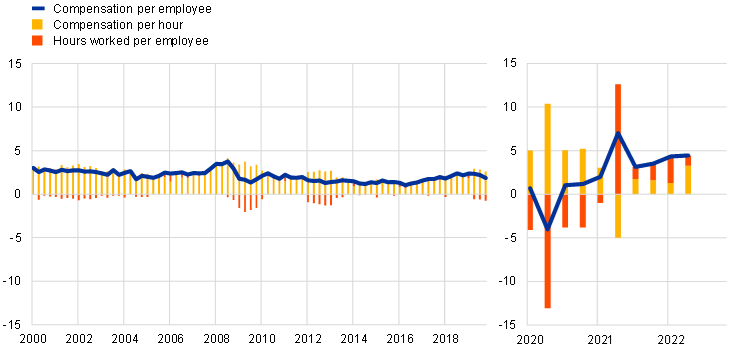

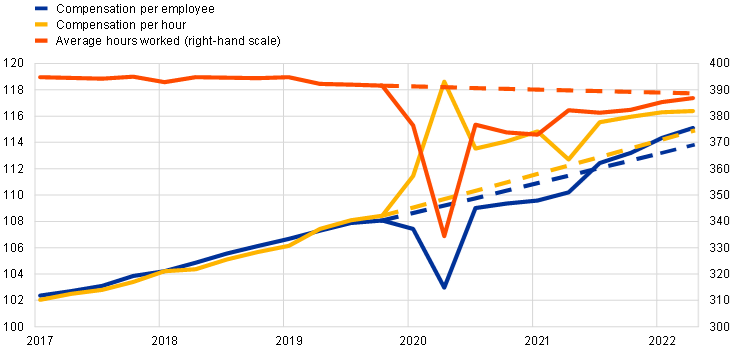

Pandemic-related support measures drove a large wedge between compensation per employee and compensation per hour. Compensation per employee declined considerably in the second quarter of 2020, whereas compensation per hour rose exceptionally strongly, by 10.4%. The difference in growth rates between the two indicators moderated in the third quarter of 2020 but increased again in 2021 (Chart 1), partly reflecting base effects from 2020.[6] The volatility of hours worked per employee caused by job retention schemes contributed decisively to this wedge. The schemes helped enrolled workers retain their employment status but with reduced compensation, thus decreasing compensation per employee. However, as hours worked fell by a lot more than pay, compensation per hour increased (Chart 3).[7] The statistical recording of government support paid under the job retention schemes is also likely to have affected the wedge between compensation per employee and compensation per hour. In some countries, government support was not recorded as compensation of employees because it was paid as a direct transfer to households, whereas in others, government payments were recorded as part of compensation of employees because they were considered a reimbursement to employers.[8]

Chart 3

Decomposition of compensation per employee growth into compensation per hour growth and the average hours worked per employee

(annual percentage growth and percentage point contributions)

Sources: Eurostat and ECB staff calculations.

Note: The latest observations are for the second quarter of 2022.

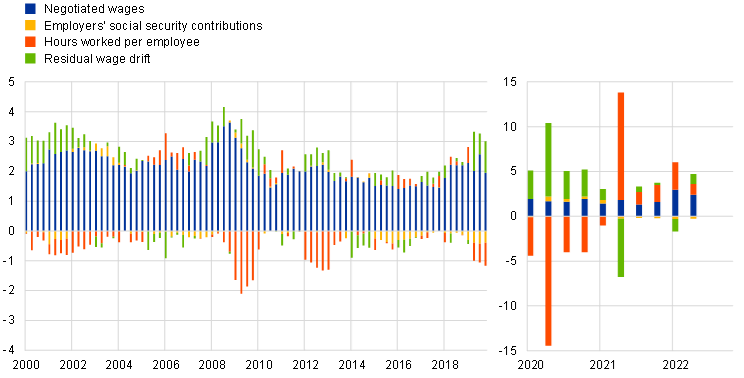

The pandemic-related distortions have become much smaller in recent quarters, but developments in hours worked per employee continue to be an important driver of growth in compensation per employee. CPE growth can be decomposed into negotiated wages, social security contributions, hours worked per employee and the residual wage drift. This decomposition suggests that the impact of pandemic-related distortions declines as job retention schemes wind down. The wage drift, which since the start of the pandemic has largely reflected the subsidies paid by governments to employers, had a significant role in explaining CPE developments during 2020 and the first half of 2021.[9] Since then, however, its role has moderated, and the recovery of hours worked per employee and more recently the pick-up in negotiated wages have accounted for most of the increase in CPE growth (Chart 4).

Chart 4

Decomposition of compensation per employee growth and role of negotiated wage growth

(percentage point contributions to annual percentage growth)

Sources: Eurostat, ECB and ECB staff calculations.

Note: The latest observations are for the second quarter of 2022.

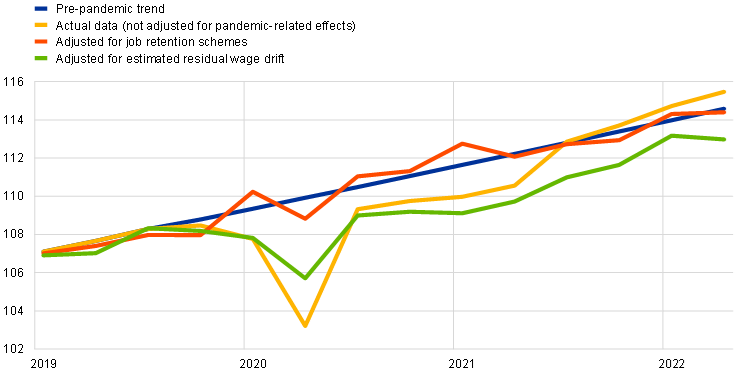

One way to look through the pandemic-related distortions of wage measures is to estimate compensation per employee adjusted for the impact of the job retention schemes. However, this is not straightforward. Without job retention schemes, the decline in GDP and total labour input would probably have been similar, but the adjustments in employment and average hours worked may have been different, with implications for the compensation measures. It is possible to estimate the path of adjusted wage measures by making some assumptions about the counterfactual path of the various components. A principal component analysis of wage growth indicators and negotiated wage growth can also be used to assess underlying wage measures. Chart 5 shows the range of these different estimates using a variety of methods. Overall, these approaches result in smoother series and suggest more moderate wage growth than the headline indicators. At the same time, the differences between these adjusted indicators illustrate the uncertainty around underlying wage growth during the pandemic.

Chart 5

CPE growth and estimates for underlying wage growth

(annual percentage growth)

Sources: Eurostat and ECB staff calculations.

Notes: The range includes six series: (i) negotiated wage growth; (ii) Christiano-Fitzgerald filter (with a cut-off of 2 and 32 quarters); (iii) a Hodrick-Prescott filter with a lambda of 1,600; (iv) the CPE series adjusted for the impact of the job retention schemes, which uses data on the government subsidies that firms received and information (including estimates) on the number and total hours worked by workers in job retention schemes; (v) the CPE series adjusted for the wage drift, which relies on the pre-pandemic relationship between the wage drift (the most cyclical part of wage growth) and business cycle indicators (GDP growth, total labour input growth, industrial production and the unemployment rate); the range includes the average of estimates using 12 specifications; and (vi) the principal component of different wage measures. The latest observations are for the second quarter of 2022.

The ECB’s indicator of negotiated wage growth, which has been less distorted by the pandemic than other indicators, has remained relatively stable. Negotiated wage growth captures the outcome of collective bargaining processes with respect to the level of salaries for a specified number of working hours, so it should be less affected by actual developments in average hours worked or by government subsidies. Negotiated wage growth slowed somewhat in 2020 and 2021, likely reflecting the worsening economic conditions and heightened uncertainty at that time. In addition, the high number of people working remotely and the alternative ways of rewarding employees during the pandemic (which included one-off support for teleworking or pandemic-related payments) may have kept wage demands low. Negotiated wages have started to pick up, albeit moderately, in recent quarters, with compensation for higher inflation and labour shortages in some sectors playing an important role. As a result, agreements signed in 2022 have been characterised by higher negotiated wage increases compared with previous years (Chart 1). In some countries, such as Germany, the wage increases have mainly been passed on to workers in the form of larger than usual one-off payments rather than permanent increases in base wage rates. Although negotiated wage growth has become a more important means of assessing underlying wage pressures since the start of the pandemic, given the significant volatility of the other wage indicators, its use comes with caveats. First, this measure does not cover all euro area countries, and the methodology is not fully harmonised across the countries for which negotiated wage series are available. For example, the sectoral coverage and the inclusion of wage indexation and one-off payments, which have become more significant recently, vary across economies. Second, negotiated wage growth tends to react to changes in labour market conditions with a lag of some quarters and, in a crisis, generally more slowly than CPE growth, for example, as agreements are signed for a year or more.[10]

Estimating the common drivers across a range of wage indicators also suggests that wage pressures have remained moderate. Another way to mitigate the impact of pandemic-related distortions in the assessment of wage pressures is to estimate underlying wage growth pressures across different wage indicators. The results of such a principal component analysis conducted using a broad range of wage indicators are shown in Chart 5. The first principal component across different wage indicators moved sideways from the onset of the pandemic to the start of 2022, when it started to pick up.[11] This is consistent with the view that overall wage growth remained modest during the pandemic, with wage pressures showing a moderate increase more recently amid high inflation – in line with the ECB’s indicator of negotiated wage growth.

Looking through the volatility of the past few years, the main wage indicators stand slightly above the levels implied by their long-term trends over the period 1999-2019 (Chart 6). In the second quarter of 2022 compensation per employee was slightly above the level implied by its pre-pandemic long-term trend (based on a long-term average annual growth rate of 2.1%). This slight upward deviation primarily reflects developments in compensation per hour, which also stood slightly above the level implied by its pre-pandemic long-term trend (based on a long-term average annual growth rate of 2.3%), while average hours worked are close to the downward trend that would have been present had pre-pandemic developments continued.

Chart 6

Compensation per employee, compensation per hour and average hours worked in relation to their linear long-term trends

(left-hand scale: index: 2015 = 100; right-hand scale: quarterly average of hours worked per salaried employee)

Sources: Eurostat and ECB staff calculations.

Notes: The linear trends are calculated by applying the long-term average growth rates for the period 1999-2019. The latest observations are for the second quarter of 2022.

Chart 7

Compensation per employee and adjusted compensation per employee levels compared with the long-term trend

(index: 2015 = 100)

Sources: Eurostat and ECB staff calculations.

Notes: The linear trends are calculated by applying the long-term (1999-2019) average growth rate of compensation per employee since 2019. The latest observations are for the second quarter of 2022.

Overall, underlying wage growth has been relatively moderate since the start of the pandemic, and it now stands close its long-term trend. The volatility caused by the pandemic and the government measures implemented to cushion its impact occurred mainly at the start of the pandemic. Wage growth normalised somewhat following the reopening of the economy, the loosening of pandemic-related restrictions and the strong base effects starting to fall out of the equation after the second quarter of 2021. However, the impact of job retention schemes on CPE growth and CPH growth is still quite substantial. Adjusting for the effects of these schemes brings current CPE growth quite close to its historical average, and compensation per employee for the adjusted series is also returning to its pre-pandemic trend. All things considered, this supports the view that CPE growth continues to move along pre-pandemic trends. Wage dynamics are also moderate compared with the United States (Box 1).

Box 1

Comparing labour market developments in the euro area and the United States and their impact on wages

The purpose of this box is to assess labour market developments in the euro area and the United States, in particular the tightening of labour market conditions and its impact on wages.[12]

Labour input, as measured by total hours worked, recovered strongly in both the euro area and the United States on the back of different adjustment patterns and government support throughout the crisis. Euro area countries implemented policies aimed at preserving employment contracts, whereas the US economy was strongly supported by a fiscal package in the recovery phase. This meant that, while there was a large decline in overall labour input in both economic areas, the extent and, in particular, the composition of this change differed, and the recovery was somewhat faster in the United States. Regarding the composition of the change in labour input, the number of persons employed was more stable in the euro area than in the United States. The decline in total labour input in the euro area was driven primarily by average hours worked, whereas unemployment was the primary adjustment channel in the United States. Hours worked per employee actually increased in the United States, reflecting compositional effects, as workers in the services sector and part-time workers were particularly affected by the crisis.[13] By contrast, hours worked per employee in the euro area are still below pre-pandemic levels, although the latest figures are broadly in line with the longer-term downward trend seen before the crisis. The decline in labour force participation has been more prolonged in the United States. This has been largely driven by older male workers who decided to retire during the crisis, but is also visible across most age and gender groups. The equivalent impact on the labour force was less pronounced in the euro area.[14] Finally, immigration in the euro area was negatively affected by the pandemic,[15] restraining working age population growth, whereas the working age population increased moderately in the United States. Consequently, labour market participation in the United States continues to be below its pre-crisis level in contrast to the euro area, where the labour force participation rate exceeds the level seen before the pandemic (Chart A).

Chart A

Change in total labour input and its decomposition in the euro area and the United States

(percentages and percentage point contributions; cumulative change compared with the level in Q4 2019)

Sources: Eurostat and Haver Analytics.

Notes: Population refers to people aged 15-74 in the euro area and people aged 16 and over in the United States. The latest observations are for the second quarter of 2022.

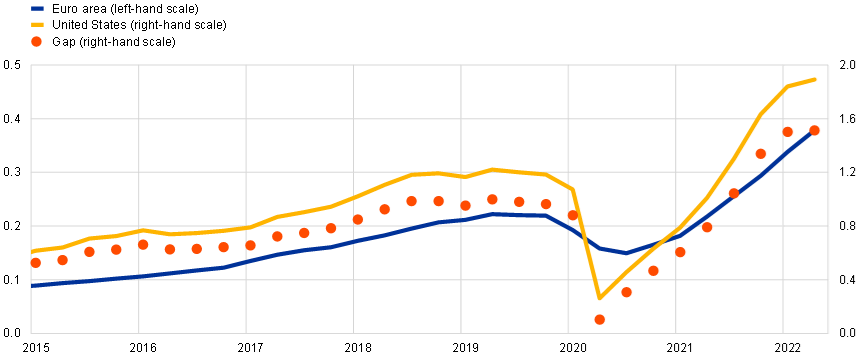

The labour market has tightened a lot more in the United States than in the euro area, in part reflecting the more advanced phase of the US business cycle. Labour market tightness is assessed using the ratio of vacancies to unemployment. In the short run, the indicator varies in response to economic activity over the business cycle. Over the longer run, it tends to be lower in the euro area than in the United States, reflecting the latter’s more dynamic labour market but also differences in the recording of open positions. Chart B shows that, in line with the decline in economic activity, labour market tightness fell to a very low level in the second quarter of 2020, particularly in the United States, but has since recovered quickly to reach record levels in the first half of 2022 in both economic areas. Recent data suggest that the gap in labour market tightness between the euro area and the United States has increased compared with before the pandemic. In the euro area, the recent increase in labour market tightness is dampened by a larger supply of labour than before the pandemic. Despite demographic factors increasingly constraining labour supply, the labour force as a whole has significantly exceeded pre-pandemic levels, to some extent matching increasing labour demand.[16] For the United States, the latest developments point to some stabilisation, as also confirmed by the decline in the quits rate – employees who left voluntarily as a percentage of total employment – which is also a good proxy for labour market tightness. Labour market tightness in the United States is broad-based across industries, but can be attributed in large part to the delay in reincorporating workers in certain industries, particularly leisure and hospitality.

Chart B

Labour market tightness in the euro area and the United States

(ratio of vacancies to unemployment)

Sources: Eurostat, Haver Analytics, Bureau of Labor Statistics and own calculations.

Notes: The gap refers to the figure for the United States minus the figure for the euro area. In France, vacancies are only reported for firms with ten or more employees. The latest observations are for the second quarter of 2022.

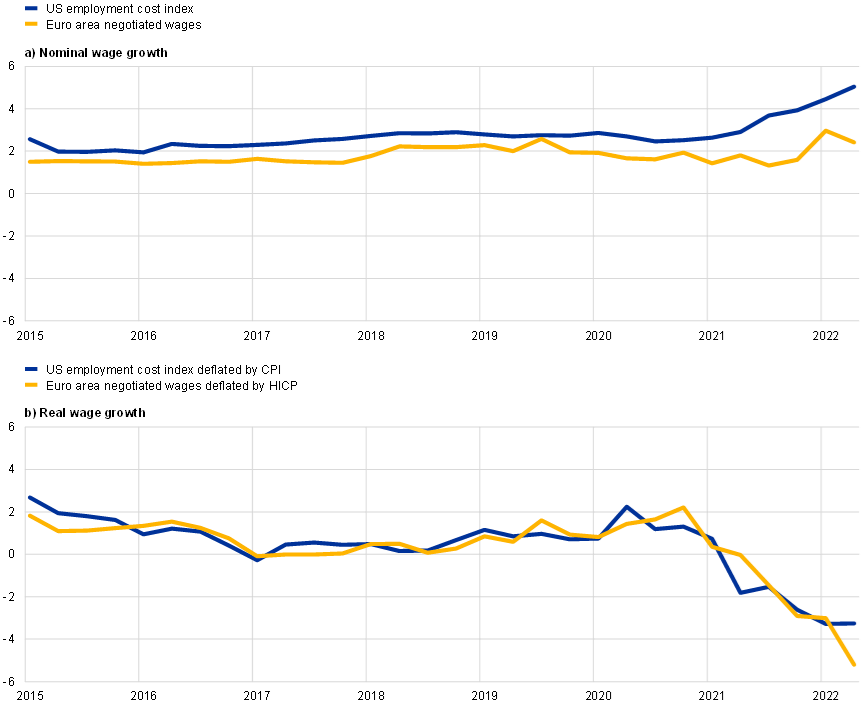

Since the start of the recovery, wage growth in the United States has been stronger than in the euro area, partly reflecting greater labour market tightness.[17] This can be attributed to the different stage of the business cycle in the United States and the country’s stronger aggregate demand, which is due in part to the more expansionary fiscal policies aimed at supporting household income – via stimulus cheques and enhanced unemployment benefits. At the same time, it is also due to differences in labour supply and demand. Since the trough of the pandemic crisis in the second quarter of 2020, US nominal wage growth has increased substantially to reach 5.0% in the second quarter of 2022, whereas the rise in euro area wage growth has been more gradual and limited, with negotiated wage growth standing at 2.4% in the second quarter of 2022 (Chart C, panel a). In the United States, wage pressures were initially only present in those sectors that were more exposed to the pandemic, notably leisure and hospitality. These then spread to other sectors from mid-2021 and are now broad-based. The differences in the wage growth trajectories can also be seen in the developments in US core inflation, which has been higher than euro area core inflation since the beginning of the recovery.[18] Nevertheless, real wages have been declining in both the euro area and the United States since the second quarter of 2021. In the first half of 2022 the more gradual growth of nominal wages in the euro area led to a stronger decline in real wages compared with the United States. In the second quarter of 2022 the real annual growth rate of the US employment cost index was -3.3%, while for negotiated wages in the euro area it was -5.2% (Chart C, panel b). Looking ahead, given the differences in labour market tightness, wage growth may remain stronger in the United States than in the euro area.

Chart C

Measures of wage growth in the euro area and the United States

(annual percentage changes)

Sources: Eurostat, Haver Analytics and ECB staff calculations.

Note: The latest observations are for the second quarter of 2022.

3 A sectoral perspective on wage growth developments in the euro area since the start of the pandemic

Wage growth has varied greatly across the main sectors of the economy since the start of the pandemic.[19] The pandemic and the government measures to cushion its impact have contributed to large differences in sectoral value added, average hours worked, productivity and, in particular, wage growth. This reflects the differing extents to which containment measures, supply disruptions and the participation in job retention schemes affected different sectors during the pandemic. Because of this, sectoral data are even harder to interpret than aggregate data. For example, activity and labour input were affected most significantly and persistently in contact-intensive services, such as accommodation, food services, transport, personal services and recreation including sports and entertainment. These sectors also recorded a strong recovery during the reopening phase, although it is difficult to disentangle the impact of the recovery on wage growth from the base effects. To address this, we focus on the change in the level of wages between the last quarter before the pandemic (the fourth quarter of 2019) and the most recent quarter (the second quarter of 2022). We look at five main sectors in the economy: industry (excluding construction), construction, contact-intensive services (including trade, transport, accommodation and other services), non-contact-intensive services (including information and communication, real estate, financial and insurance activities, and professional and administrative services) and public sector services.[20]

The volatility of CPE growth in the euro area has mainly been driven by contact-intensive services. Compensation per employee declined very strongly, by almost 13%, in contact-intensive services after pandemic-related lockdowns were imposed, explaining most of the decline in compensation per employee for the total economy, as this was the sector with the highest share of workers in job retention schemes. As a result, these services are the most affected by base effects, so wage growth here has been strong recently. CPE growth in industry and construction also declined at the start of the pandemic, but to a smaller degree, while wages were relatively smooth in non-contact-intensive services and public services. CPE growth rates over the last 18 months have been above their historical averages for almost all the main sectors.

Compensation per employee is above its pre-pandemic trend, mainly because of developments in the services sectors (Chart 8). Comparing the latest data with the last observation before the pandemic helps to look through the volatility caused by the job retention schemes. Compensation per employee is above its pre-pandemic trend in all private services, both contact-intensive and non-contact-intensive. In these sectors, average hours worked have already returned to pre-pandemic levels, whereas in the other main sectors they have not fully recovered. Compensation per employee for the total economy has also exceeded its long-term trend, again owing mostly to the increase in wages in the services sectors. In non-contact-intensive services, the catch-up is largely due to real estate activities – probably reflecting the strong dynamics of housing markets and, to a lesser extent, professional and administrative services (i.e. those subsectors where demand for their output did not increase because of digitalisation). In contact-intensive services, labour shortages in certain subsectors may explain the strengthening of wage growth in the most recent period.

Chart 8

Compensation per employee in the main sectors and its decomposition compared with pre-pandemic levels and trends

(percentage change, Q2 2019-Q2 2022)

Sources: Eurostat and ECB staff calculations.

Note: The latest observations are for the second quarter of 2022.

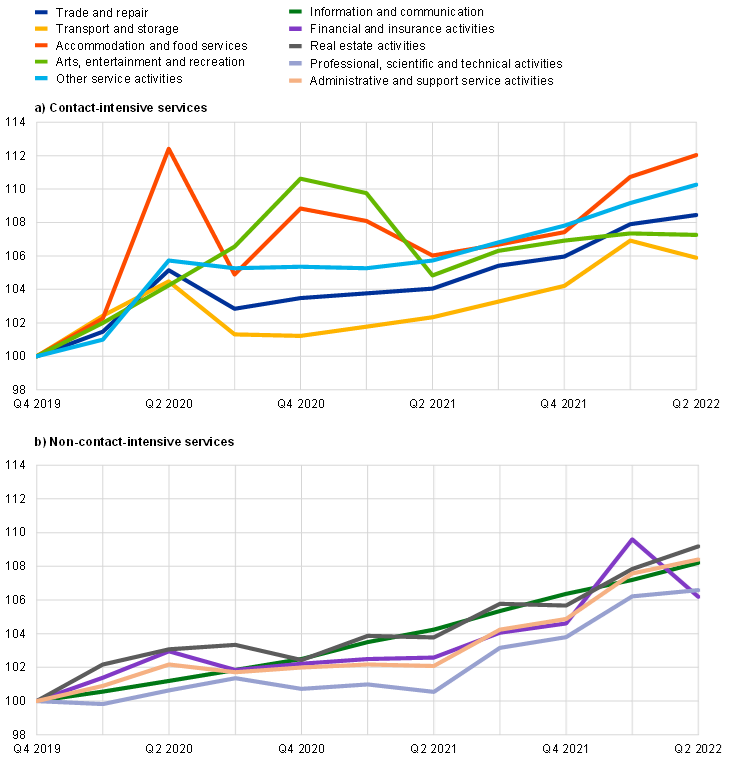

Initially, the pandemic had a strong negative impact on wages in contact-intensive services, but the wage growth rate picked up with the reopening of the economy. Given the dominant role of the services sectors in total economy CPE developments since the start of the pandemic, these sectors should be analysed more closely. We focus on the wages and salaries component of the labour cost index, as the national accounts data provide a more detailed sectoral breakdown for this component than for compensation per employee. In contact-intensive services, hourly wages closely followed the developments in containment and social distancing measures, which caused strong volatility through both hours worked per employee and statistical distortions. By contrast, in non-contact-intensive services sectors such as information and communication, hourly wage growth was less volatile (Chart 9). When comparing the latest data observation for these indicators with their pre-pandemic level, the heterogeneity within contact-intensive services is much greater than within non-contact-intensive services. This reflects the recent strong pick-up in hourly wages in those services sectors where tourism plays a larger role, such as accommodation and food services, transport and trade. This is probably due to the labour shortages experienced in some of these subsectors following the reopening of the economy.

Chart 9

Labour cost index in contact-intensive and non-contact-intensive services sectors

(percentage difference compared with the level in Q4 2019)

Source: Eurostat.

Note: The latest observations are for the second quarter of 2022.

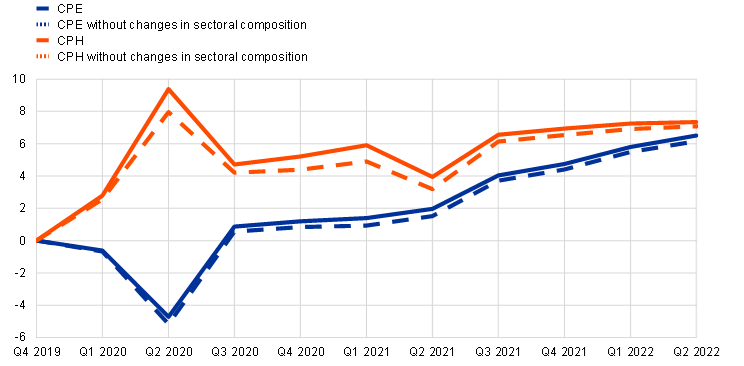

Despite such a varied impact across sectors, changes in overall wage growth owing to sectoral composition remained limited as job retention schemes contained changes of employment. During the recovery, changes in employment across sectors have only had a slight positive impact on compensation per employee and compensation per hour for the total economy (Chart 10). However, the composition of employment has probably changed within sectors, especially in those sectors where employment declined. Such changes, seen for example in the education level, age or gender of workers, could have an impact on wage growth in different sectors. Unfortunately, data limitations mean that these intra-sector shifts cannot be estimated and they remain an area for future research.[21]

Chart 10

Compensation per employee and per hour and the role of compositional changes

(percentage change compared with the level in Q4 2019)

Sources: Eurostat and ECB staff calculations.

Note: The latest observations are for the second quarter of 2022.

4 The impact of inflation on wage growth in the euro area

Looking at real wage developments, which take nominal wage growth and inflation into account, makes it possible to analyse changes in the purchasing power of employees and to evaluate real cost pressures for companies stemming from wages. The purchasing power of employees can be monitored by looking at real consumer wage developments, which are obtained by taking the difference between nominal wage growth and HICP inflation. The real wage from an employer’s perspective is different. It is a cost factor rather than an income item, so the calculation requires a different deflator. Real producer wages can be derived by adjusting the nominal wages using value-added deflators, which measure the prices charged for the production of goods and services in the economy. Real consumer wages indicate how severe purchasing power losses have been for employees. To the extent that employees try to compensate for this loss of purchasing power, this could affect nominal wage demands. Real producer wages reflect the cost pressures implied by nominal wage growth relative to the overall growth in the price of output.

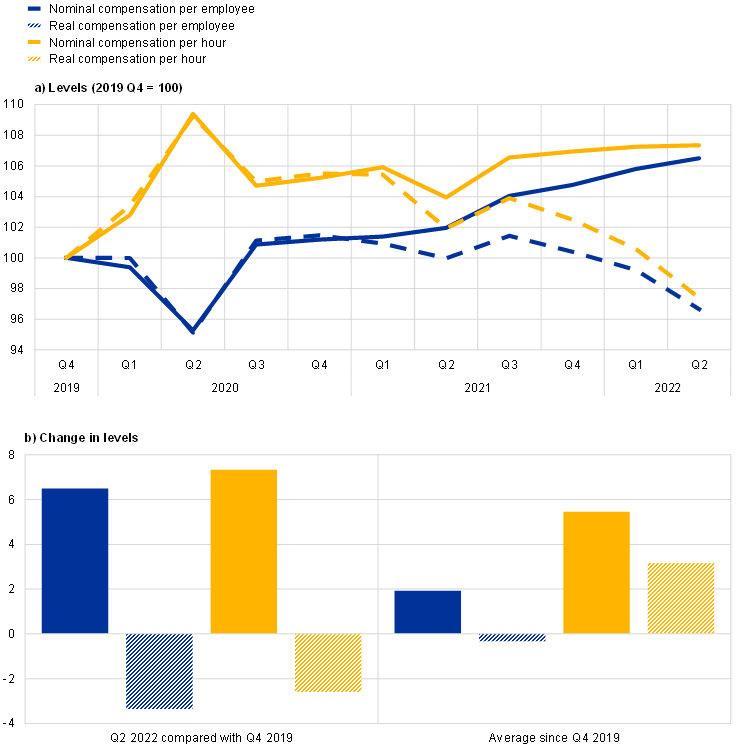

Nominal and real consumer wages developed in a very similar way in 2020 before diverging strongly from the first quarter of 2021, when consumer price inflation started to pick up (Chart 11).[22] Headline inflation was very low during the initial phase of the pandemic, reflecting low overall price pressures, a substantial negative contribution of energy inflation and other factors such as temporary cuts in indirect taxes to stimulate the economy. Consequently, the wedge between nominal and real consumer wages was quite small, and nominal and real consumer wage developments as reflected in CPE and CPH growth were dominated by the effects of job retention schemes (as discussed in Section 2 above). When inflation started to pick up in 2021 – driven first by energy inflation then also by supply bottlenecks, especially for goods but later on also for services in the context of the economic reopening – a substantial gap opened up between nominal and real consumer wage growth.

Chart 11

Nominal and real wage growth (consumer wages) compared with pre-pandemic levels

(panel a: index: Q4 2019 = 100; panel b: percentage change compared with the level in Q4 2019)

Sources: Eurostat and ECB staff calculations.

Notes: Real compensation per employee and per hour are calculated using HICP (consumer wages). The latest observations are for the second quarter of 2022.

Real consumer wages are now substantially lower than before the pandemic and are likely to fall further in the coming months (Chart 12). Nominal wages have increased at a slower pace than HICP, leading to a decrease in the purchasing power of wages, which in the second quarter of 2022 stood around 3.6% below its level in the fourth quarter of 2019. Over the period from the fourth quarter of 2019 to the second quarter of 2022, employees experienced an average quarterly reduction in their pre-pandemic real wage level of around 0.5%.[23] The further losses in real wages expected over the coming months will increasingly be felt by consumers as a loss in purchasing power compared with before the pandemic. This might increase pressure on trade unions to demand higher pay rises in upcoming negotiation rounds, especially in sectors with lower wages. However, losses in purchasing power are only one factor affecting unions’ wage demands – the tightness of the labour market and the current economic situation are also likely to play a central role.

For the total economy, compared with the levels before the pandemic, real producer wages have decreased a lot less strongly than real consumer wages (Chart 12). In the second quarter of 2022 real producer wages were only 0.5% below their pre-pandemic levels. This is because developments in wage growth as a cost factor were broadly similar to those for the price of output.

Chart 12

Nominal and real growth of producer and consumer wages in the main sectors

(percentage change compared with the level in Q4 2019)

Sources: Eurostat and ECB staff calculations.

Notes: Real consumer wages reflect compensation per employee deflated by HICP, while real producer wages are calculated based on compensation per employee deflated by value-added deflators. The latest observations are for the second quarter of 2022.

Developments in real producer prices have diverged strongly across different sectors of the economy, with implications for expected wage and price pressures. [24] Developments in real producer wages suggest that additional price pressures can be expected, especially in non-contact-intensive services. This is in line with the decrease in unit profits in this sector compared with pre-pandemic levels.[25] While value-added deflators have increased broadly in line with nominal wages in public services, these have increased somewhat more strongly than nominal wages in contact-intensive services and in construction and industry in particular, in line with the large increases in sectoral profits in these sectors.[26]In non-contact-intensive services, however, the deflators have increased a lot less strongly than wages. This suggests that, based on developments in real producer wages with value-added deflators, there is pressure on firms to raise prices in the future or to hold out against additional wage claims. Looking ahead, the good cyclical position of the non-contact-intensive services sectors up to the second quarter of 2022, coupled notably with the tight labour markets, could – if persistent – point to further wage pressures and, subsequently, price increases in these sectors in particular. As these services are to a large degree provided to businesses rather than consumers, such increases are likely to affect HICP only partially, and with a delay.[27]

5 Conclusions

The COVID-19 pandemic and the government measures to cushion its impact have caused exceptionally high volatility in wage growth indicators, which makes it harder to assess wage developments. The effects of job retention schemes introduced by governments to prevent large-scale job losses played a key role in this regard. In this unusual economic environment, well-established empirical models such as wage Phillips curve regressions offer only limited help in assessing wage developments in the euro area. This is because wage indicators and their main drivers have displayed patterns that are way off historical regularities. Their volatility can be understood by taking into account statistical distortions stemming from job retention schemes.

Estimates of underlying wage growth have, on average, remained relatively moderate since the start of the pandemic, but have started to pick up more recently. Adjusting for the effects of job retention schemes using different methods brings CPE growth quite close to its historical average over the period from the start of the pandemic to the second quarter of 2022.

So far there has been no evidence of a change in the wage growth trend in terms of compensation per employee since the start of the pandemic. Looking through the volatility of the past couple of years, the levels of the main wage indicators, like compensation per employee and compensation per hour, currently stand slightly above those implied by pre-pandemic long-term trends. Adjusted for pandemic-related effects, the level of CPE growth has essentially returned to its pre-pandemic long-term trend.

Looking through pandemic-related distortions in wage measures, which have varied greatly across sectors, there are signs of stronger wage growth in services sectors. Wages are above their pre-pandemic levels primarily in those services sectors that have recently seen serious labour shortages.

Taking into account the impact of inflation, real consumer wages are now substantially lower than before the pandemic. This could lead trade unions to demand higher wage increases in upcoming negotiation rounds, especially in sectors with lower wages. For the total economy, real producer wages have decreased far less strongly than real consumer wages when compared with their pre-pandemic levels in the fourth quarter of 2019. This has largely been driven by non-contact-intensive services.

Looking ahead, wage growth over the next few quarters is expected to be very strong compared with historical patterns. This reflects robust labour markets that so far have not been substantially affected by the slowing of the economy, increases in national minimum wages and some catch-up between wages and high rates of inflation. Beyond the near term, the expected economic slowdown in the euro area and uncertainty about the economic outlook are likely to put downward pressure on wage growth.

For more details, see Nickel, C., Bobeica, E., Koester, G., Lis, E. and Porqueddu, M. (eds.), “Understanding low wage growth in the euro area and European countries”, Occasional Paper Series, No 232, ECB, Frankfurt am Main, September 2019, revised December 2020.

See, for example, Bobeica, E. and Hartwig, B., “The COVID-19 shock and challenges for time series models”, Working Paper Series, No 2558, ECB, Frankfurt am Main, May 2021, or Lenza, M. and Primiceri, G.E., “How to estimate a VAR after March 2020”, Working Paper Series, No 2461, ECB, Frankfurt am Main, August 2020.

The labour cost index measures developments in compensation per hour, including employers’ social security contributions and taxes paid less any subsidies received by employers.

Total hours worked by salaried employees declined by 15.8% year on year in the second quarter of 2020. Over the same period total hours worked by all workers (i.e. salaried employees and self-employed workers) declined by 17.3%. See also the article entitled “The impact of the COVID-19 pandemic on the euro area labour market”, Economic Bulletin, Issue 8, ECB, 2020.

A positive contribution from the falling number of employees to the growth of compensation per employee is characteristic of recessions and was also observed during the global financial crisis and the sovereign debt crises in some euro area countries. This partly reflects compositional effects, as workers on low wages are generally the first to be dismissed during a recession.

Looking through the volatility caused by base effects, the quarter-on-quarter growth rates of the different wage measures have been aligned and moderate since the second half of 2021.

See the box entitled “Developments in compensation per hour and per employee since the start of the COVID‑19 pandemic” in the article entitled “The impact of the COVID-19 pandemic on the euro area labour market”, Economic Bulletin, Issue 8, ECB, 2020.

See also the box entitled “Wage dynamics across euro area countries since the start of the pandemic” in this issue of the Economic Bulletin and the box entitled “Short-time work schemes and their effects on wages and disposable income”, Economic Bulletin, Issue 4, ECB, 2020. The strong negative correlation between average hours worked and compensation per hour was also characteristic of the recession following the global financial crisis, when job retention schemes were also used in some euro area countries, albeit to a much lesser extent than during the pandemic.

For an explanation of the wage drift, see the box entitled “Recent developments in the wage drift in the euro area”, Economic Bulletin, Issue 8, ECB, 2018.

See also the box entitled “Assessing wage dynamics during the COVID-19 pandemic: can data on negotiated wages help?”, Economic Bulletin, Issue 8, ECB, 2020.

This component captures 34% of the variability of all different wage measures.

The box compares the developments in the US employment cost index with negotiated wages in the euro area, which are the measures least affected by statistical distortions stemming from pandemic-related public support schemes.

See also Gomez-Salvador, R. and Soudan, M., “The US labour market after the COVID-19 recession”, Occasional Paper Series, No 298, ECB, Frankfurt am Main, July 2022.

See the box entitled “COVID-19 and retirement decisions of older workers in the euro area“, Economic Bulletin, Issue 6, ECB, 2022.

See the box entitled “The role of migration in weak labour force developments during the COVID-19 pandemic”, Economic Bulletin, Issue 1, ECB, 2022.

See the box entitled “Labour supply developments in the euro area during the COVID-19 pandemic”, Economic Bulletin, Issue 7, ECB, 2021.

For the United States, we focus on the employment cost index as a measure for wage costs as it captures all elements of employee compensation (including benefits) and, unlike other measures such as hourly wages, is not affected by compositional changes in employment. This is in contrast to the average hourly earnings, which were strongly affected by compositional effects because employment declined more strongly in low-wage industries during the pandemic.

See the box entitled “Recent inflation developments in the United States and the euro area – an update”, Economic Bulletin, Issue 1, ECB, 2022.

See also the discussion in the box entitled “The role of sectoral developments for wage growth in the euro area since the start of the pandemic”, Economic Bulletin, Issue 5, ECB, 2021.

See also Bandera, N., Bodnár, K., Le Roux, J. and Szörfi, B., “The impact of the COVID-19 shock on euro area potential output: a sectoral approach”, Working Paper Series, No 2717, ECB, Frankfurt am Main, September 2022.

For a detailed assessment of such compositional effects in the euro area in the pre-pandemic period, see the article entitled “The effects of changes in the composition of employment on euro area wage growth”, Economic Bulletin, Issue 8, ECB, 2019.

See the article entitled “The role of demand and supply factors in HICP inflation during the COVID-19 pandemic – a disaggregated perspective”, Economic Bulletin, Issue 1, ECB, 2021, or Nickel, C., Koester, G. and Lis, E., “Inflation Developments in the Euro Area Since the Onset of the Pandemic”, Intereconomics, Vol. 57, No 2, pp. 69-75.

The largest part of payments made under job retention schemes is already included in wage measures like compensation per employee. Adding support paid to employees in the form of transfers or other social benefits (which are not included in compensation per employee) does not change the picture substantially.

Real producer wages could also be analysed by deflating wages using producer price indices (PPI). These are available for industry or construction, but there are data limitations for services. PPIs measure gross output prices, whereas the value-added deflator measures only the price of value added (i.e. the difference between gross output and intermediate inputs). Real producer wages in construction, and even more so in industry, decrease far more strongly when deflated by PPIs. This probably reflects significant increases in intermediate costs (going well beyond increases in wage costs), which push up gross output prices in particular (reflected in PPIs).

For a more complete picture, it would be interesting to assess the role of differences in input costs (including energy) in this cross-sectional analysis, for example by assessing real producer wage developments also based on PPIs, which reflect output prices and include costs of intermediate inputs. For services, however, this is hindered by data limitations (see the previous footnote).

Compared with pre-pandemic levels, sectoral unit profits increased strongly in manufacturing and construction as well as in contact-intensive services like trade, transport, and accommodation and food services. Sectoral unit profits decreased compared with pre-crisis levels in non-contact-intensive services like professional, business and support services. For further details, see slide 6 of Schnabel, I., “Monetary policy in a cost-of-living crisis”, Remarks at a panel on the “Fight against inflation” at the IV Edition Foro La Toja, 30 September 2022.

Inflation can also affect wage growth via indexation mechanisms or increases in minimum wages, which are often motivated by large changes in inflation. For an assessment of these mechanisms, see the box entitled “The prevalence of private sector wage indexation in the euro area and its potential role for the impact of inflation on wages”, Economic Bulletin, Issue 7, ECB, 2021, and the box entitled “Minimum wages and their role for euro area wage growth”, Economic Bulletin, Issue 3, ECB, 2022.