US dollar funding tensions and central bank swap lines during the COVID-19 crisis

Published as part of the ECB Economic Bulletin, Issue 5/2020.

US dollar funding conditions started to become tense around the end of February 2020 when supply-demand imbalances led to rising funding premia amid volatile financial markets. This box focuses on these tensions in the foreign exchange (FX) swap market, where market participants lend funds in two currencies (e.g. the euro and the US dollar) to each other with the commitment to swap these funds back at a later date and at a pre-agreed exchange rate. The box provides evidence on the positive impact of the swap lines between central banks on the functioning of the EUR/USD FX swap market. These central bank swap lines enable the Eurosystem to provide US dollars to euro area banks.[1] The enhancement of these swap lines and the subsequent supply of US dollars via more frequent liquidity-providing operations not only helped banks to satisfy their immediate US dollar funding needs but also supported market activity, as banks participating in the US dollar operations became more willing to intermediate and passed funds borrowed from the Eurosystem on to other market participants. This was key to reducing tensions on US dollar funding conditions and restoring orderly market functioning in the EUR/USD FX swap market. The analysis is based on market transaction data gathered through the ECB Money Market and Statistical Reporting (MMSR)[2].

In the context of high market volatility and risk aversion due to the coronavirus (COVID-19) pandemic, the EUR/USD FX swap basis spread – an important indicator of US dollar funding costs for European banks – rose significantly. The FX swap basis spread is the difference between the average implied interest rate on borrowing US dollars in the EUR/USD FX swap market and the US dollar risk-free rate, which is represented by the US dollar overnight index swap (OIS) rate. Under normal market conditions, the FX swap basis spread is small[3] and only reflects temporary market frictions, such as those related to balance sheet reporting dates. However, from the end of February, European banks increased the premium that they were willing to pay in order to secure US dollar funding in the EUR/USD FX swap market, which resulted in a wider FX swap basis spread. This reflected a large increase in the demand for US dollars as market participants hoarded cash in anticipation of potential liquidity outflows to the real economy. European banks and corporates that generally have significant business exposure to the US dollar were also affected. On 28 February the overnight FX swap basis spread reached 25 basis points, doubling in only three days. At the same time, the FX swap basis spread in the three-month maturity widened to 49 basis points on 3 March, which was 30 basis points above the average level recorded in February 2020 (see Chart A).

Despite the announcement of enhanced central bank swap lines on 15 March, the premium to borrow US dollars in the EUR/USD FX swap market initially continued to rise, especially in the short-term tenors. Given the deteriorating US dollar funding conditions worldwide, on 15 March the Federal Reserve System, the ECB, the Bank of Japan, the Bank of England, the Swiss National Bank and the Bank of Canada announced coordinated action to enhance the provision of US dollar liquidity through the standing swap line arrangements. [4] The ECB announced that the Eurosystem would offer 84-day operations from 18 March onwards, in addition to the existing 7-day operations. Moreover, the pricing of both operations was lowered by 25 basis points to a level equal to the US dollar OIS rate plus 25 basis points. The announcement itself brought little relief to US dollar funding premia in the EUR/USD FX swap market, particularly in short maturities. Accordingly, short-term US dollar borrowing rates started to grow exponentially and the overnight FX swap basis spread peaked at 644 basis points on 17 March, on the eve of the first US dollar operations under the enhanced swap line conditions.

The allotment of the Eurosystem’s first US dollar operations under more favourable pricing conditions as of 18 March produced significant relief for short-term US dollar funding conditions in the EUR/USD FX swap market, while longer maturities were affected less. On 18 March, when the 84-day US dollar operation was offered for the first time since the spring of 2014, the ECB allotted USD 76 billion to 44 bidders in the 84-day operation and USD 36 billion to 22 bidders in the 7-day operation. The total allotment of USD 112 billion on 18 March was the highest in a single day since 2008. Both operations were substantially cheaper than comparable market prices and, according to market feedback, the significant take-up and large number of participating banks helped to remove the possible stigma attached to banks’ participation in these operations. After the results of the US dollar operations were announced, MMSR reporting agents reported significantly lower US dollar funding premia for short-term transactions, with the overnight FX swap basis spread falling by 476 basis points to 168 basis points. In contrast, the three-month FX swap basis spread temporarily tightened, but to a lesser extent, from 157 basis points to 107 basis points, before rising again to 144 basis points on 19 March. Owing to the highly uncertain market outlook related to potential abrupt US dollar outflows, banks initially hoarded US dollar liquidity obtained via the Eurosystem’s US dollar facility. Only a portion of this liquidity was passed through to the market. This was mostly in shorter tenors, which limited the relief on longer-term US dollar funding premia.

It was only when 7-day US dollar operations were offered on a daily basis as of 23 March[5] that conditions started to improve sustainably across all tenors, as uncertainty about US dollar availability abated. Market participants considered the provision of daily operations to be useful as the daily frequency reduced the uncertainty around the availability of US dollars to accommodate daily funding needs. In addition to the introduction of daily 7-day US dollar operations, the Eurosystem continued to provide weekly operations with a longer maturity of 84 days, which ensured that US dollar funds were available to euro area banks over a longer horizon. These two measures combined supported the gradual pass-through of liquidity obtained in US dollar operations to the market and proved effective in lowering US dollar funding premia.[6]

Chart A

Spread between the US dollar borrowing rate in the EUR/USD FX swap market and the US dollar risk-free rate

(basis points)

Sources: ECB, MMSR, Bloomberg.

Notes: The effective federal funds rate is used as a US dollar risk-free rate for the overnight maturity and US dollar OIS rates are used for the other tenors. The US dollar borrowing rate is the rate paid by MMSR reporting agents to receive US dollars in the EUR/USD FX swap market at different maturities. The overnight US dollar borrowing rate in the EUR/USD FX swap market is based on tomorrow/next day transactions.

US dollar funding costs in the EUR/USD FX swap market remained, however, at elevated levels in the run-up to the March quarter-end. As banks need to report certain regulatory ratios at the quarter-end, they are typically reluctant to expand their balance sheets for intermediation activity that covers the quarter-end. The March quarter-end is also the fiscal year-end for banks in jurisdictions such as Japan, where tax is determined by the size of the balance sheet, therefore the relief from the US dollar operations was reduced around the quarter-end period. As a result, funding conditions in EUR/USD FX swap markets continued to be volatile in the run-up to the quarter-end, in both short and long maturities. The FX swap basis spread in the overnight maturity remained higher than before the COVID-19 crisis and spiked at the March 2020 quarter-end. It reached 209 basis points on 30 March, which was 88 basis points higher than the level recorded at the March 2019 quarter-end. Meanwhile, the three-month FX swap basis spread averaged 95 basis points in the last week of March, about five times as large as the average basis spread recorded in February 2020.

After the quarter-end, the premium for borrowing US dollars in the EUR/USD FX swap market fell further, US dollar funding conditions started to normalise and the Eurosystem’s US dollar operations gradually lost their appeal, leading to a drop in participation in these operations. FX swap basis spreads gradually normalised throughout April, amid improving market sentiment and abating concerns over the availability of US dollar liquidity. Short-term US dollar funding premia (between one-day and one-week tenors) declined rapidly after the quarter-end and returned to almost pre-pandemic levels by mid-April. Longer-term FX swap basis spreads took longer to normalise but also stabilised at around pre-crisis levels by the end of April. In line with these developments and what was observed in other jurisdictions, the Eurosystem’s US dollar operations started to lose their economic appeal in April. The use of the Eurosystem’s US dollar facility therefore fell considerably over time. In the second half of May, the ECB allotted less than USD 3 billion overall, which was USD 173 billion less than during the second half of March (see Chart B). On 21 April the ECB saw no bids for the first time since the start of the enhanced US dollar operations. Operations with no allotment subsequently became more common, reflecting the normalisation of US dollar funding conditions in the EUR/USD FX swap market.

Chart B

Daily allotment and outstanding amounts in the Eurosystem’s US dollar operations

(USD billions)

Source: ECB.

Market turnover in the EUR/USD FX swap market remained solid throughout the crisis, with market participants initially increasing activity in longer tenors in anticipation of a tightening in US dollar funding conditions. MMSR transaction data show a significant increase in turnover for maturities of more than one month in the weeks preceding the peak of the crisis. This suggests that, as US dollar funding conditions started to deteriorate, market participants attempted to secure US dollar funding at prevalent prices in anticipation of further market tightening. Volumes with maturities of more than one month, including forward transactions, remained elevated until 19 March,[7] which was the settlement date for the first enhanced US dollar operation. Driven by higher longer-term trading volumes, total daily market turnover between 25 February and 19 March increased by more than one-third on average, compared with the rest of February 2020, to around USD 250 billion (see Chart C).

Central bank US dollar operations supported the functioning of the EUR/USD FX swap market as the US dollar funding borrowed from the Eurosystem found its way to the market. However, a general shift towards shorter maturities was observed. Overall, activity in the EUR/USD FX swap market remained elevated following the launch of the enhanced US dollar provision by the central banks and increased further after the March quarter-end. This indicates that funds borrowed by banks in the Eurosystem’s operations were passed on to other market participants, helping to satisfy additional crisis-related demand for US dollars. The increase in activity in the EUR/USD FX swap market in April was primarily observed in short-term maturities, reflecting the high levels of risk aversion and market participants’ preference to lend surpluses in the market primarily in short tenors. In particular, the volume of one-day transactions increased by more than 50% after the March quarter-end, from a daily average of USD 118 billion in the first quarter of 2020 to a daily average of USD 184 billion in the period between 1 and 20 April. Finally, volumes and maturity composition returned to pre-crisis levels at the end of April.

Chart C

EUR/USD FX swap daily transaction volume by maturity

(USD billions)

Sources: ECB, MMSR.

Notes: The daily transaction volume takes into account both lending and borrowing trades reported by MMSR reporting agents in the EUR/USD FX swap market segment.

Banks participating in the Eurosystem’s US dollar operations passed the funds on to other market participants, thereby providing relief to US dollar funding conditions in the EUR/USD FX swap market, especially in short maturities. In particular, MMSR transaction data show that a large group of euro area banks participating in the Eurosystem’s US dollar operations increased their daily US dollar short-term lending volumes significantly. In particular, these lending volumes grew on average by USD 34 billion between 1 and 20 April, amid declining US dollar funding premia. As they are among the largest banks in Europe, MMSR reporting agents usually trade with a large number of counterparties, which means that the US dollar funds are likely to have been distributed widely.[8]

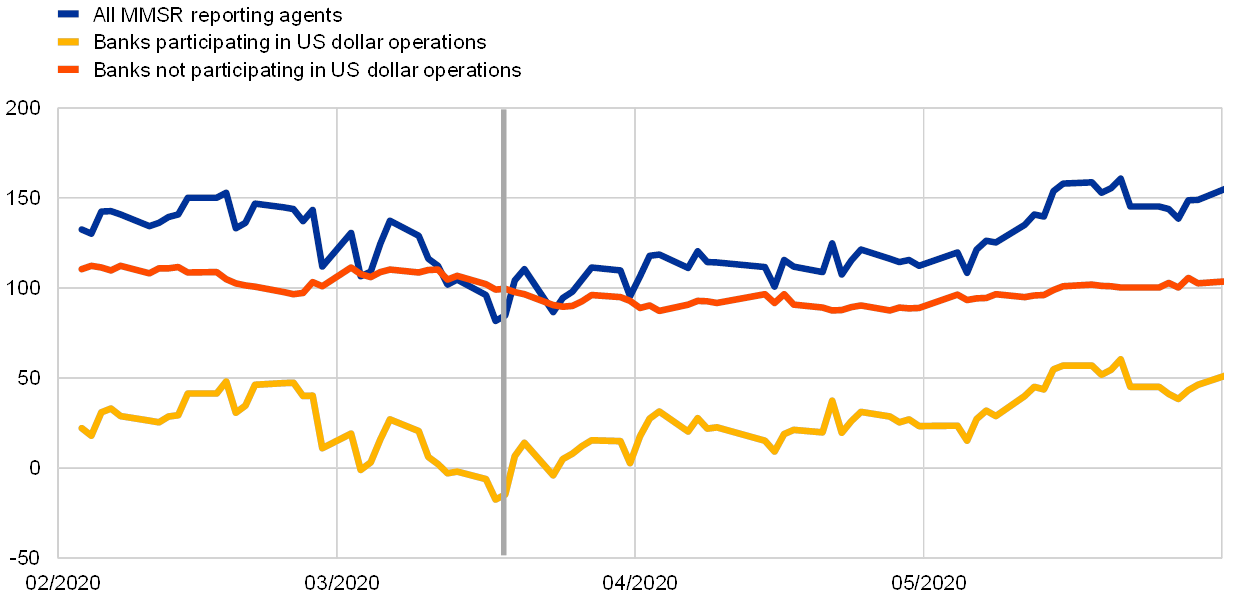

The supply of US dollars via Eurosystem operations allowed large European banks to restore their US dollar intermediation role, which had been disrupted by the crisis in March. MMSR reporting agents are important intermediators in the US dollar market and provide US dollar liquidity to various other market counterparties. Taken together, MMSR reporting agents are usually net lenders of US dollars in the EUR/USD FX swap market. This means that they have a surplus of US dollars which, in normal times, is invested in the EUR/USD FX swap market. However, some reporting agents saw their net lending position – measured by the difference between the volumes of US dollars lent and borrowed by them in the EUR/USD FX swap market – deteriorate as the crisis intensified, and the total net US dollar surplus dropped from USD 153 billion to USD 82 billion (see Chart D). Moreover, the MMSR reporting agents that took part in the Eurosystem's US dollar operations accounted for around three-quarters of total take-up in these operations.[9] Overall, these reporting agents saw a very large decline in their net lending position and even became net borrowers of US dollars in the EUR/USD FX swap market in the run-up to the enhanced US dollar provision, while the net lending position of the other reporting agents decreased only marginally. After these reporting agents took part in the Eurosystem’s US dollar operations, the total net lending position in the EUR/USD FX swap market started to normalise and reached USD 161 billion on 21 May, which was USD 79 billion more than during the peak of the crisis on 17 March. This suggests that the US dollar operations were effective in providing relief to the market and in offsetting the effect of the shocks registered during the first half of March, as market functioning gradually recovered and banks became more willing to intermediate. The swap lines between central banks therefore helped to mitigate the effects of the strains in the US dollar funding market. This supported the supply of credit from banks to households and businesses, both domestically and abroad.

Chart D

Net US dollar lending position of MMSR reporting agents in the EUR/USD FX swap market

(USD billions)

Sources: ECB, MMSR.

Notes: Net position of lending US dollars against euro. The figures are expressed in US dollar equivalent by multiplying the net euro lending position by the EUR/USD spot exchange rate of the day. A negative value indicates a net US dollar borrowing position. The grey line represents the start of the enhanced US dollar operations on 18 March. The participating banks are those MMSR reporting agents that took part in the US dollar operations between 18 March and 7 April 2020.

- Swap lines between central banks allow a central bank (the ECB in this case) to receive foreign currency liquidity (US dollars) from the issuing central bank (the Federal Reserve System), which keeps the recipient currency (the euro) as collateral until maturity. In turn, the recipient central bank lends the foreign currency liquidity that it receives to domestic banks against eligible collateral. In line with the ECB's press release published on 17 June 2014, US dollar tender operations offered by the Eurosystem follow a fixed rate and full allotment procedure, i.e. the ECB satisfies all bids received from counterparties against eligible collateral. In 2011 the ECB, together with the Bank of England, the Bank of Canada, the Bank of Japan, the Federal Reserve, and the Swiss National Bank, established a network of swap lines enabling the participating central banks to obtain currency from each other. For more details, see the ECB’s website and the Federal Reserve’s website.

- The MMSR dataset consists of transaction-by-transaction data of the 50 largest euro area banks, based on the value of balance sheet assets, including their FX swap activity. For more details, see the ECB’s website.

- For instance, FX swap basis spreads in maturities of less than three months were on average smaller than 0.2% in January and February 2020.

- For more details, see the ECB’s press release published on 15 March 2020.

- On 20 March 2020 the Federal Reserve, the ECB, the Bank of Japan, the Bank of England, the Swiss National Bank and the Bank of Canada announced an increase in the frequency of the 7-day maturity operations from weekly to daily. These daily operations commenced on 23 March 2020 and were intended to further enhance the provision of liquidity via the standing US dollar liquidity swap line arrangements. For more details, see the ECB’s press release published on 20 March 2020.

- The effect of the provision of daily operations and of long-term US dollar tenders on US dollar funding conditions for euro area banks was also examined in the ECB’s Monthly Bulletin published in August 2014.

- Between 25 February and 19 March, MMSR reporting agents reported an average daily turnover of USD 45 billion in maturities of more than one month, including forward transactions. This was 50% larger than the average daily trading volume recorded in January and February 2020.

- Between 1 September 2019 and 17 March 2020, MMSR reporting agents provided US dollar funding to, on average, 578 different counterparties per day in the EUR/USD FX swap market. Between 18 March (when the enhanced swap lines were launched) and 30 April, the average daily number of counterparties borrowing US dollars from MMSR reporting agents grew to 648, representing an increase of roughly 12%.

- The analysis was conducted on results of the Eurosystem's US dollar operations that were carried out between 18 March and 7 April 2020. The group of MMSR reporting agents considered to be "participating" banks are those that took part in the Eurosystem’s US dollar operations during the same period. Reporting agents with no or negligible participation were included in the “not participating” group.